by Australian Energy Council

Market assessment highlights evolving market

In late July, the Australian Energy Market Operator published their analysis of the wholesale market for Q2 of this year. While the media headlines trumpeted price rises of 31 per cent, the report itself paints a much more restrained picture of the state of the market. As the AEC pointed out at the time, the report illustrates a stabilisation when compared with this time last year, with the industry in a much better position heading into Winter than it was in 2022. We take a look at some of the report’s findings.

Minimum demand records were again set in the National Electricity Market (NEM) in the second quarter this year and total generation increased 143MW (0.6 per cent) compared to the same quarter a year ago, according to the latest energy market assessment.

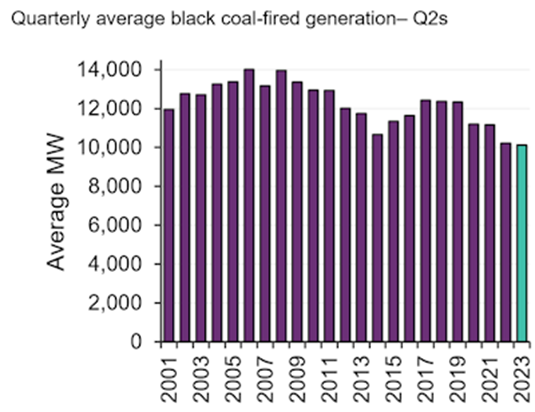

The Australian Energy Market Operator’s Quarterly Energy Dynamics report shows that coal and gas-fired generation continued to decline throughout the quarter, which also saw the retirement of the Liddell Power Station. Black coal-fired generation was 10,121 MW, its lowest Q2 output since NEM start (see figure 1 below).

Figure 1: Q2 Black coal-fired generation 2001-2023

Source: AEMO

While plant availability was up 3 per cent quarter-on-quarter, daytime coal generation decreased as a result of the higher penetration of renewables and showed a marked decline in the middle of the day as shown in Figure 1 below. Only the Eraring Power Station in NSW increased output, with additional generation being utilised in the evenings and overnight when renewable generation was lower.

Figure 2: Daytime coal-fired generation

Source: AEMO

Black coal output declined in Queensland by 174 MW quarter-on-quarter due to a number of outages across the fleet, notably at Tarong North and Callide C.

Increased plant availability at Loy Yang A & B and Yallourn power stations led to a 2 per cent increase in brown coal generation (76MW) during the quarter. While there was increased availability only Yallourn recorded an increase in generation of 151MW for the period.

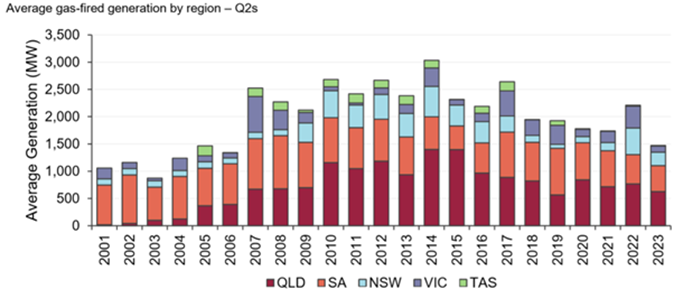

Gas-fired generation declined by 742 MW to its lowest level since 2006 on a quarter-on-quarter basis as a result of additional renewable output and lower spot electricity prices compared with Q2 2022.

Figure 3: Gas-fired generation

Source: AEMO

Hydro generation across the NEM declined 272MW or 12 per cent quarter-on-quarter to an average of 1,967MW. This was due to a number of factors including a lower incidence of spot prices exceeding $300/MWh – a price point at which owners of hydro plant have sold cap contracts will typically offer significant volumes of supply and some plant being on a scheduled outage (McKay station). It is worth noting that hydro generators tend to maintain agreed water levels as part of their upstream water management strategy throughout winter in order to be able to offer adequate supply to the market during summer peaks.

Variable renewable generation increased. 1,176 MW of additional grid-scale solar and wind and distributed solar PV output offset decreases in coal and gas in terms of average output. More than half of the increase (53 per cent) was from wind and 47 per cent came from grid-scale solar. Solar output was up in every state, with the largest increase in Queensland (69 per cent higher than Q2 2022).

New Connections

Additionally, 337MW of additional capacity was available from newly connected wind farms across the NEM and a further 332MW of additional capacity available during the quarter from newly connected grid-scale solar with the bulk of this coming from 10 solar projects (227MW) in Queensland that either recently connected or were being commissioned.

