by Peter Brook

Inflation, interest rates, commodity prices and electricity prices

After a decade of low and stable inflation and extremely low interest rates primarily driven by the global financial crisis in 2009 and then the COVID19 global pandemic, the situation has now changed. Inflation across the globe has risen sharply (e.g., USA 8.3 per cent, UK 7.0 per cent, NZ 6.9 per cent, and India 7.8 per cent) . Key drivers of this include the pandemic i.e., government stimulus policies, supply chain disruptions, labour shortages and key input shortages (e.g., semi-conductors, polysilicon). More recently Russia’s invasion of Ukraine has caused large increases in energy and many commodity prices.

‘Demand pull’ inflation is caused by an overheating economy with strong aggregate demand growth, low unemployment and rising wages. In contrast, this situation is ‘cost push’ inflation where the primary drivers are supply side costs increasing, as opposed to wages growth and aggregate demand.

Inflation and the cash rate

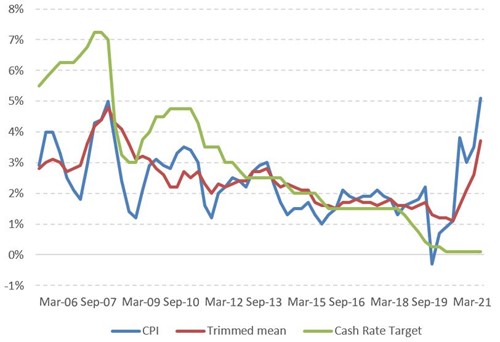

Figure 1 illustrates the recent spike in inflation and how it has rapidly accelerated from a negative value in 2019. The trimmed mean strips out volatile items but it too has risen sharply, and this is the rate the Reserve Bank of Australia (RBA) focusses on when determining monetary policy. Figure 1 also shows the steady decline in interest rates leading up to the pandemic and then the decrease to extreme monetary policy where the Cash Rate is 0.1 per cent at the end of 2010 it was 4.0 per cent. On 3 May the RBA increased the cash rate to 0.35 per cent.

Figure 1: Annual CPI, Trimmed Mean and RBA Cash Rate Target to 31 March 2022

Source: ABS and RBA

Interest Rates

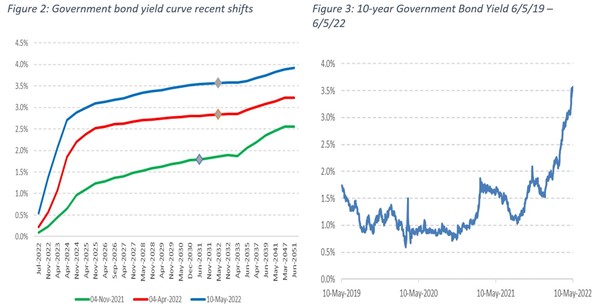

Figure two displays the Australian government bond (AGB) yield curve at three points in time. As can be seen since November 2021 the curve has increased significantly. The grey diamonds indicate the 10-year AGB rate which for financial and regulatory purposes is generally assumed to be the risk-free rate. In November it was 1.83 per cent and by 10 May had increased to 3.57 per cent. Figure 3 illustrates the 10-year AGB yield over the past three years where up until 2022 the yield ranged between 0.5 per cent and 2 per cent.

Source: RBA

How will this affect electricity prices?

This paper will examine four key determinants of electricity prices both in the near term and longer term:

- Wholesale electricity prices

- Coal, gas and oil prices

- Network costs

- Inflation and interest rates

- Generation investment costs

- Commodity prices, inflation and interest rates

- Network investment costs

- Commodity prices, inflation and interest rates

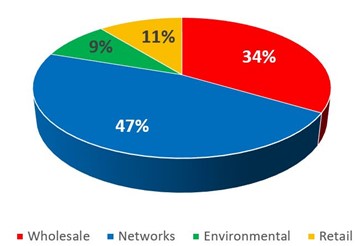

Residential electricity prices are comprised of four components, wholesale electricity, network, environmental and retail. Figure 3 illustrates the proportion of each cost on average in the National Electricity Market (NEM). Network costs include transmission and distribution costs and is the largest cost component. Across regions the percentages differ with Queensland having the highest network (49 per cent) and wholesale (38 per cent) while Victoria has the lowest network share (46 per cent) and SA the lowest wholesale share (28 per cent).

