by Australian Energy Council

Coal exits: What’s in store for batteries?

There has been plenty commentary about the implications of coal plant closures following Origin Energy’s Eraring announcement last week, along with earlier announcements from AGL Energy and EnergyAustralia, as well as the “audacious” bid by Brookfield and Mike Cannon-Brookes for AGL with reported plans to accelerate coal plant closures if successful[i].

The announcement of potential early coal plant closures is significant, but it is also not unexpected by the market. It reflects the reality of the changing energy dynamics in Australia. Our energy market is in the midst of a renewables revolution.

Coal plant is retiring faster than the market operator had previously anticipated and current announcements will see more than 5GW of the current 23GW of coal plant capacity leave the market by 2030[ii]. The Australian Energy Market Operator’s (AEMO) step change scenario in its draft Integrated System Plan forecast coal closures could increase to 14GW by 2030 (although this has been contested), while the level of capacity withdrawal under its slow change scenario would be 10GW based on expectations of lower operational demand.

Energy companies, which invest heavily in renewables as well, know the switch to renewable generation has made life harder for coal-fired power stations. This is because they are a more inflexible generation source – they are designed to turn on and run constantly, which makes them a lot less nimble than gas peakers or other forms of generation. This in turn makes it harder for coal plant to operate in a market which is increasingly dominated by generation from lower cost renewables, but which are also variable depending on weather conditions.

Increasing periods of negative pricing and low operational demand driven by renewables complicates the economics of coal plant that are more limited in their ability to ramp up and down with rapid changes in demand. The Australian Energy Regulator (AER) has asked AEMO to reconsider its assumptions around coal plant operations and the ability to operate flexibly on an intra-day basis, given they are known to adopt different daily load profiles. While this may impact the forecasting of the timing of coal exits, it will not change the overall market dynamics at play.

Currently, the National Electricity Market (NEM) relies on 23GW of firm capacity from coal, and another 20GW of dispatchable firming capacity from storage and gas generation. As coal plants exit the grid they will be replaced by renewables supported by with batteries, pumped hydro and gas generation.

Battery storage and pumped hydro will play an increasingly important role. Large-scale batteries are being proposed to replace capacity as coal plants retire.

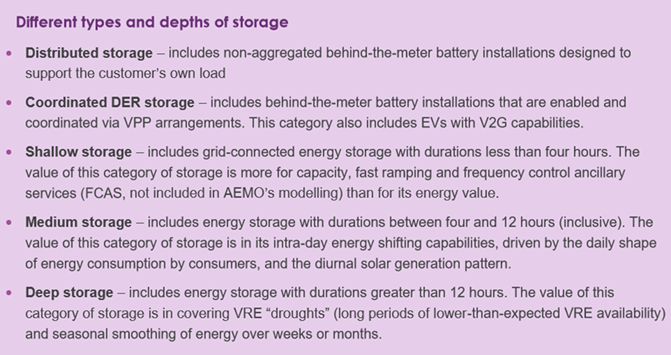

There are multiple types of storage as shown in table 1 below.

Table 1: Types and depths of storage

Source: AEMO Draft ISP 2022

Lithium-ion batteries are effective at providing shallow storage and battery storage systems can be used for a range of network services including load shifting, ancillary services and Frequency Control Ancillary Services (FCAS)[iii].

Aside from small-scale batteries as part of distributed energy resources, there are around 14 large-scale BESS currently in operation or under construction[iv], including the 150MW/194MWh Hornsdale Power Reserve system in South Australia and the Victorian Big Battery (300MW/450MWh) and we are increasingly seeing renewable generation proponents looking at integrating and co-locating them with BESS. Aurecon notes that most new large-scale BESS developments require the support of funding or support mechanisms, but this is expected to reduce as costs fall and energy market price profiles change[v].

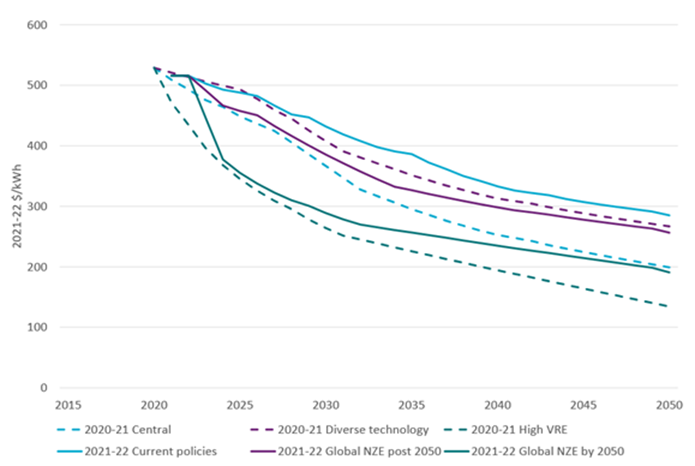

The cost of batteries has come down significantly, and in its latest assessment Aurecon revised the capital cost of large-scale 2-hour duration batteries and projected the future cost trend for these batteries (figure 1) based on various scenarios.

Figure 1: Projected capital costs for 2-hour duration battery by scenario

Source: GenCost 2021-22

Batteries have sustained cost reductions and historical cost reductions came from deployment in areas like electric vehicles and consumer electronics, according to the CSIRO’s 2021-22 GenCost report. It found that battery current costs saw a 5-6 per cent decline in costs over the previous year, while pumped hydro current cost estimates did not change significantly.

