by Ben Skinner

NEM: Technology and policy shifting the market

The National Electricity Market (NEM) is presently subject to numerous proposals for government interventions. It appears much of the genesis for these interventions is driven by a common view in government and regulators that the market is insufficiently competitive, with vertically and horizontally integrated firms in generation and retailing.

The Australian Energy Council asked respected economist, Rajat Sood, then of Frontier Economics, to contemplate this issue, particularly with a focus on future developments.

What his report found is very significant[i]. The widespread presumptions of imperfect competition derive from a historical paradigm of large generators supplying electricity in one direction to unresponsive consumers. However, profound technological and policy shifts are underway that are radically shifting that paradigm.

In short, the report found that recent and upcoming changes to electricity generation and storage technology, market architecture and supporting infrastructure, like transmission investments, are likely to mitigate medium-term price cycles in the NEM and resolve many of the pressures that provoked market interventions.

The market was designed to balance supply against demand at all times and pricing was largely a signal to change investment in supply rather than to change demand. And because supply sources were lumpy and slow to build, the market would effectively lurch between “feast and famine”. Wholesale prices went through major cycles which was problematic for stakeholder acceptability, even if these outcomes reflected the market operating as designed given the historical industry paradigm. It was inevitable that firms would structure their businesses to better manage these risks, including development of the gentailer model – businesses that have both retail portfolios and generation assets.