Figure 4: NEM residential electricity price cost shares 2021/22

Source: AEMC Residential Electricity Price Trends 2021

Wholesale electricity prices

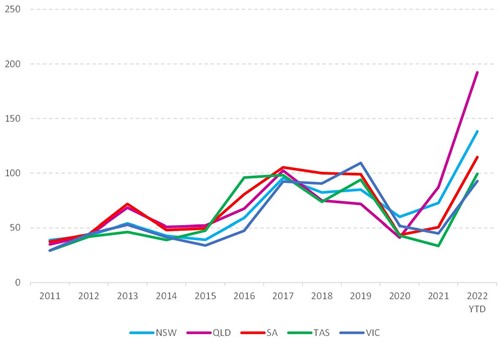

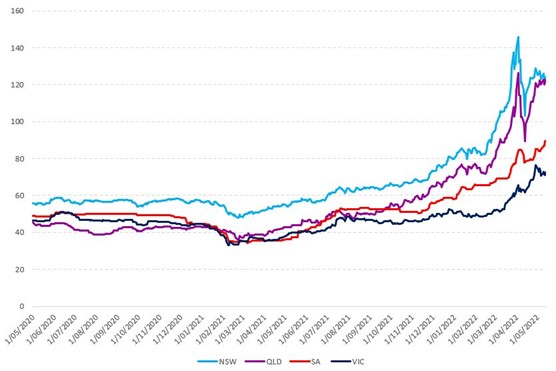

Figure 5 shows average spot prices over the past decade and clearly shows how prices have increased in 2022 year to date (as at 16 May). Queensland prices are at $192/MWh and NSW are at $138/MWh.

Figure 5: Calendar year time weighted average spot prices by NEM region ($/MWh)

Source: NEOexpress

Figure 6 illustrates flat calendar year forward prices over time. As can be seen in March 2022 New South Wales and Queensland forward prices increased dramatically with a clear spread between the black coal northern states and the non-black coal southern states. The rapid increase in forward prices can be explained by:

- Very high and sustained spot prices in NSW and Queensland;

- Victoria to New-South-Wales interconnector flow north is mostly constrained to low or reverse flows during daylight hours due to the recent commissioning of a number of large-scale solar farms near the interconnector (in 2021), which is expected to continue into the future;

- The 17 February announcement of potential early retirement of Eraring (2,922MW) closure by August 2025;

- Delay of the return of major units including Callide C4 (420MW) and Swanbank E (385MW) in Queensland; and

- Expectations of higher fuel costs.

Figure 6: NEM calendar 2023 flat forward prices over time to 13 May 2022 ($/MWh)

Source: NEMfutures by Global-Roam

The spread between northern and southern states can be further explained by fuel types and flexibility:

- Brown coal generation in Victoria is very cheap but inflexible, which means during periods of surplus it is unable to greatly reduce output.

- Black coal in NSW and Queensland is moderately flexible and has a degree of exposure to export prices.

- Gas and diesel plants are very flexible, but exposed to world LNG and oil markets.

- Wind is intermittent, flexible and has a negative fuel cost because they produce Large Generation Certificates (LGCs) under the Renewable Energy Target.

- Large-scale solar cost and flexibility is similar to wind, but operates daytime only. Rooftop solar is mostly uncontrollable.

- When there is surplus electricity, typically caused by a combination of low demand, high renewables and inflexible coal plant, it becomes necessary to curtail (or “spill”) large-scale renewable output. Given they have a negative fuel cost, these plants will set a negative market price equivalent to the LGC price when they spill.

Wholesale prices are dependent on many factors including demand, transmission constraints, outages, weather, and contract positions. One of the key drivers of wholesale electricity prices is fuel costs. The short run marginal cost (SRMC) of a thermal generator is an important component when generators decide the prices at which they bid their capacity into the market. Fuel costs account for most of gas-fired generation SRMCs and a major portion of coal-fired SRMCs. In addition to influencing bidding behaviour, SRMCs will also determine contract prices offered by generators.

Fuel and wholesale prices

Coal

Of the four mainland NEM regions only NSW and Queensland are potentially exposed to global thermal coal prices. A recent article in the Australian (11 May 2022, p18) observed that in NSW (with the exception of Mt Piper), the coal-fired power stations are connected to the rail network that transports coal to Newcastle for export which exposes them to global prices to varying degrees, noting that the coal required for power stations is not as high as the global benchmark. The other issue is that coal exporters are trying to export more coal which makes it harder for generators to access coal due to demand on the rail network. In contrast, only one Queensland generator (located in the coal export port of Gladstone) is directly exposed to global prices. All other coal-fired power stations are what is referred to as mine mouth, so located close to supply.

