by Australian Energy Council

Critical minerals and renewables: The supply challenges

The International Energy Agency (IEA) recently released its flagship report, World Energy Outlook 2021 – its crystal ball look at emerging trends and their potential impact on how energy systems evolve.

While most of the focus is on the total share of energy markets by generation and fuel type, the report also carries some insights into emerging energy security risks as the world moves to lower emissions grids, which the report notes could well be a “bumpy” road.

Traditional risks such as gas supply remain, while new potential hazards will emerge with the shift to increased renewables and low emissions technologies and as a result will likely increase the issues to be managed. Some of the issues highlighted by the IEA include:

- The possibility of investment imbalances and mismatches;

- The need for greater flexibility in power systems;

- New linkages with other aspects of supply such as delivery and storage of different kinds of gases, including hydrogen;

- Potential for bottlenecks as the rollout of solar, wind, batteries, electrolysers and electric vehicles increases globally;

- Ensuring there is access to reliable and affordable energy, and managing social and economic consequences of change given the need for public support for the transition; and,

- The increasing importance of critical minerals with demand expected to rise significantly from today’s levels, fuelled by increased demand for clean technologies (we take a closer look at this, below).

It also flags the potential for additional and increased physical risk to energy infrastructure from climate change and weather-related risks such as cyclones, coastal floods, bushfires, and more limited water supplies.

The latest report highlights, while we assume an orderly process in move to decarbonisation, it could be volatile and disjointed; as the transition accelerates, reliable operation of the energy system will depend on increasingly complex interactions and there will be the risk of destabilising regions and local communities if not well managed.

As we have seen in Australia, rising shares of solar and wind generation bring fundamental changes to how the system operates and must be managed and, according to the IEA, there is the need for “policy makers to mobilise investment in all sources of flexibility in order to maintain electricity security”.

Electricity security

The key challenge as more renewables enter power systems will be continuously matching demand and supply. The expected strong growth in wind and solar generation across the three key scenarios[i] - Net Zero Emissions by 2050 (NZE), Announced Pledges Scenario (APS) and State Policies Scenario (STEPS) - considered by the IEA across all regions, will see a global shift from grids based on dispatchable generation which, as we are witnessing in Australia, will require a shift in the operation of systems.

Australia is in the leading pack with the transition, and its speed is what is behind the Australian Energy Market Operator’s commitment to having the grid capable of managing 100 per cent renewables at times by 2025.

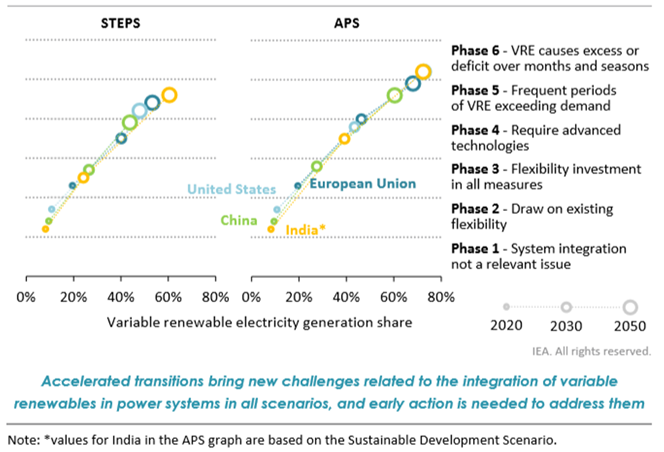

Figure 1 shows the IEA’s projections for the volume of renewables by regions and scenario, as well as the impacts they are expected to have on the energy system based on six phases.

Figure 1: The phases of renewable integration based on scenarios

The report’s APS projected each region to hit phase 4 by 2030, where renewable generation accounts for most or all generation for increasing periods putting greater stress on system management and requiring frequent interventions by system operators. By 2050 all regions are forecast to reach phases 5 and 6 in the APS with longer periods of mismatch between renewable generation and demand with supply needing to be supplemented by dispatchable generation, long-term storage systems or demand management.

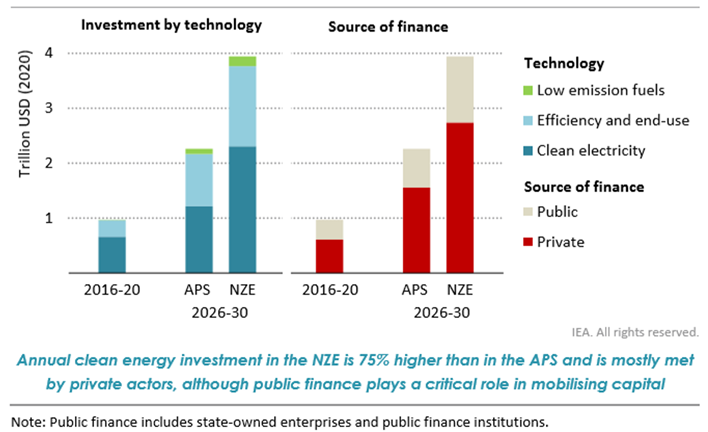

Figure 2 highlights the changing scale of investment in clean technologies, energy efficiency and low emission fuels under two scenarios.

Figure 2: Average annual clean energy investment and financing in the Announced Pledges and Net Zero Emissions by 2050 scenarios

Critical minerals

A particular risk to progress towards a lower emissions system could come from higher or more volatile prices for the critical minerals that are used in the manufacture of solar panels, wind turbines, EV batteries and other technologies. Some of the critical minerals include copper, cobalt, nickel, lithium, and graphite. The IEA believes this risk could slow the progress to lower emission systems or simply make the shift that much more costly.

