by Ben Skinner

NEM: Technology and policy shifting the market

The National Electricity Market (NEM) is presently subject to numerous proposals for government interventions. It appears much of the genesis for these interventions is driven by a common view in government and regulators that the market is insufficiently competitive, with vertically and horizontally integrated firms in generation and retailing.

The Australian Energy Council asked respected economist, Rajat Sood, then of Frontier Economics, to contemplate this issue, particularly with a focus on future developments.

What his report found is very significant[i]. The widespread presumptions of imperfect competition derive from a historical paradigm of large generators supplying electricity in one direction to unresponsive consumers. However, profound technological and policy shifts are underway that are radically shifting that paradigm.

In short, the report found that recent and upcoming changes to electricity generation and storage technology, market architecture and supporting infrastructure, like transmission investments, are likely to mitigate medium-term price cycles in the NEM and resolve many of the pressures that provoked market interventions.

The market was designed to balance supply against demand at all times and pricing was largely a signal to change investment in supply rather than to change demand. And because supply sources were lumpy and slow to build, the market would effectively lurch between “feast and famine”. Wholesale prices went through major cycles which was problematic for stakeholder acceptability, even if these outcomes reflected the market operating as designed given the historical industry paradigm. It was inevitable that firms would structure their businesses to better manage these risks, including development of the gentailer model – businesses that have both retail portfolios and generation assets.