Figure 7 illustrates the dramatic rise in monthly average thermal coal prices which appears to have peaked at $453/T. However forward prices to July 2022 are above $500/T but the curve is in backwardation with prices trending down to 300/T by 2024. In contrast the price was 124AUD/T in April 2021. Hence, the price of thermal coal has increased by a factor of 3.7. In simple terms, a black coal generator requires approximately 0.4 tonnes of coal to produce 1MWh of electricity. At 124AUD/T a 70 per cent export exposed generator would have a fuel cost of $36/MWh whereas at the current price the cost is $127/MWh.

Figure 7 Newcastle Thermal Coal AUD/T Monthly Price May 2017 – December 2024. Futures from May as at 12 May 2022

Source: https://au.investing.com/commodities/newcastle-coal-futures-historical-data; https://www.barchart.com/futures/quotes/LQ*0/futures-prices; RBA.

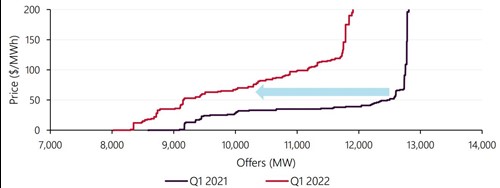

Figure 8 illustrates how black coal bidding has changed recently with more capacity being bidded in at much higher prices. Over 3,000MW of offers were moved from lower price bands to above $60/MWh.

Figure 8: NEM black coal fired generation bid supply curve – Q1 2022 versus Q1 2023

Source: AEMO Quarterly Energy Dynamics Q1 2022

Gas

The most common types of gas-fired generation in the NEM are open cycle gas turbines (OCGT) and combined cycle gas turbines (CCGT). OCGTs are generally peaking plants and require around 10GJ of generate one MWh. CCGTs are generally mid-merit and require around 6GJ/MWh. Reciprocating engine gas-fired generators are another type which may become more common in the NEM and their usage is around 7GJ/MWh. Barkers Inlet power station in South Australia was the first large-scale plant using this technology in Australia. These plants offer fast ramp rates

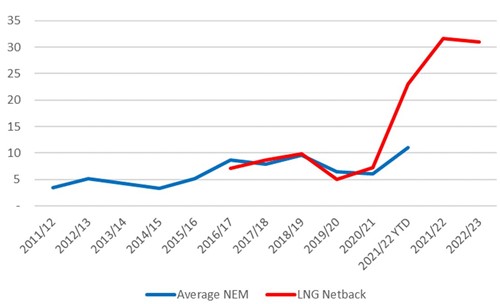

Figure 9 illustrates how wholesale gas prices have steadily increased since 2015. When the Queensland LNG export trains were commissioned prices bottomed in 2020/21 and have since increased to peak at over $10/GJ. Figure 3 also shows the LNG netback price which subtracts liquefication and transport costs from the price of Asian LNG prices. As can be seen, the two price series have tracked each other closely up to 2020/21 and there has been a massive divergence since then. If domestic gas prices continued to track LNG netback prices gas prices will stabilise around $30/GJ.

Figure 9 Financial year average NEM wholesale gas prices to Dec 2021 and LNG netback prices including futures as at 19 April (AUD/GJ)

Source: https://www.accc.gov.au/regulated-infrastructure/energy/gas-inquiry-2017-2025/lng-netback-price-series; https://www.aer.gov.au/wholesale-markets/wholesale-statistics/gas-market-prices

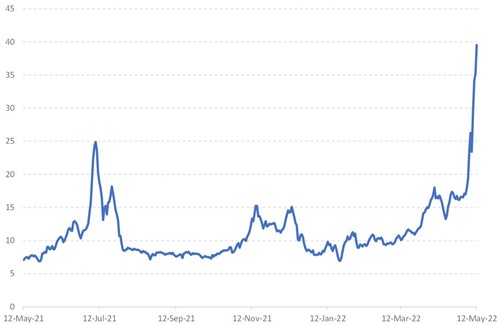

While Figure 9 shows relatively stable gas prices it is important to be cautious with annual average prices. Figure 10 displays the average of daily short term trading market (STTM) gas prices for Adelaide, Sydney and Brisbane and average daily wholesale prices in the Victorian declared wholesale gas market (DWGM). On a daily basis gas prices have ranged from $5/GJ to over $30/GJ.

