by Carl Kitchen

Where’s the energy for new gas generation?

The importance of gas-powered generation (GPG) to our energy system is well recognised with system planners and market operators often seeing it as an essential ‘last line of defence’.

The role of gas generation has been further highlighted by two recent papers: the Australian Energy Council’s Energy2050 Vision for the Future Energy System and an energy policy paper “Are gas turbines ‘bankable’ in energy-only markets?” published by Griffith and Cambridge Universities.

Energy2050 highlights that the National Electricity Market (NEM) will still rely on gas-powered generation (GPG) for firming and to fill in for renewable droughts. Our assessment is that during periods when GPG gas demand is high, the gas network, including pipelines and storage will need to be capable of very flexible supply (90PJ annually, but up to 3,000TJ on a peak day, compared to 100-150PJ pa in recent years, and peak demand of around 1,200TJ). The Australian Energy Market Operator (AEMO) expects the ramp up in peak day demand to start in the early 2030s and its draft 2026 Integrated System Plan (ISP) projects that 14 GW of gas-fired generation will need to be in place by 2050. This accounts for the replacement of all current mid-merit plants (4 GW) and nearly all of the existing 8 GW of peaking gas plant.

Despite these forecasts and expectations, and a general acceptance of the critical role gas will have to play in a renewables-dominated system, there appears to be investor reticence to invest in gas plants in the NEM. For example. AEMO’s generation data shows that only 574 MW out of the 6830 MW of publicly announced gas-fired projects are actually anticipated.

The anticipated gas plants according to AEMO’s generation data are:

- Brigalow Kogan Creek (400MW) with a target date of 31 December 2028.

- Dubbo Firming Power Station (listed at 57MW), which does not have a firm date.

- Lockyer Valley Energy Project, near Grafton (117MW OCGT) with a target date of 30 September 2030.

Anticipated projects are those that are sufficiently progressed towards meeting at least three of the five commitment criteria (see figure 1 below) used by AEMO, so they still have some way to go before becoming a committed project.

Figure 1: Project Criteria

Source: AEMO

Currently there is only Snowy Hydro’s 750 MW Hunter Power Project in commissioning phase in New South Wales and AEMO’s data does not show any other committed natural gas projects currently, aside from 6 MW (this likely refers to the Mugga Lane Renewable Hybrid plant which runs on biogas). Two of the major gas plants - Hunter Power Project and Brigalow Kogan Creek - are government-backed.

In his recent paper – “Are gas turbines “bankable” in transitioning energy-only markets?” – Professor Paul Simshauser[i] considers why, given both pending coal plant closures and the need for reliable, dispatchable supply in a renewables-dominated grid, that we have not seen more gas turbine (GT) investment appearing in the National Electricity Market.

Prof. Simshauser’s paper reinforces the central importance of gas plants and writes “all power system planners consider gas plants to be an indispensable ‘last line of defence’ in maintaining a power system in a secure state” and that alternatives like batteries can be quickly exhausted during periods of low wind and solar output.

“At this point, some form of dispatchable generation without an energy constraint is required. For this purpose, the GT is frequently a least cost option. Their comparatively low capital cost (with high marginal running costs) makes GTs ideally suited to peaking duties.”

When considering the bankability of gas power plants, the paper’s modelling finds that a merchant GT operating in a transitioning energy-only market and relying solely on spot market revenues is problematic. However, when combined with cap derivatives from forward markets, the investment appears viable with “a tractable result” emerging. So what does the paper attribute the lack of proposals to?

Three policy and government-related issues are seen as weighing on investment decisions:

- Policy uncertainty around natural gas;

- This uncertainty has been “amplified” by the Federal Capacity Investment Scheme (CIS) which specifically excludes GTs in favour of batteries; and,

- Coal closures that have been delayed or are seen to be at risk of being delayed in the NEM’s three biggest regions – New South Wales, Victoria and Queensland – because of government interventions.

The paper notes investors in the NEM have no experience of a bipartisan, integrated energy and climate policy framework.

The CIS does not include gas generation even though there is no “theoretically grounded reason in energy economics or energy policy” for excluding gas plants from the underwriting scheme. The CIS instead supports utility-scale batteries. Batteries can play an important role, particularly given the number of solar installations Australia has, and they can reduce renewable generation curtailment and shift low-cost energy to evening peaks.

