by Carl Kitchen

How do we deal with emerging excess supply?

A great deal has now been written about the early closure of Yallourn Power Station in 2028, with many commentators outlining the potential implications for Victoria and the broader National Electricity Market (NEM) of coal plant closures.

The economics of traditional plants are well understood, but since their construction, the way they need to operate has changed substantially. This has been driven by a combination of the age of the plants as well as the large influx of renewables, which is changing the supply and demand patterns of the grid.

The Clean Energy Regulator’s most recent Quarterly Carbon Markets Report shows two records were achieved last year – 7GW of new renewable energy capacity delivered across Australia.

The Small-scale Renewable Energy Scheme (SRES) delivered 3GW of the new renewable energy capacity, with the remaining 4GW coming from power stations accredited under the Large-scale Renewable Energy Target (LRET). Australia has now met its LRET of 33,000 gigawatt hours (GWh) with the CER expecting eligible generation could reach 40,000GWh this year.

Australia has added, on average, more than 6GW of renewable capacity each year since 2018. This “super cycle” of investment is reshaping Australia’s electricity sector.

Renewable developments are further encouraged by state-based renewable targets. These include:

- Victoria’s 50 per cent RET by 2030. This has been enshrined in legislation (Renewable Energy (Jobs and Investment) Act 2017 (Vic)) and is in addition to the state's previously legislated renewable energy generation target of 40 per cent by 2025.

- Queensland’s renewable energy target of 50 per cent by 2030.

- New South Wales committing to build 12GW of renewable generation through its Electricity Infrastructure Roadmap.

- Tasmania targeting 15,750 GWh of electricity generation from renewable energy sources by 2030 (a target of 150 per cent). It has also legislated for 200 per cent of its current needs to come from renewables by 2040 under the Tasmanian Renewable Energy Action Plan.

- South Australia committing to a 100 per cent net RET by 2030 under its Energy and Mining Strategy.

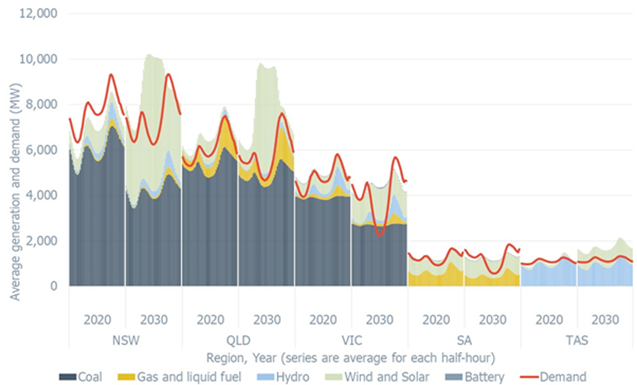

The states have shown a strong appetite to go-it-alone, initially fuelled by the absence of agreement on national climate and energy policy. The potential consequences of this state-by-state approach in terms of the NEM’s overall supply and demand has been highlighted by the work of energy analysts and researchers, Cornwall Insight Australia. They have produced the below graph to illustrate the potential excess supply resulting from meeting the state-based renewable targets.

Figure 1: Time-of-day average generation and demand profile 2020 v 2030

Notes: Time-of-day average generation profile in 2020 versus 2030. Additional renewable capacity needed for the states’ 2030 targets has then been added while the coal and gas plants that are forecast to retire based on Australian Energy Market Operator (AEMO) data have been removed (the recent Yallourn closure announcement is captured here). The average shape for each fuel type is constant. The future demand pattern is based on AEMO’s central forecast for 2030.

Source: Cornwall Insight Australia

Cornwall[i] estimates that by reaching the state-based targets across the NEM there will be nearly 12GW of excess generation waiting to be used in the middle of the average day – with each region having more supply than demand as solar generation hits its peak.

Batteries are touted as one answer. There is a significant volume of battery storage proposals being put forward (see previous EnergyInsider, Big Battery Bonanza). Up to 7GW of batteries have been proposed, but it is not clear if all will proceed, with some projects also requiring government support to reach finalisation. Even assuming all these batteries are built, along with the 2GW of pumped storage from Snowy 2.0, there would still be a shortfall in its capacity to soak up the projected supply.

The Australian Energy Market Operator in its most recent Integrated System Plan (2020) estimated up to 19GW of new dispatchable resources will be needed by 2040 to firm up distributed and utility-scale renewable generation.

Transmission links can help, but as highlighted by Cornwall Insight’s analysis, this may not be the case in the middle of the day when all regions may have excess supply and be looking to export electricity.

One consequence of excess supply that has increasingly become a feature in the NEM is the number of negative price events. Victoria recorded negative prices for 10 per cent of the time during the last quarter of 2020, and South Australia saw negative prices 17 per cent of the time.

On the surface negative pricing might seem like a good thing, but as noted in our EnergyInsider, Dropping demand and plunging prices – can you have too much of a good thing? it is not clear cut, and it increases investor risks.

New large-scale solar and wind are estimated to need to realise average prices over $50/MWh to recover their capital costs. And for investors who moved early and locked in positions when renewable technology costs and interest rates were higher, they need to realise considerably higher prices again.

Wind and large-solar can readily spill generation, which should happen before prices get much below $zero/MWh. However poorly written contractual arrangements can lead to these generators remaining at full output, while the counterparty (potentially a state government) pays the negative price which can go all the way to -$1,000/MWh.

Cornwall Insights argues that to get more from the renewable capacity that is being installed there may be merit in a greater coordination, with states focussing on their comparative advantages:

“For example, rather than focusing on generating more green energy within their own borders, states with better pumped hydro resources could build more of those, which could help manage not just their own, but their neighbour’s excess energy as well. This in turn might support more renewable generation across the whole NEM.”

This perspective, it notes, was the original premise of the NEM “to promote long-term consumer interests through better trade and coordination”[ii].

The task confronting the Energy Security Board is to design a post-2025 grid. The answer to managing the new grid is likely to be a combination of renewables, storage with different durations, transmission links and fast-start gas generators. But to ensure the reliability and resilience of the NEM (and that more advantage can be taken of lower emissions generation) it will require a greater level of coordination than is currently the case.

[i] When less could be more – on the state’s green targets, Franklin Liu, Senior Policy and Regulatory Consultant, Cornwall Insight Australia, 11 March 2021

[ii] ibid

Related Analysis

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Green certification key to Government’s climate ambitions

The energy transition is creating surging corporate demand, both domestically and internationally, for renewable electricity. But with growing scrutiny towards greenwashing, it is critical all green electricity claims are verifiable and credible. The Federal Government has designed a policy to perform this function but in recent months the timing of its implementation has come under some doubt. We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.