Figure 10 provides better resolution of gas prices for the past 12 months. Over the period prices have ranged between $7/GJ and $40/GJ with recent prices being well over the netback price shown in Figure 9. If gas generators had to pay $40/GJ the fuel cost for OCGT would be $400/MWh and $240/MWh for CCGT. This would make OCGT almost as expensive as diesel generation prior to the recent oil price increase.

Figure 10: Daily wholesale gas prices ($/GJ) 12 May 2021 12 May 2022

Source: AEMO

Oil prices

Oil prices and their impact on domestic diesel prices can also affect prices because a number of generators are powered by diesel or have dual gas/diesel capability. Prior to the surge in oil prices diesel (excluding the excise) was around $1.00/Lt but is now around $1.50/Lt, which increases diesel generation costs by 50 per cent. The forward market in Figure 11 indicates that prices will decrease but remain over 120AUD/bbl.

Figure 11: AUD Brent crude monthly prices AUD/bbl, futures from July 2022 with AUD at USD0.69 (as at 12 May 2022)

Source: US Energy Information Administration; RBA; and https://au.investing.com/commodities/brent-oil-contracts

Networks

As can be seen from Figure 4 network costs represent the single biggest component of residential electricity prices. There are two network charges, transmission use of service (TUOS) for the high voltage network and distribution use of system charges (DUOS) for the low voltage network ie, the power lines you see in your street. When combined these charges are known as network use of system (NUOS) charges and as noted above at a NEM level they represent 47 per cent of residential electricity costs. Within this 8.3 per cent is TUOS and 38.4 per cent is DUOS.

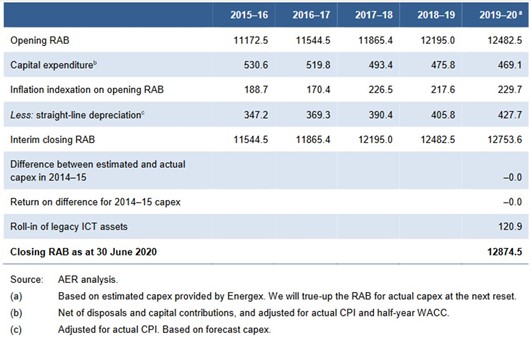

Networks are capital intensive natural monopolies and the AER regulates the revenues they are allowed to recover and the level of capital expenditure (capex) they can undertake. NSPs are regulated on a five-yearly basis which establishes their expected returns and regulatory asset base (RAB) over a five-year regulatory control period (RCP). A breakdown of the revenues (for Energex) is set out in Table 1. As can be seen the largest item is return on capital which is determined by multiplying the RAB by the weighted average cost of capital (WACC) as determined by the AER. In the case of Energex its opening RAB was $12.9 billion and its WACC was 4.73 per cent yielding a return on capital of $609 million for 2020/21.

Table 1: Energex 2020-25 Final Determination: Annual expected revenues

Source: AER

Under the CPI–X framework, the X factor measures the real rate of change in annual expected revenue from one year to the next. A negative X factor represents a real increase in revenue. Conversely, a positive X factor represents a real decrease in revenue.

Within the RCP, NSPs are allowed to adjust their tariffs and charges to reflect actual inflation and for DNSPs these tariffs are approved annually by the AER.

Inflation and Regulated DNSPs and TNSPs

Inflation is a key input into the revenue determinations and tariffs of electricity network service providers. This because the NER requires the AER to provide a real rate of return consistent with the opportunity cost of capital for NSPs. The revenues recovered by NSPs are in nominal dollars which means they need to be compensated for inflation to ensure the real rate of return is received and the value of the original investment in real terms is preserved. As part of the regulatory process which determines the cost of network services, the AER uses actual and expected inflation (referred to as the consumer price index (CPI) hereafter) in the following ways:

- Actual (lagged) CPI is applied each year when DNSPs submit new tariffs for AER approval and TNSPs adjust their tariffs to ensure they are recovering their maximum allowed revenue (MAR).

- At the commencement of each five yearly regulatory control period (RCP), expected inflation is used in the AER’s Post Tax Revenue Model to determine forecast annual revenues and indexation of the RAB. The indexation also determines the annual regulatory depreciation allowance (ie, straight line depreciation less RAB indexation).