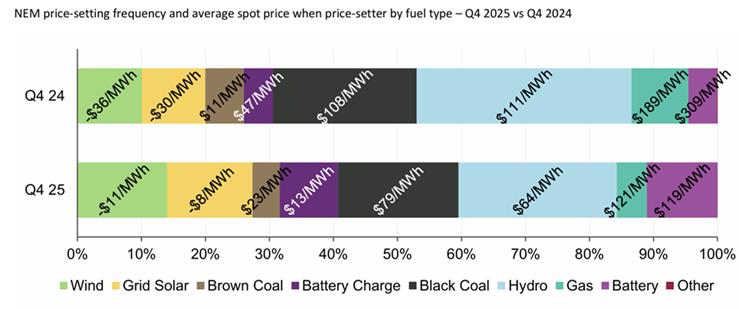

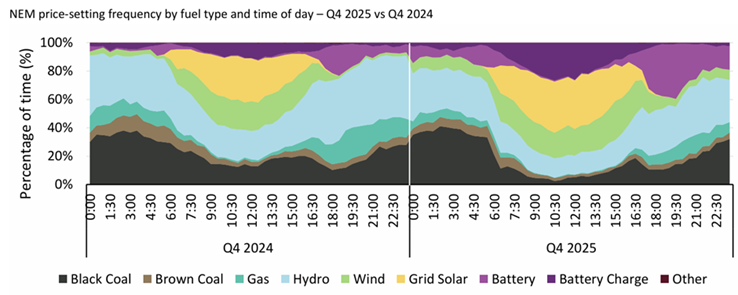

But batteries will also reduce the amount of gas back up needed. AEMO’s Quarterly Energy Dynamics (QED) reports are showing that batteries are increasingly involved in price setting in the wholesale market in high price periods, traditionally the role played by peaking gas generators. For example. the QED for the fourth quarter last year showed growth in the price setting role of batteries (see figures 2 and 3).

Figure 2: Price setting and prices by fuel type Q4 2024 and Q4 2025

Source: AEMO QED Q4 2025

Figure 3: Price setting frequency by fuel type

Source: AEMO QED Q4 2025

Batteries are “unlikely to replace the fundamental ‘capacity need’ for unconstrained primary generating capacity”, according to Prof Simshauser’s paper. Batteries store and don’t generate energy and “therefore cannot resolve structural renewable energy shortages during critical event days or winter periods” and short duration batteries can’t “defend $300 Caps” at nameplate capacity.

Coal plant closures present a material issue for gas plants, the paper notes.. The size of coal plants “makes them a significant variable in any investment equation – creating a chicken and egg policy problem. Three years of visible $300 Cap premiums in forward markets may not convince a Board of Directors to make a 30+ year GT investment commitment when utility planning models are telegraphing a material lack [of] volatility because of coal closure delays”.

The AEC’s Energy2050 vision for the future energy system also highlights regulatory uncertainty as a major challenge for the next 20 years, along with ensuring sufficient gas supply to meet demand (rather than managing the consequences of very rapid demand decline). At the same time new supply remains challenging in the context of a broader drive to decarbonise and jurisdictional policies that limit the scope for new development.

It argues that if maintaining a gas network post-transition just to supply gas peaking capacity on rare occasions appears unviable, we may have to consider alternatives such as diesel or potentially more longer-term storage – though it would be valuable to have at least one external fuel source contributing to electricity reliability (see Box 1 below). If gas is still playing a bigger role – for example longer-term seasonal shifting to meet winter supply/demand gaps, then a functioning gas network that can recover its costs remains essential.