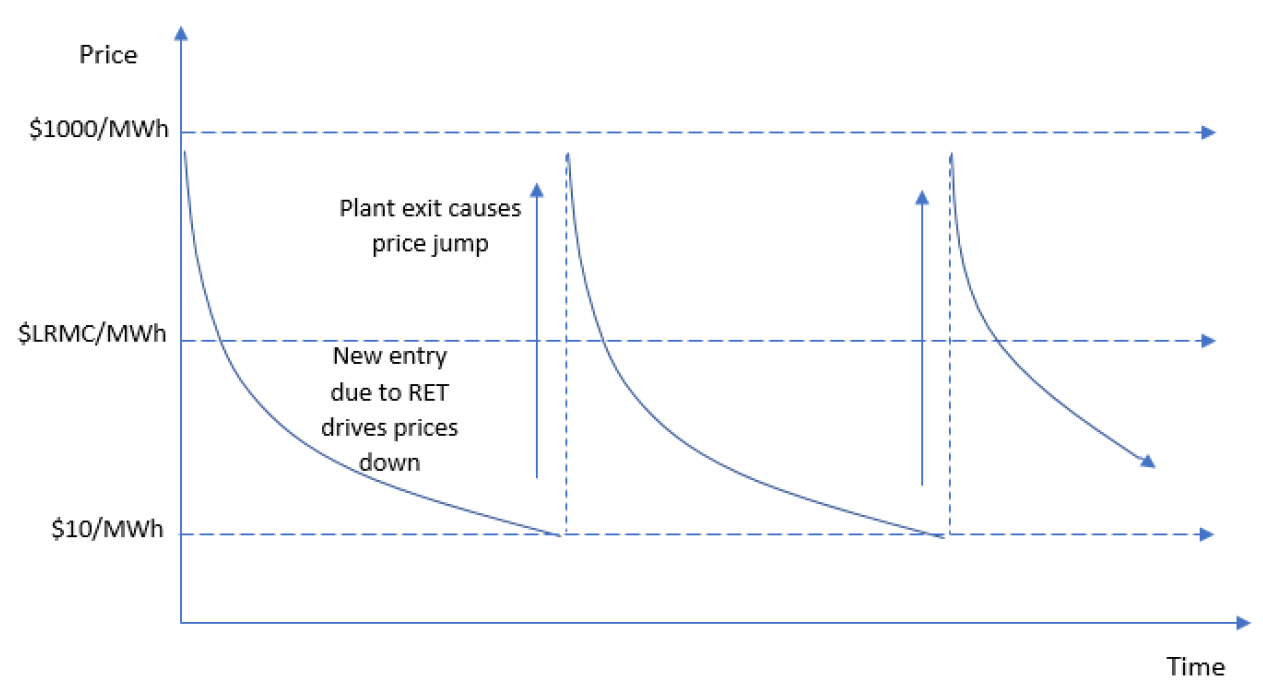

Figure 1: Recent RET-driven price-cycle dynamics

Source: Frontier Economics, 2018

The figure above illustrates this issue in the context of low prices triggering the closures of Northern and Hazelwood power stations. Note the large step changes in wholesale prices when supply changes followed by a long period of high prices and before new supply restarts the cycle. What is overlooked, and what is highlighted by Rajat Sood’s work, is that recent and upcoming changes to electricity generation and storage technology, market architecture and supporting infrastructure are likely to mitigate not only these medium-term price cycles, but also the scope of generators to lead to short-term price spikes. That in turn alleviates much of the push for the kind of interventions that have been put forward and that often lead to unforeseen consequences (which in turn prompt calls for further intervention – a less-than-virtuous circle).

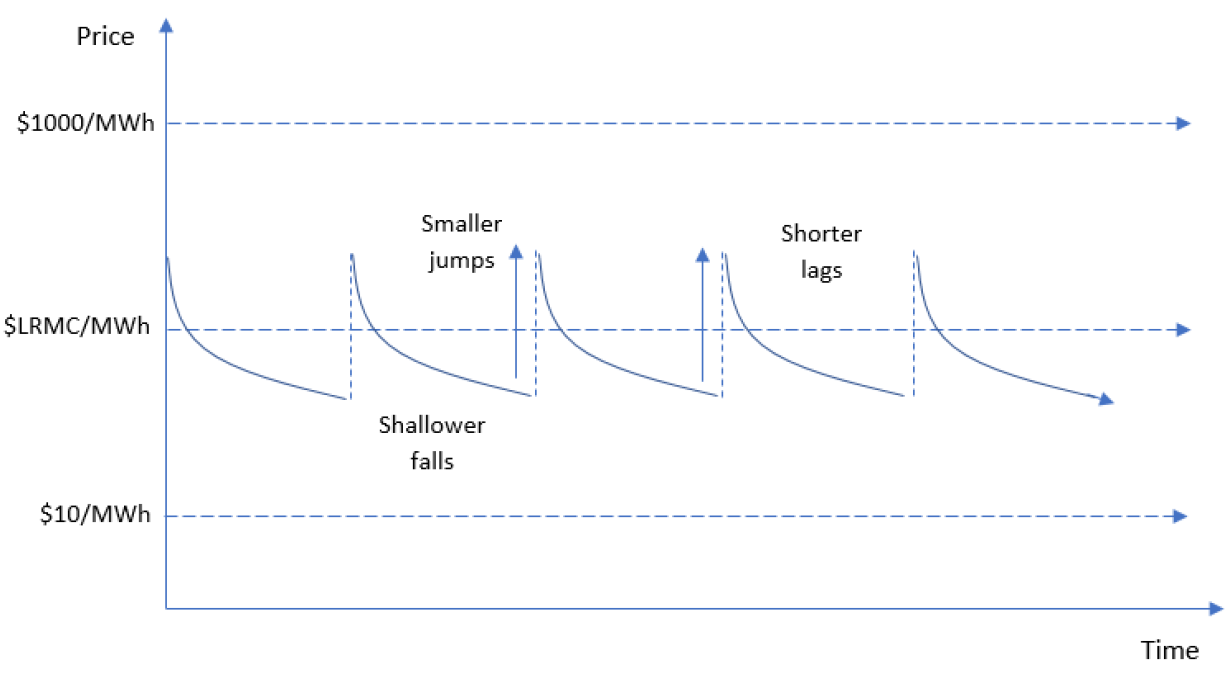

Figure 2: Future RET-driven price cycles in the NEM  Source: Frontier Economics, 2018

Source: Frontier Economics, 2018

Figure 2 illustrates the smaller steps that would be expected in the market of the future and the quicker recovery to a level of equilibrium and reasonable prices. This is cause for some optimism about future stakeholder acceptability.