- At commencement of each RCP, the RAB is ‘rolled forward’. As part of this process, the RAB is taken back to its value at the start of the previous RCP and indexed by actual inflation over that RCP.

Referring back to Energex in Table 1, these revenues are only forecasts and from the second year of the RCP they are updated to incorporate actual inflation. The AER’s expected inflation assumption was 2.27%. However, the actual inflation used for setting Energex’s 2022-23 revenues is 3.5 per cent. Hence, all things being equal that year’s revenue will be $15 million higher than forecast.

Table 2 sets out the roll forward of Energex’s RAB to establish the opening RAB for the 2020-25 RCP. The indexation of the based on actual CPI. During the 2020-25 RCP the RAB will be indexed by the AER’s expected inflation of 2.27% and for the next RCP (2025-26) the RAB will be updated to reflect actual inflation. If CPI is five per cent over the remaining three years of the current RCP, the RAB at the commencement of the next RCP could be over $350 million larger due to higher CPI.

Table 2: Energex 2020-25 Final Determination: RAB roll forward for 2015-20 RCP

Interest Rates and Network Costs

At each five-yearly revenue determination a new rate of return is set. This is the weighted average cost of capital (WACC) which has two components:

- Gearing assumption ie, percentage of debt versus equity.

- Return on Equity (ROE)

- Cost of Debt (COD)

For the purposes of estimating the WACC, NSPs are assumed to be geared at 60 per cent with the balance being 40 per cent equity. Apart from providing the weightings for the ROE and COD the gearing assumption also influences the equity beta and credit spread (both described below).

The ROE is the risk-free rate plus the systemic risk of the industry relative to the market (equity beta) multiplied by the market risk premium. The risk-free rate is the yield on 10-year Australian Government Bonds (AGB) at the time of the determination. Below is an example from a recent TNSP determination of the ROE.

6.16% = 2.5% + 0.6 * (6.1%)

In simple terms, the COD is the risk-free rate plus the credit spread (above the 10-year AGB yield) for a BBB+ rated 10-year bond issued by a stand-alone DNSP or TNSP. In practice the process for estimating this is complex using multiple data sources but the intent is to estimate the simple equation. NSPs are also allowed to recover debt raising costs. An example of the simple COD approach from the same determination would be:

4.35% = 2.5% + 1.85%

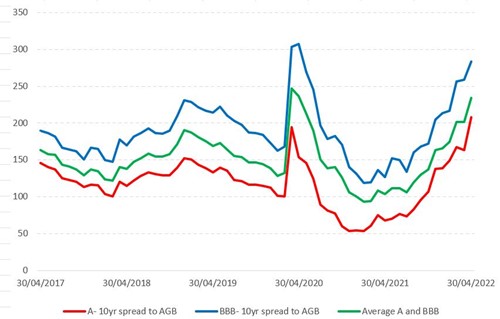

Unlike the ROE which remains in place for the RCP, the COD is updated annually because the AER uses a 10-year trailing average approach. This assumes the NSP refinances 10 per cent of its debt each year. The COD is changed to reflect the impact of the new borrowing costs on the existing COD. Hence, if rates and/or credit spreads increase, the COD will slowly capture these increases. The average of A rated and BBB rated spreads to AGB is a proxy for BBB+ spreads which is the assumed credit rating for a stand-alone NSP. Figure 12 illustrates credit spreads over the past five years and how they have more than doubled since April 2021.

Figure 12: Estimated credit spreads to 10-year AGB: A rated, BBB rated and average (basis points)

Source: RBA

Powerlink case study

Powerlink’s draft determination was released on 30 September 2021 and its final on 26 April 2022. During that five-month period, interest rates and inflation both increased. The risk-free rate increased from 1.53 per cent to 2.50 per cent, annual inflation to December 2021 was 3.5 per cent and the AER increased its inflation assumption from 2.25 per cent to 2.65 per cent. The return on equity increased from 5.19 per cent to 6.16 per cent and the return on debt increase marginally. The higher inflation resulted in the final RAB being $174.5 million higher than the draft. This resulted in Powerlink’s allowed revenues increasing by $152 million (4.2 per cent higher) between the draft and final decision.

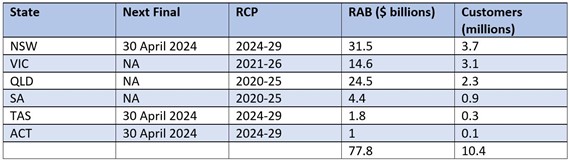

NSP Reset dates

To put all of this into perspective, the total RAB of all NSPs is $100 billion. If forecast inflation is 2.5 per cent and actual inflation is five per cent in any given year the annual indexation of their RABs would increase from $2.5 billion to $5 billion.