Box 1: Firming the last MW

|

An ongoing role for GPG in the system is predicated on having a gas transportation system that is flexible enough to deliver large volumes of gas on a handful of peak days and potentially very little at other times. If there is little role for gas in daily firming (because there is sufficient storage or demand flexibility for example), and if there are few other gas users (if electrification pathways for industrial users improve), then it may prove inefficiently expensive to maintain a gas network primarily for occasional GPG use. If this scenario appears likely to emerge before 2050, then we will need to consider alternative ways to keep the power system going through renewable droughts. Options include: Diesel – As an energy-dense liquid, diesel can be transported by truck and is easier to store on site than natural gas. While diesel would usually be considered a more expensive peaking option than natural gas, under this scenario, it could prove better value as it doesn’t require its own transportation network. From an emissions perspective, the amounts consumed would be relatively low and biodiesel may be an option. It is also worth noting that diesel supply and cost can be subject to external shocks, as we are currently witnessing with the Iran conflict. Long duration energy storage (LDES) – while having an independent fuel vector is somewhat desirable from a system resilience perspective, we may be able to achieve reliability with LDES, providing we have enough of it to cover an extended renewable drought. Obvious options for the LDES technology are pumped hydro and long duration batteries, though there are other emerging technologies. The key to success is to ensure that sufficient capacity is held in reserve, which constrains the storage operator from maximising their opportunities in diurnal or other short-term storage situations. Green hydrogen – as hydrogen is less dense than natural gas, it is more challenging to store and transport. So, this is only likely to be a viable option if there is an extensive hydrogen network being set up for industrial heat in any case. Assuming hydrogen production is via electrolysis, then it is effectively another form of storage rather than an independent fuel source. Regardless of which technologies prove the most cost effective, critically we need to find ways to reward plant for ensuring it is available in rare cases (and potentially only then). Ideally the market will find a way to reward such plants, but this will depend on the reliability settings. An alternative may be to establish a reserves procurement process, whether centralised or decentralised, separate from the spot market. |

Aside from regulatory uncertainty there are also supply chain issues and increasing lead times for development of gas projects. Global research firm Wood Mackenzie has reported that lead times for GTs has been rising as demand grows, particularly in the US and on the back of development of data centres.

“As of last year, the average lead time for delivery of a gas turbine was almost five years after receipt of order, Wood Mackenzie’s Supply Chain team found. Lead times may have edged up slightly since then. In 2021, the average was only about two years.”

Major gas turbine manufacturers such as GE Vernova, Siemens Energy and Mitsubishi Heavy Industries, have all announced significant capacity expansions since the start of last year and Wood Mackenzie is forecasting lead times should start to drop by 2027, as additional manufacturing capacity ramps up. “But that is not expected to have much impact on generation capacity additions until 2030 and beyond.”[ii]

Supply chain issues may be a contributing factor to a slower than expected rollout of new gas projects but are not the root cause of the seeming inertia in Australia.

Rather financial risk, as a result of an increasingly renewables dominated grid, the growth of large-scale battery storage, and government policy settings, is the major factor. Given that, we are likely to need to find ways to reward plant for ensuring it is available even as the requirement for it can expect to become increasingly rare (and potentially only then). In an ideal world the market would find a way to reward such plants, but this will depend on the reliability settings. An alternative may be to establish a reserves procurement process, whether centralised or decentralised, separate from the spot market.

[i] Paul Simshauser is also CEO of Iberdrola Australia and was CEO of Powerlink Queensland. He is a Professor of Economics at Griffith University’s Centre for Applied Research in Energy Economics and Policy (CAEEPR).

[ii] https://www.woodmac.com/blogs/energy-pulse/supply-chain-constraints-limit-the-growth-of-gas/#:~:text=As%20of%20last%20year%2C%20the,was%20only%20about%20two%20years.

Related Analysis

From Energy to Flexibility: Rewiring Australia’s Wholesale Markets for Net Zero

Australia’s path to net zero will depend not only on new technologies, but on fundamentally reshaping the markets that underpin the energy system. As coal exits, renewables, storage and consumer energy resources will drive a far more dynamic and decentralised National Electricity Market, where flexibility becomes the critical commodity. We explore the market reforms, investment signals and system changes required to deliver a secure, affordable and reliable Energy2050 future, themes that will also sit at the centre of the Australian Energy Council Conference 2026 in Sydney on 4 June.

Global oil shock, but local calm - how the NEM is holding steady

Whilst Australia is lucky to be located well away from the horrors of the war in Iran, we are witnessing some economic impact with higher petrol and diesel prices. However, can there be impacts on the electricity market as well? In short, yes, but at this stage these impacts are minimal. We take a look at how the oil price could impact the electricity market and what the market has observed so far. Read more.

Energy2050: Building the ‘Light on the Hill’ for Australia’s Net-Zero Future

Today, we are pleased to publish an important report for the Australian Energy Council and the energy industry. Energy2050 is intended to be a vision statement, providing a practical illustration of what it will take to deliver a net zero energy system while balancing affordability, reliability and sustainability. Read more.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.