by Carl Kitchen

Energy storage assessment: Where are we now?

A new report from the CSIRO has highlighted the major challenge ahead in having sufficient energy storage available in coming decades to support the National Electricity Market (NEM) as dispatchable plant leaves the grid.

The CSIRO assessment used the Australian Energy Market Operator’s (AEMO) 2022 Integrated System Plan for its analysis of what might be required with the step change and hydrogen superpower scenarios, suggesting the NEM could need between 44 and 96GW/550-950GWh of dispatchable storage by 2050, while Western Australia might need 12-17GW/74-96GWh.

The report notes that the combined 3,700MW storage committed to 2030 in short duration storage and longer duration pumped hydro - through the development of Snowy 2.0 in NSW, Kidston in Queensland and Cethana in Tasmania - will cover only a fraction of what is required. Increased uptake at customer-owned storage with home battery systems could cover some of the gap, according to the report. But if that does not fully eventuate, the task will fall to utility-scale developers. There is an increasing sense of urgency to developing alternatives to the traditional dispatchable plants as referenced in the AFR’s ESG Summit this week. So-called “big batteries” are only capable of providing short duration storage of 2 to 4 hours, compared to a typical stockpile of coal providing a one-to-two-month buffer.

The CSIRO expects investment in short and medium-duration storage to play an important part, while it also suggests investment in thermal energy storage systems would be required to deliver process heat in industrial settings. While there are a number of storage technology options the report flags that there are only a handful that are commercially mature. Others remain under development.

Much longer duration storage will be required, but the technology available to deliver that remains limited with the best and most proven option being pumped hydro.

Landing on the most competitive and effective methods of storage will depend on its ability to be used along with site and regional factors that could influence the most viable technology even among similar sectors, according to the CSIRO. Below we take a closer look at the report’s findings.

Horses for Courses

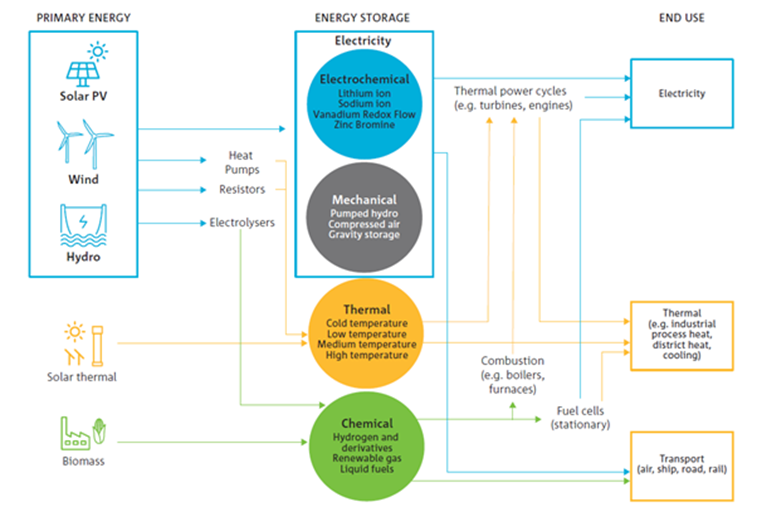

The different types of storage technologies and applications are shown in figure 1 below.

Figure 1: Energy Storage Applications

Source: CSIRO Renewable Energy Storage Roadmap

Applications for energy storage and current limitations are outlined as:

Major grids: These will need a substantial storage capacity as dispatchable generation leaves the grid. It will need to be of varying durations to be able to deal with changes in supply and demand. There are limited commercially mature options deployable in the near term in Australia. Even the most widely applied currently – lithium-ion batteries and pumped hydro – face supply chain risks and geographical constraints respectively.

The remote and off grid mining: Short-duration storage associated with hybrid generation can reduce emissions in the near term. The elimination of emissions will also ultimately require long duration storage. These are not yet widely demonstrated at scale across mining operations.