If their WACCs were to be increased by one per cent they would earn an additional $1 billion of revenue per year. This scenario in conjunction with unexpected RAB increases due to inflation returns would further increase NSP revenues. This simplistic WACC scenario ignores the timing of regulatory determinations. Tables 3 and 4 set out the timing of regulatory determinations. Six NSPs ($45 billion of RAB) have commenced the regulatory determination process with final decisions due in April 2023 and April 2024.

Table 3 DNSP regulatory determinations

Source: AER

The three DNSP regulatory processes on foot are NSW, Tasmania and the ACT. These total over $3 billion of RAB and 4.1 million customers.

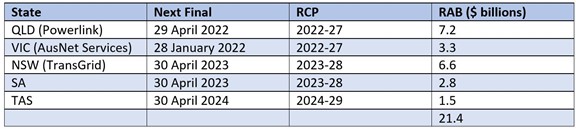

Table 4: TNSP regulatory determinations

Source: AER

The three TNSP regulatory processes on foot are NSW, SA and Tasmania. These total nearly $11 billion of RAB.

New renewable generation and storage (batteries)

When assessing a new generation project such as a solar or wind farm, the levelized cost of electricity (LCOE) is a key determinant of the project’s viability. LCOE incorporates all of the project’s costs (ie, capital, financing, opex, etc) and the expected output of the plant to determine the price of the electricity produced by the plant. The WACC for the project is the rate that is used to discount the cash flows and output. A simple analysis based on market data, gearing assumption and risk assumption produces a real pre-tax WACC of 6.6 per cent in 2021. Combining this with an output assumption yields an LCOE of $50/MW. Updating these assumptions for higher interest rates and credit spreads produces an LCOE of $60/MWh, a 20 per cent increase of the LCOE. This simple example illustrates how interest rates and credit spreads increase the costs of new generation.

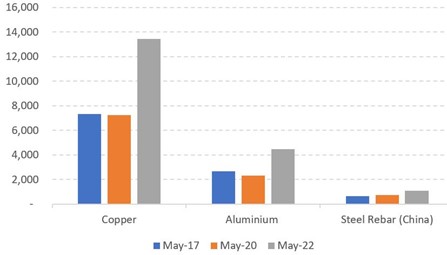

In addition to the interest rate cost pressure, higher commodity prices are also likely to increase the cost of projects as well as inflation and demand driving higher wages. Figure 13 illustrates how key commodity input prices have increased.

Figure 13: Metal prices over last five years (AUD/Tonne)

Sources: https://tradingeconomics.com/ ; RBA; http://www.kitcometals.com/; https://www.macrotrends.net/

Since May 2020 prices for metals that are critical for network investment have risen: Copper up 85 per cent; aluminium up 94 per cent; and steel in China is 48 per cent higher.

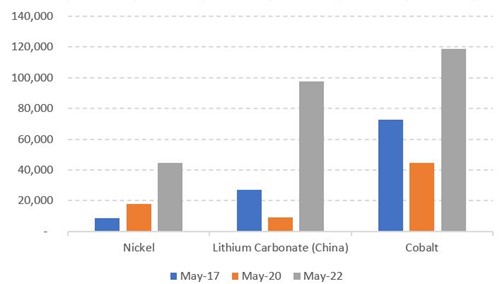

New battery investment costs will increase due to the reasons outlined above and the massive increase in battery metal costs. Figure 14 illustrates the increases in key battery metals.

Figure 14: Battery minerals May prices over five years (AUD/Tonne)

Sources: https://tradingeconomics.com/ ; RBA; http://www.kitcometals.com/; https://www.macrotrends.net/

Since May 2020 battery metal prices have increased substantially: nickel by 147 per cent; lithium up 948 per cent; and cobalt up 165 per cent. According to recent research by the Bank of America the cost share of nickel and lithium for a lithium ion battery has risen from 21 per cent to 34 per cent.