The agency estimates the average amount of minerals needed for a unit of generation capacity has already increased 50 per cent since 2010 with the growth in renewable technologies. In its STEPS (see endnote) scenario, demand for critical minerals for clean energy technologies are projected to nearly triple between now and 2050. While the report’s NZE scenario would require six times the amount of mineral inputs by 2050; demand from EVs and battery storage is expected to jump by “well over 50-times” in the next three decades, while the projected expansion of networks to complement record levels of clean energy deployment could lead to a doubling of copper demand up to 2050.

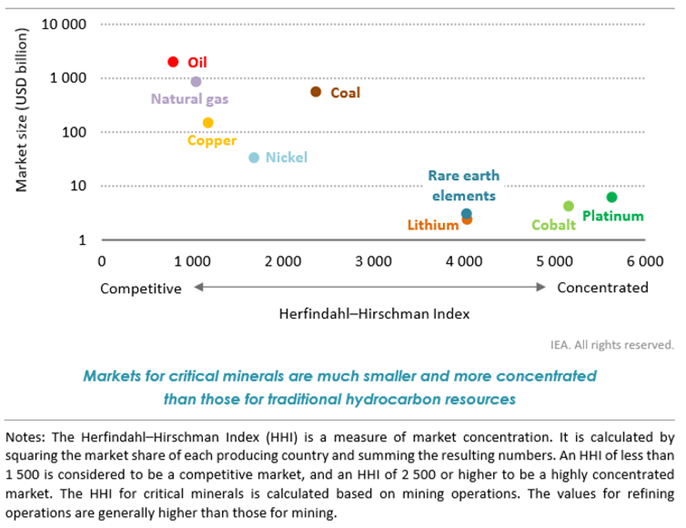

The rapid jump in demand for critical minerals raises questions about availability and reliability of supply with supply very concentrated and the lack of geographical spread in extraction and processing operations:

“For example, the world’s top-three producing nations control well over three-quarters of global output for lithium, cobalt, rare earth elements. The level of concentration is even higher for processing operations, with China having a strong presence across the board”.

Figure 3: Market size and level of geographical concentration for selected commodities, 2019

The supply chain risks for critical inputs, including minerals, was also highlighted earlier this year in a White House report. A risk flagged by the IEA is that any higher and more volatile prices or supply disruptions could hamper global progress on cleaner energy grids or simply make the transition more costly.

Some examples of the impact of critical material costs on technologies and projects included in the Outlook include:

- Solar PV: Silicon makes up 10-15 per cent of module costs; silver 5-7 per cent. The doubling of polysilicon prices since last year (previously covered here) and 30 per cent increase in silver prices cited by the IEA have led to a cost increase of USD 0.04/watt or a 16 per cent rise in module costs, “for a typical 100 megawatt (MW) utility-scale PV project… (it) represents a 4 per cent hike in total project cost on a dollar-per-watt basis”.

- Wind turbines: Turbine materials account for an estimated 15 per cent of the total wind turbine prices over the past decade. Steel prices nearly doubling in China and tripling in the US and copper prices up 50 per cent on last year have led to an 8-10 per cent rise in the cost of turbine manufacture “which could increase total capital costs by around 5 per cent”.

- Grids: Copper and aluminium represent around 14 per cent and 6 per cent of total grid investment respectively, according to the IEA. It notes copper prices have averaged USD9300/tonne in 2021 (currently USD9,878/t), compared to an average price in previous decade of USD7000/tonne. At highest prices, the copper and aluminium share of total grid investment rise to almost 20 per cent and 8 per cent respectively, which is estimated to increase overall grid investment costs by around 9 per cent.

- EV batteries: Lithium (lithium carbonate USD27,500/t) and nickel (USD19,857/t) average prices in the first half of this year increased 20-40 per cent, while cobalt (USD56,585/t) average prices increased by two-thirds, which increases battery costs by 6 per cent.

While it is unclear how long the surge in prices will continue this year, according to the IEA, a rise of the magnitude seen “would generate upward pressure on total capital costs by 5-15 per cent ... (and) could add USD430 billion to cumulative investment needs for solar PV, wind, batteries and electricity networks over this decade in the STEPS, and nearly USD700 billion” in the NZE scenario.

Trading in critical minerals will grow due to the shift to lower emission grids – the IEA calculates the value of key minerals such as copper, nickel, lithium and cobalt will double by 2050 in their APS scenario from USD120 billion today while in the NZE scenario the value would triple to USD400 billion in the same timeframe.

Australia is among Canada, Chile and Peru as a top exporter of critical minerals while China, Japan, Korea and the European Union are the main importing countries – although China accounts for about half of the imports because of its key role in refining.

[i] The main scenarios:

- Net Zero Emissions by 2050 Scenario (NZE), which sets out a narrow but achievable pathway for the global energy sector to achieve net zero CO2 emissions by 2050.

- Announced Pledges Scenario (APS), which assumes that all climate commitments made by governments around the world, including Nationally Determined Contributions (NDCs) and longer-term net zero targets, will be met in full and on time.

- Stated Policies Scenario (STEPS), which reflects current policy settings based on a sector-by-sector assessment of the specific policies that are in place, as well as those that have been announced by governments around the world.

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

The ‘f’ word that’s critical to ensuring a successful global energy transition

You might not be aware but there’s a new ‘f’ word being floated in the energy industry. Ok, maybe it’s not that new, but it is becoming increasingly important as the world transitions to a low emissions energy system. That word is flexibility. The concept of flexibility came up time and time again at the recent International Electricity Summit held in in Sendai, Japan, which considered how the energy transition is being navigated globally. Read more

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.