Remote communities: Storage linked with renewable generation has the potential to increase access to electricity supply, but eliminating emissions will need storage that can maintain power quality and deliver reliable energy for days or weeks.

Manufacturing, mid-temperature processes: Thermal and chemical storage systems along with electrification of processes is considered a means to decarbonise this sector but still in very early stages. The report notes it will require further demonstration and scale up.

High temperature processes: There remains a lack of technology maturity and scale for these applications.

Hydrogen: Large-scale storage would be required if Australia is to meet its hydrogen export ambitions. Hydrogen storage could also play a role in decarbonising heavy-duty vehicles, but it is still emerging.

Maturity

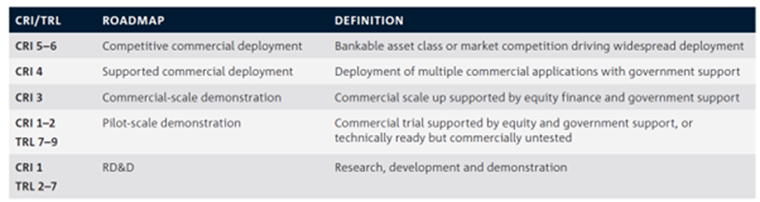

To better understand where specific technologies currently sit, the report provides a useful insight into the current maturity level of energy storage technologies, using the commercial readiness index (CRI) as well as a technical readiness level (TRL) framework. The intent is to provide decision makers with a tool to understand investment risks, barriers and actions to commercial scale up.

The CRI is usually employed to determine the maturity level of storage technologies, however, the report also provides an assessment of various technology’s TRL “to understand the nuances between technologies that are at a lower level of commercial readiness”. The definitions for the various levels are shown below. More detailed assessment by various energy storage technologies is at the bottom of this article.

Grid Applications

In considering applications for major grids, the table shown in this link* highlights the capabilities and limitations of various storage technologies, while the second table shown in this link* outlines the key factors that would impact considerations of the technologies.

The first table shows that the best option for longer duration storage is pumped hydro, while concentrated solar thermal (CST) with molten salts and underground hydrogen may have potential. But as noted underground hydrogen is a long way from commercial maturity and CST with molten salts continues to be developed. Molten salts are considered to offer flexibility and efficient heat storage, and have that capability because of the heat they can transfer to support a wider range of power generation options. The first commercial molten-salt TES plant came on line in 2008 with the ANDASOL 1 parabolic trough plant of 50MW in Granada Spain. Molten salt is currently the most used in the power sector and molten salt storage capacity is estimated to be 21GWh worldwide. As noted by ARENA, to date, there has been very little use of CST in Australia. ARENA is supporting a proposed concentrated solar thermal power (CSP) plant in Port Augusta, South Australia. The project is expected to reach a financial close later this year.

Pumped hydro energy storage (PHES) is mature and well-established and used for large-scale energy storage and management. It is considered low risks with more than 9000GWh estimated to have been installed globally. It accounts for more than 95 per cent of installed storage around the world and highlights the need to get other technologies to commercial maturity to meet the decarbonisation challenge. Pumped hydro is limited by geographical considerations as shown in the table in this link.

Lithium-ion batteries have reached competitive commercial deployment for short-duration grid use, and can be constructed in 8-20 weeks, according to the CSIRO. There are a large number of batteries proposed for Australia, including the Waratah Super Battery in New South Wales and eight grid-scale batteries (total of 2GW capacity) which received ARENA support at the end of last year.

CST plus storage is considered to be competitive commercially and is able to provide medium and long intraday storage. Vanadium redox flow batteries (VRFB) are most suited to short- and medium-duration grid use and benefit from being able to operate in higher temperatures than lithium-ion batteries. Compressed air energy storage adiabatic (A-CAES). While these are considered mature because commercial systems are available, it is still undergoing commercial-scale demonstrations and benefits from a moderate footprint. Development times are considered to be 2.5-3.5 years.