While these cost projections will affect all projects across the NEM, NSW electricity consumers may be particularly vulnerable. This because the NSW Electricity Infrastructure Act (2020) requires at a minimum the construction of 12GW of renewable generation and 2GW of long-term storage (LTS) by 31 December 2029. These investments will be underwritten by put options being provided to renewable generation projects and annuity arrangements to ensure storage projects receive an adequate rate of return. Higher interest rates and the resulting higher LCOEs have the potential to increase the strike price of the put options issued to generators which will increase the risk that the NSW electricity consumers have to pay out on the options. The required rate of return will also be likely to increase the required rate of return for storage developers. However, it needs to be noted that if we are in an extended high wholesale price environment it could reduce the probability of options being exercised, noting the options have a duration of 20 years.

Network investment

AEMO’s Draft ISP 2022 is forecasting over $12 billion of transmission investment over the next decade. As part of the ISP development AEMO acknowledges that higher discount rates will alter the costs and benefits of the projects. In its IASR The cost of these projects can also be affected by the higher commodity prices shown in Figure 12 and the likely increase in labour costs due to the combination of inflation and specialized worker demand.

Similarly, DNSPs are likely to have to undertake significant capex to manage increasing levels of distributed energy resources (DER), electric vehicle uptake and decarbonisation of gas through electrification.

Retail costs

Retailers:

- procure hedged wholesale energy;

- incur prudential costs;

- pay network charges (NUOS);

- pay environmental costs;

- incur cost to serve (CTS) for each customer; and

- incur customer acquisition and retention costs (CARC).

Retailers have to earn a return commensurate with their turnover and this is a function of the cost stack outlined above. As wholesale and network costs increase, the dollar value of their return will have to increase. In addition to this increasing interest rates and/or credit spreads will unilaterally increase the cost of capital for retailers.

Conclusion

Higher inflation, interest rates and commodity prices will increase electricity prices both in the short term and the longer term. The current cycle of commodity prices are contributing to elevated wholesale spot and forward prices and this will affect electricity prices relatively quickly. Higher inflation will flow through to higher network prices at each annual network tariff price setting. Over the medium to long term inflation will increase the nominal value of network assets while higher interest rates and credit spreads will gradually increase the cost of debt for networks. Furthermore, as each NSP’s five-year regulatory reset period expires higher inflation will increase the nominal value of network assets which will embed higher costs. In addition to this higher interest rates and credit spreads will increase the return on equity which will increase costs.

Retail returns are built up on the input costs for a retailer which are primarily network and wholesale. As these procurement costs will be higher retailers will require a higher return and their cost of capital will also increase due to higher interest rates and/or credit spreads.

Finally, higher interest rates and commodity prices will result in higher levelized costs of electricity for new generation and storage (eg, batteries) investment. This will also increase the cost of new transmission and distribution network investment.

In summary, upwards pressure on electricity prices is being applied on all fronts with both immediate and longer-term impacts.

Related Analysis

Network Tariff Reform: From Cost Recovery to Coordination in a High-CER System

Network tariff reform has shifted from a technical pricing issue to a central challenge for Australia’s future energy system, shaping affordability, market design and the transition to a customer-centric grid. Recent modelling by the Australian Energy Market Commission provides a timely and valuable contribution to this debate, with one of the most consequential ideas in its Pricing Review reform package being Recommendation 6—proposing that networks develop tariffs for retailers, rather than directly for end-use customers. We take a closer look at the implications.

Addressing Energy Affordability Needs More Than Short-Term Relief

The conflict in the Middle East has continued to highlight the challenges we face in ensuring energy supply remains accessible and affordable for everyone. Ensuring Australia becomes more resilient to international energy price shocks will dominate the energy policy landscape for some time, and rightfully so. But while political debate often gravitates toward regulatory interventions and subsidies that deliver short term household bill relief, the real solution lies in something far more complex: reshaping how the energy system works for consumers. What’s increasingly clear is that energy affordability is not just about price - it’s about design. That is why the AEC is releasing its Affordability Action Agenda today – an 8-point plan of critical actions that industry and governments need to take to ensure that energy remains accessible and affordable for all Australians. Read more.

Efficient Pricing in an Uncertain Energy Market

Electricity prices are once again front of mind for Australians, and with cost-of-living pressures mounting, expectations for fair and transparent pricing are entirely reasonable. But as reforms to the Victorian Default Offer and Default Market Offer evolve, a more complex challenge emerges: how to keep prices in check without undermining the stability, competition and investment needed to sustain the energy system over time. Striking that balance is at the heart of current reform debates, and will ultimately determine whether today’s affordability measures support or weaken the system in the long run. Read more.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.