Around a third of homes in the NEM have rooftop PV with around 15GW of capacity. In another decade (by 2032), this is expected to increase to more than half of the homes in the NEM and increase to 65 per cent (69 GW capacity) by 2050, and increasingly as the costs improve rooftop systems are expected to be complemented by battery storage. Home batteries are predominantly used to take greater advantage of solar output, but as they increase in numbers there will be potential for aggregation of energy storage. In its work Aurecon estimated home battery costs to be $13,000 for a 5kW/10kWh system or $1300/kWh, including installation – more than twice the cost of large-scale batteries[vi].

The most pressing utility-scale need in the next decade, according to AEMO, will be for 4-12 hour storage to manage variation in output from renewable generation and meet demand as coal leaves the market.

Pumped hydro is the most mature technology for storage and Snowy 2.0 is expected to provide much of the necessary additional storage depth to 2030 (2000 MW/175 hours), but additional deep storage will be required in subsequent decades to support renewables.

Large-scale vanadium redox batteries are considered to have the potential to complement lithium-ion and other storage technologies for medium storage applications. They offer potential longer duration storage (at least 4 hours). The Yadlamalka project in South Australia, supported by the Australian Renewable Energy Agency (ARENA) is expected to be the first grid-scale battery in Australia using the technology, but will still be only 2MW/8MWh. The largest operational battery of this type is a 15MW/60MWh system in Hokkaido Japan. Large-scale flow batteries have a higher capital cost than lithium-ion but have a longer lifespan. Aurecon has estimated the EPC cost of a 5MW vanadium-redox flow storage system to be $21.7 million (grid connected - 4 hour storage) and $21.4 million when col-located with a renewable plant. For an 8-hour system the cost is estimated at $29.1 million and $28.8 million respectively. The relative energy cost was estimated to be $372/kWh for both durations and whether grid connected or co-located.

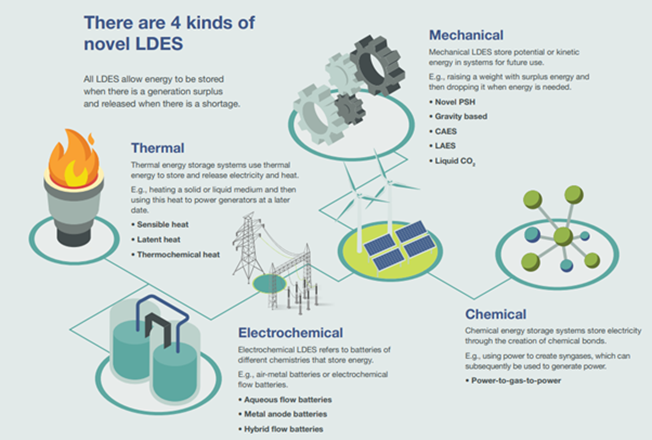

Long-duration energy storage is being flagged as a possible storage solution – there are more than 5GW/65GWh of LDES capacity announced or operational, according to McKinsey Sustainability, which has recently released a report into the potential of the technology. LDES types are shown in figure 2.

Figure 2: LDES types

Source: McKinsey

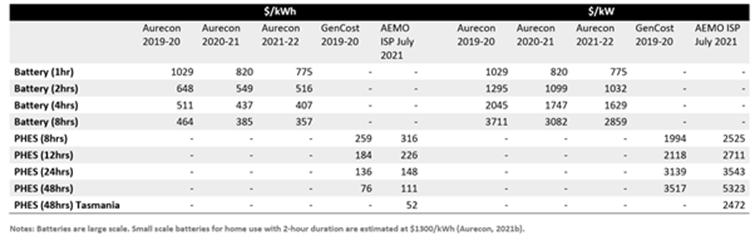

In its most recent GenCost report, the CSIRO provided an update on the cost of storage based on the most common types currently in use and this is shown in the table below.

Figure 3: Storage current cost by source, total cost basis

Source: GenCost 2021-22

The total cost basis means the costs are calculated from the total project costs divided by the capacity in kW or kWh. The $/kWh costs fall with increasing storage duration, while the cost in $/kW increase as the duration increases because the additional duration adds costs without adding any power rating to the system – additional duration is most costly in batteries, so batteries are best placed to manage shorter changes in demand, while pumped hydro storage becomes more competitive with longer duration.

[i] $20bn to reinvent coal-free AGL, The Australian 22 February 2022

[ii] Draft Integrated System Plan, AEMO, December 2021

[iii] Aurecon, 2021 Costs and Technical Parameters Review, Revision 1, October 2021

[iv] Aurecon, 2021 Costs and Technical Parameters Review, Revision 1, October 2021

[v] Aurecon, 2021 Costs and Technical Parameters Review, Revision 1, October 2021

[vi] GenCost 2021-22

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Australia’s Home Battery Surge: A Question of Equity

Australia is a global leader in rooftop solar, with more than 4.3 million households and small businesses installing photovoltaic (PV) systems as of February 2026. Battery uptake has also accelerated, particularly since the introduction of the Cheaper Home Batteries Program in July 2025, which offers around a 30 per cent upfront discount for systems between 5 kWh and 100 kWh. More than 236,000 batteries had been installed by February 2026, although this likely understates the true figure due to reporting lags; the Federal Government has since indicated installations have surpassed 250,000 as of March 2026. Despite this rapid growth, an important question remains: who is actually benefiting from these subsidies?

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.