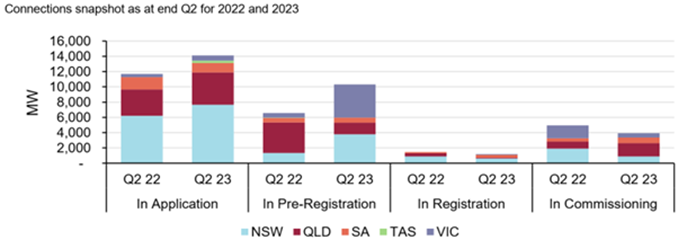

With an increased focus on the speed of the energy transition publicly, the market operator has included a new section to its reporting to show the progress of new grid connections as well as the level of approvals made for new connections.

There was 30GW of new capacity progressing through the connection process from application to commissioning at the end of the second quarter, up from 25GW at the end of Q2 2022.

Figure 4: Increases in number of applications received and projects under construction (pre-registration)

Source: AEMO

AEMO has reported receiving another 16 new applications, totalling 3.9GW, in the current quarter to commence the connection process. At the end of Q2 2023 there were 10.3 GW of plant at various stages of construction (pre-registration), compared to 6.5 GW at the end of Q2 2022. The number of connections progressing through registration and commissioning has remained similar to the previous corresponding period. There was 1.2GW going through registration and 3.9GW of plant being commissioned in Q2 2023. This compares to 1.5GW and 5GW last year. Common issues currently reported to be impacting construction timelines include the need for refinancing, and factors associated with supply chain issues - long lead times for equipment, and the need to change original equipment manufacturers.

The market operator noted there was a significant increase in the number of new connection applications approved in 2022-23 compared to the previous financial year and notes that by the end of the FY23:

- 2.4GW of plant had been approved over the year for market registration to commence commissioning, down 32 per cent than FY22 (3.6GW).

- There was a 21 per cent increase in capacity that completed commissioning and was approved for full operation (2.9GW), compared to a year earlier (2.4GW).

Figure 5: Increase in connection applications approved

Source: AEMO

Interconnector Flows

Total inter-regional energy transfers in Q2 2023 were up 14 per cent (3,516GWh) compared to Q2 2022. The Queensland-New South Wales interconnector (QNI) and Basslink, between Tasmania and Victoria accounted for the bulk of this increase. Net flows across jurisdictions remained similar to Q2 2022, although net flows between Queensland and New South Wales averaged 52MW more southward.

The second quarter did see increased northern flows from Victoria into NSW on the VNI interconnector. Even though the northern state generally had higher prices in both Q1 and Q2, Q2 saw increased northward flows. The flows were restricted by export limits in Q1 and these were especially low during the middle of the day. It has previously been acknowledged both by the Australian Energy Regulator (AER) and AEMO that VNI is being regularly constrained during the day when certain solar farms are generating. The impact of this will be most noticeable in the sunnier months and the middle of the day. We have also previously written about the VNI flows (see Victoria to NSW Interconnector, a functionally impaired asset?) and noted that from 15 March 2023 AEMO split the X5 constraint into two constraint equations and may also have been a factor. It will be interesting to note if this has a noticeable impact on Q1 2024.

Figure 6: VNI Export Limits

Source: AEMO

All in all, the QED highlights a market that is continuing to evolve. While the situation is more stable than last year, higher prices will be a feature of the system for some time to come.

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Where’s the energy for new gas generation?

The importance of gas-powered generation (GPG) to our energy system is well recognised, with system planners and market operators often seeing it as an essential “last line of defence.” The role of gas generation has been further highlighted by two recent papers: the Australian Energy Council’s Energy2050 Vision for the Future Energy System and the policy paper “Are gas turbines ‘bankable’ in energy-only markets?” published by Griffith and Cambridge Universities. Despite this clear and ongoing need, investment in new gas-fired generation remains limited, raising important questions about market settings, policy signals and the future role of dispatchable capacity in a transitioning grid — we take a look.

Integrated System Plan – What Should We Expect?

The release of an expert study of last year’s autumn wind drought in Australia by consultancy Global Power Energy[i] this week raised some questions about the approach used by the Australian Energy Market Operator’s in its 2024 Integrated System Plan (ISP). The ISP has been subject to debate before. For example, there has previously been criticism that some of the ISP’s modelling assumes what amounts to “perfect foresight” of wind and solar output and demand[ii], rather than a series of inputs and assumptions. The ISP is produced every two years and with the draft of the next ISP (2026) due for release soon, it is useful to consider what it is and what it is not, along with what the ISP seeks to do.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.