The report notes that the types of changes that are forthcoming or likely to occur over the next few years include:

- The availability of renewable plant in much smaller increments, reflecting much smaller scale efficiencies than traditional generators, and the much shorter lead times for commissioning such plant. These developments will make it easier for small non-vertically-integrated retailers and business customers to sponsor the entry of new plant.

- Substantial reductions in the costs of utility-scale solar thermal plant and battery storage, in particular.

- More transmission investment across the NEM to reduce network constraints and facilitate the movement of power from ‘renewable energy zones’ to demand centres.

- Detailed changes to the operation of the NEM to change bidding incentives and promote dispatchable demand response from smaller customers.

- A new obligation on generators to notify the market of their intention to exit three years in advance of closure.

- Smarter metering and energy management systems combined with further increases in rooftop PV and distributed batteries to increase the real-time ability of demand to respond to high wholesale prices.

- The possibility of a liquefied natural gas (LNG) import terminal in the southern part of the NEM (there are currently three proposals for import terminals) helping to diversify fuel supplies and increase competition.

This combination of technological, economic and policy-driven changes is likely to have a very significant effect on participant short and longer-term decision-making and on medium-term price cycles.

These kinds of developments, according to the report, are likely to offer these major benefits from the perspective of policy-makers and regulators:

- They should help smooth wholesale price volatility in both the short term and in the medium to longer term;

- They should reduce the advantages of the vertically-integrated ‘gentailer’ business model; and

- They should encourage more competition in the NEM wholesale market.

When contemplating interventions, policy makers should be considering their application to the industry of the future, rather than that of the past.

[i] NEM structure in light of technology and policy changes, Report for the Australian Energy Council prepared by Rajat Sood, Frontier Economics, 13 December 2018

Related Analysis

Addressing Energy Affordability Needs More Than Short-Term Relief

The conflict in the Middle East has continued to highlight the challenges we face in ensuring energy supply remains accessible and affordable for everyone. Ensuring Australia becomes more resilient to international energy price shocks will dominate the energy policy landscape for some time, and rightfully so. But while political debate often gravitates toward regulatory interventions and subsidies that deliver short term household bill relief, the real solution lies in something far more complex: reshaping how the energy system works for consumers. What’s increasingly clear is that energy affordability is not just about price - it’s about design. That is why the AEC is releasing its Affordability Action Agenda today – an 8-point plan of critical actions that industry and governments need to take to ensure that energy remains accessible and affordable for all Australians. Read more.

Efficient Pricing in an Uncertain Energy Market

Electricity prices are once again front of mind for Australians, and with cost-of-living pressures mounting, expectations for fair and transparent pricing are entirely reasonable. But as reforms to the Victorian Default Offer and Default Market Offer evolve, a more complex challenge emerges: how to keep prices in check without undermining the stability, competition and investment needed to sustain the energy system over time. Striking that balance is at the heart of current reform debates, and will ultimately determine whether today’s affordability measures support or weaken the system in the long run. Read more.

The Shadow of the Safety Net: Who Pays for Fairness?

Fairness is a defining Australian value, and it sits at the heart of Victoria’s Getting to Fair strategy aimed at improving equity in essential services. While the Australian Energy Council strongly supports helping people in vulnerable circumstances, funding social equity programs through energy bills risks creating hidden cross-subsidies that place additional pressure on households already struggling with affordability. We take a look at why a more transparent, tax-funded model, combined with retailers acting as delivery partners, may provide a more sustainable and genuinely fair pathway to supporting vulnerable customers.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.