Liquid air (LAES), zinc–bromine batteries (ZNBR), underground hydrogen and thermal energy storage systems are all being studied to meet medium-duration and grid-scale storage applications. LAES and ZNBR batteries are currently in pilot-scale demonstrations, while underground hydrogen and thermal energy storage systems require more time for development. LAES and ZNBR batteries benefit from minimal geographical considerations and short construction time frames, while underground hydrogen and thermal energy storage systems require longer development times and their deployment may be limited by geographical considerations. Advantages of thermal energy storage systems include modularity and scalability.

Concrete and packed bed systems have been demonstrated in district heating and manufacturing applications and could potentially be used in an eTESe system to generate electricity. Miscibility gap alloys (MGA) systems and Na-ion batteries are both in the RD&D phase and being considered as options for both short and medium-duration storage. Gravity storage systems are also in the pilot-scale demonstration stage and are aimed at providing medium-duration storage. Other lower CRI storage alternatives such as sodium sulphur batteries and polysulfide bromine batteries can provide grid storage at different durations, as with chemical carriers such as methanol, ammonia, and liquid organic hydrogen carriers.

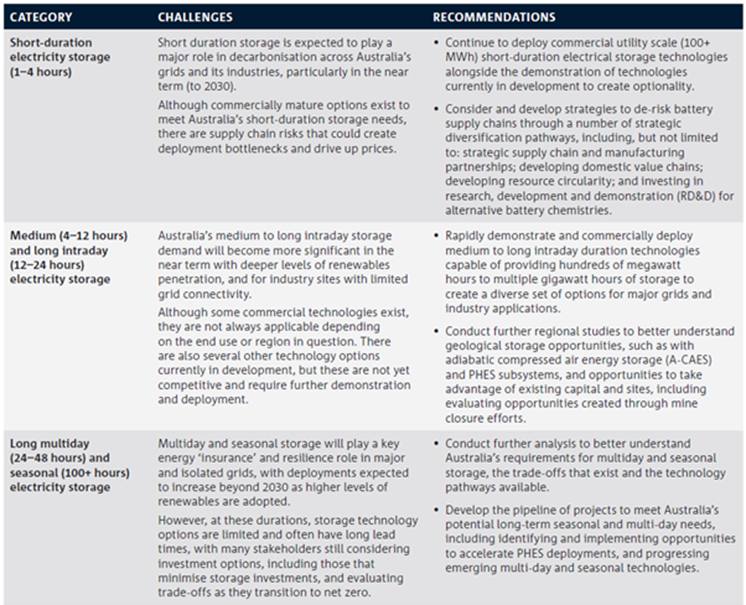

The challenge remains to continue to increase our storage options as the transition advances and the report does make a range of recommendations to encourage development and these are outlined in the table below.

The maturity and stage of development of a range of storage technologies as assessed by the CSIRO is shown in the following tables.

Lithium Ion batteries

Vanadium redox flow batteries

Zinc Bromine batteries

Sodium ion batteries (Na-ion batteries)

Pumped hydro

A-CAES

Liquid air energy storage

Gravity energy storage (Vertical weights)

Underground hydrogen

Molten Salts

*All tables sourced from CSIRO Renewable Energy Storage Roadmap

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Australia’s Home Battery Surge: A Question of Equity

Australia is a global leader in rooftop solar, with more than 4.3 million households and small businesses installing photovoltaic (PV) systems as of February 2026. Battery uptake has also accelerated, particularly since the introduction of the Cheaper Home Batteries Program in July 2025, which offers around a 30 per cent upfront discount for systems between 5 kWh and 100 kWh. More than 236,000 batteries had been installed by February 2026, although this likely understates the true figure due to reporting lags; the Federal Government has since indicated installations have surpassed 250,000 as of March 2026. Despite this rapid growth, an important question remains: who is actually benefiting from these subsidies?

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.