by Rhys Thomas

Ireland’s Green Energy Rule: What Can Australia Learn From Its Approach to Data Centres?

A repeated theme at the Australian Energy Council’s inaugural Energy2050 Conference last week was what to do about data centres. The message from various speakers across the day was clear: data centres are an enormous economic opportunity, but policy settings must be designed carefully to avoid adverse impacts to customers and the environment.

For their part, Energy Ministers are keen to require data centres to bring in additional renewable generation and firming if they want to locate in Australia. What that looks like in practice is currently up in the air. Helpfully, there is precedence with Ireland introducing a similar policy late last year.

In this article, we look into Ireland’s data centre policy and see what lessons it might hold for Australia.

Ireland’s history with data centres

Up until 2022, Ireland had been a primary destination for data centre investment. Its combination of modest corporation tax rates, stable and low temperature climate (which makes data centre cooling easier), and access to critical transatlantic cables made it a popular choice for developers.

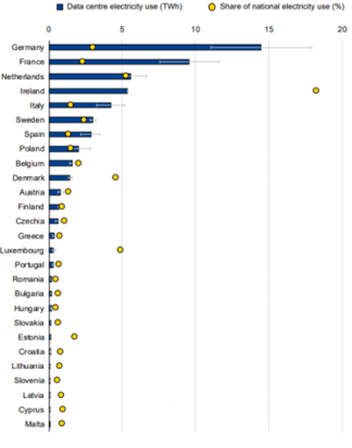

As the graph below shows, these favourable conditions resulted in data centres coming to represent a significant chunk of Ireland’s total electricity demand, about 18 per cent, far above any other European country. For comparison, data centres in Australia were responsible for about 2 per cent of total NEM-wide consumption in 2025, and this is forecast to grow to 12 per cent by 2050[i].

Figure 1: Estimated data centre electricity use by country, 2022

Source: Ireland’s Commission for Regulation of Utilities, Large Energy Users Connection Policy, p39.

Ireland’s rapid data centre development also brought scrutiny about the potential impacts it was having on electricity prices, grid stability, and the country’s emissions.

Ireland’s state operator, EirGrid, subsequently enforced a de-facto moratorium on new data centre connections in 2022, which stayed in effect until December 2025 when Ireland’s Commission for Regulation of Utilities (their equivalent of the Australian Energy Regulator) published the “Large Energy Users Connection Policy” (‘LEUC Policy’).

Despite its neutral sounding title, the LEUC policy is designed to “apply exclusively to all data centres seeking to connect to the electricity network” and sets out the range of requirements they must meet to receive connection access.

The Commission reasoned that specific rules were needed for data centres because of their unique attributes: the rapid rate at which contracted demand can ramp up and their large flat energy profile.

The requirements in the LEUC Policy are the bureaucratic workings of a government directive to ensure data centre growth supports Ireland’s climate change targets, as well as the economy.

In this respect, Ireland’s LEUC Policy is instructive for Australia because Energy Ministers, through the most recent May ECMC Communique, have requested advice from policymakers on implementation options to ensure data centres “invest in additional renewable generation and firming in their state of operation to fully offset their electricity demand and provide demand flexibility services”.

What can Australia learn from Ireland?

The table below considers some of the key policy issues currently dominating data centre debates and compares how Ireland’s LEUC Policy has tackled them versus considerations in the Australian context.

| Policy Issue | Ireland Position | Australian Context |

| How to determine whether renewable generation is additional/new? |

Generation is additional so long as it -Is not already operational in the market - Has not been previously contracted or committed - Is outside any government support schemes |

Policymakers will need to consider whether government-funded generation counts as additional. This would include, for example, generation underwritten through schemes like the Commonwealth’s Capacity Investment Scheme (CIS) and NSW’s Long-Term Energy Service Agreements (LTESAs).

Additionality could be demonstrated through the purchase of Large-scale Generation Certificates (LGCs) or Renewable Electricity Guarantee of Origin (REGO) certificates, with the latter having attributes like time and jurisdiction that can be leveraged. |

| Does additionality mean 100 per cent of data centre demand must be met by renewable generation? |

Data centres are required to meet at least 80 per cent of their annual demand with additional renewable electricity generated in Ireland (this is designed to align with the Irish Government’s target of 80 per cent renewable electricity in 2030). |

Australia currently has an 82 per cent renewable energy target by 2030, with different state targets sitting underneath that.

While symmetry can be visually appealing, policymakers will need to weigh the barrier to entry this might impose, noting there is less time for preparation here than in Ireland which has been consulting on their policy for some time.

Australia’s federated structure may also complicate target setting, with Queensland already disagreeing on the need for additionality as expressed in the Energy and Climate Change Ministerial Council (ECMC) Communique from May 2026. |

| What about the time it takes for new renewables to be built? |

Data centres have a 6-year glide path from the date of demand site’s energisation in order to meet the above 80 per cent annual requirement.

As part of the grid connection application, data centres must show a credible plan in relation to how they intend to meet that 80 per cent. This includes, for example, identifying the specific renewable generation that will support the projects and the anticipated timeline for development. |

While there are project variables, research from Net Zero Australia suggests large-scale wind projects take around eight years to develop, while solar farms are over five years on average.

Even with financing from data centres, supply-side barriers like planning approvals, social licence, and access to critical electrical equipment means it is difficult to build renewables quickly.

Policymakers should also consider how any requirement would interact with the Electricity Entry Services Mechanism (ESEM) which is set to kick in late 2027. |

| What generation do data centres use in the meantime? |

Small data centres are required to provide an auto-producer unit that meets 100 per cent of demand on a de-rated basis.

Large data centres must provide dispatchable generation and/or storage capacity equivalent to their peak demand.

Because there is no renewable requirement, these requirements along with the glide path have received criticism for allowing fossil fuel generation to be used in the interim. Some environment groups have taken legal action against the decision on this basis. |

Noting that the Renewable Energy Target (RET) and related LGCs wind down in 2030, there is likely to be a reasonable volume of existing renewable generation looking to re-contract.

Policymakers may be interested in encouraging some contracting with existing renewables during any glide path or transition period to minimise emissions but also maintain commercial incentives for existing renewable generation.

|

| Must data centres be connected to the grid? |

While data centres can use on-site or proximate generation, it must be separately connected and metered and participate in the wholesale electricity market as a standalone market unit. Islanded data centres are not permitted.

The System Operator, not the data centre, will have responsibility for dispatch.

Despite pushback from data centre developers about logistical and financial burdens, the Commission determined this is necessary for system security and to maintain control over generation access in the event of data centre non-compliance. |

While some data centre developers prefer total behind-the-meter solutions to avoid grid connection delays, policymakers should weigh that against the benefits of grid-connected investment.

The National Electricity Market has design features intended to expose large loads to the cost of new entry through scarcity pricing (such as the market price cap) and the forward market to ensure the efficient economic pooling of risk.

Further, grid-connection reduces the risk of stranded assets and under-utilised build, allowing for generation to be used elsewhere even when the data centre shuts down. |

| Where must the generation be located? | The generation must be on-site or proximate to the data centre; however, the Commission has chosen not to define what counts as “proximate”. It will instead be assessed on a case-by-case basis by the System Operator. |

Given’s Ireland’s small geography and unitary government structure, their location requirement may not be too instructive for the Australian context.

The ECMC Communique has a “state of operation” requirement which presumably means the generation must be located in the same state jurisdiction as the data centre.

There will be intrigue over how policymakers approach this topic as it seems to go against the NEM’s intended design features which is to enable efficient investment in generation through an interconnected wholesale electricity market.

Further, noting that most prospective data centre projects are aiming to be located in Melbourne or Sydney, it could increase the risks of network congestion and inefficient build if generation cannot be spread across the NEM. |

| Should data centres be required to provide demand flexibility? |

There is no requirement for data centres to provide demand flexibility contribution to the system.

The Commission reasoned that requiring onsite or proximate generation was enough and mandating demand flexibility on top would be too onerous. Furthermore, they placed confidence in emerging market initiatives and network options to smooth demand. |

The ECMC Communique has tasked policymakers with ensuring data centres provide demand flexibility options to reduce costs.

There are different options for achieving this each with their policy trade-offs: - Back-up (behind-the-meter solutions have a role, but it tends to be less efficient and can risk becoming stranded. Further, policy design should ensure that low emissions back-up, such as batteries, is incentivised over emissions intensive options like diesel). - Load shifting (while tariff signals can be an efficient tool, the incentives for behavioural change may only be strong enough for certain data centre use cases, such as non-critical processing). - Market directions (the most blunt and direct instrument but also carries significant costs and not a sustainable long-term option to maintain system security). |

Conclusion

How to effectively regulate data centre investment in the electricity system is likely to remain a hot topic for some time and fairly so as it is something that must be done right. Excessive or cumbersome regulation could deter investment and curb what is an enormous economic opportunity for Australia.

Equally, there are legitimate concerns that adding such high and sudden demand without the necessary system planning could impact customer bills and Australia’s carbon emissions.

From the energy industry’s perspective, the NEM, its market bodies, and market participants have a sophisticated and largely successful history of connecting and servicing large loads. Making full use of this knowledge and experience will require genuine consultation about the rules and regulations being developed, to allow for market-based solutions that most efficiently manage capital and risk.

[i] AEMO’s updated forecasting methodology targets rapidly growing electricity loads, following industry consultation

Related Analysis

Conference highlights: Shared vision, Real challenges

The Australian Energy Council’s inaugural Energy2050 Conference brought together industry leaders, policymakers and experts to discuss the opportunities and challenges shaping Australia’s energy transition. While there was broad consensus on the direction of the future energy system, speakers highlighted the significant investment, infrastructure and policy challenges that must be addressed to deliver it successfully. Read more.

From Energy to Flexibility: Rewiring Australia’s Wholesale Markets for Net Zero

Australia’s path to net zero will depend not only on new technologies, but on fundamentally reshaping the markets that underpin the energy system. As coal exits, renewables, storage and consumer energy resources will drive a far more dynamic and decentralised National Electricity Market, where flexibility becomes the critical commodity. We explore the market reforms, investment signals and system changes required to deliver a secure, affordable and reliable Energy2050 future, themes that will also sit at the centre of the Australian Energy Council Conference 2026 in Sydney on 4 June.

Global oil shock, but local calm - how the NEM is holding steady

Whilst Australia is lucky to be located well away from the horrors of the war in Iran, we are witnessing some economic impact with higher petrol and diesel prices. However, can there be impacts on the electricity market as well? In short, yes, but at this stage these impacts are minimal. We take a look at how the oil price could impact the electricity market and what the market has observed so far. Read more.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.