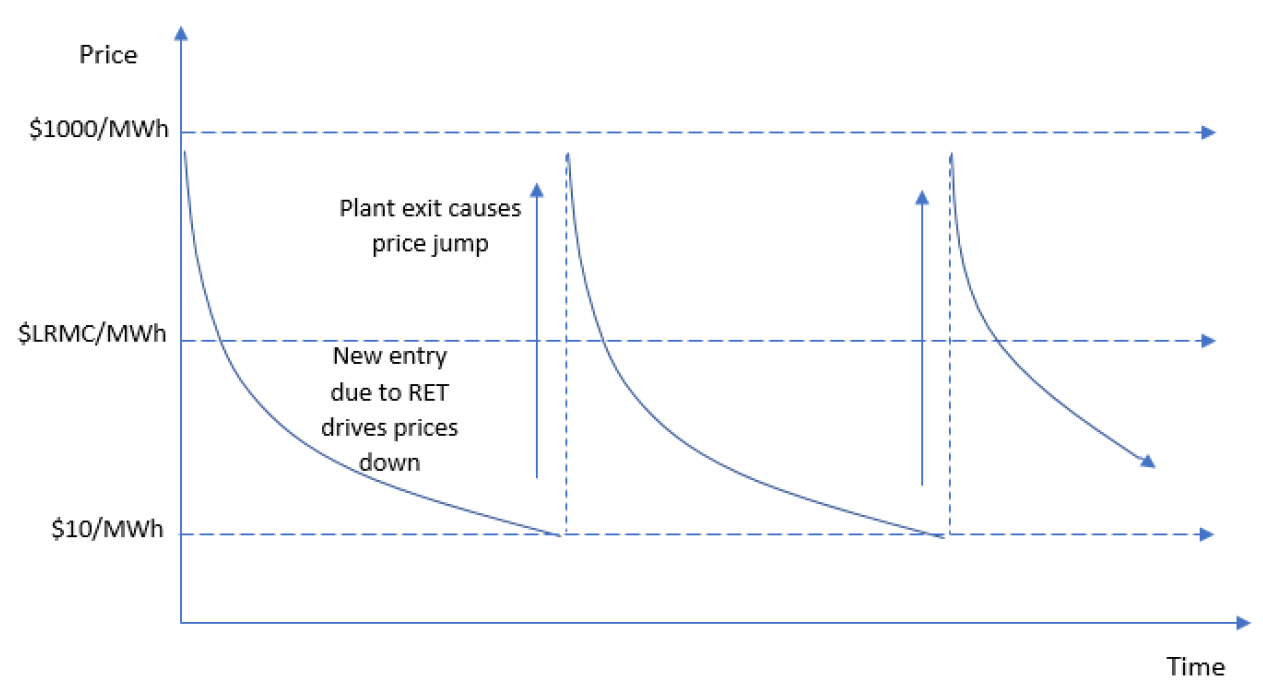

Figure 1: Recent RET-driven price-cycle dynamics

Source: Frontier Economics, 2018

The figure above illustrates this issue in the context of low prices triggering the closures of Northern and Hazelwood power stations. Note the large step changes in wholesale prices when supply changes followed by a long period of high prices and before new supply restarts the cycle. What is overlooked, and what is highlighted by Rajat Sood’s work, is that recent and upcoming changes to electricity generation and storage technology, market architecture and supporting infrastructure are likely to mitigate not only these medium-term price cycles, but also the scope of generators to lead to short-term price spikes. That in turn alleviates much of the push for the kind of interventions that have been put forward and that often lead to unforeseen consequences (which in turn prompt calls for further intervention – a less-than-virtuous circle).

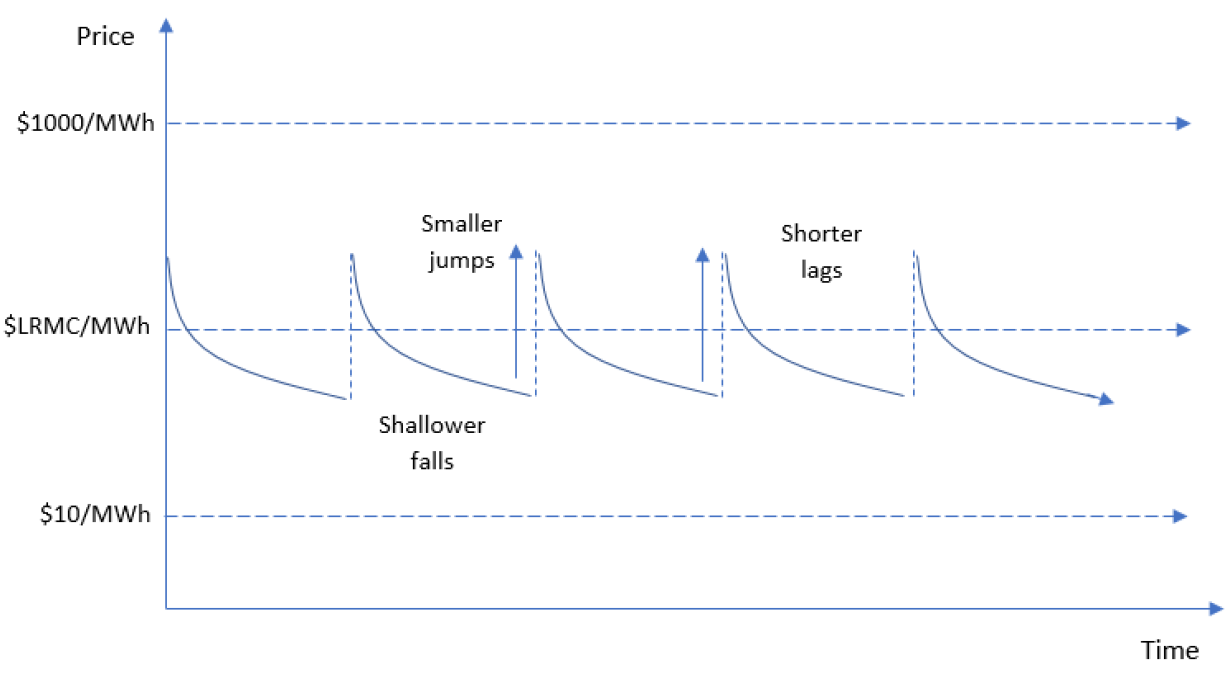

Figure 2: Future RET-driven price cycles in the NEM  Source: Frontier Economics, 2018

Source: Frontier Economics, 2018

Figure 2 illustrates the smaller steps that would be expected in the market of the future and the quicker recovery to a level of equilibrium and reasonable prices. This is cause for some optimism about future stakeholder acceptability.

The report notes that the types of changes that are forthcoming or likely to occur over the next few years include:

- The availability of renewable plant in much smaller increments, reflecting much smaller scale efficiencies than traditional generators, and the much shorter lead times for commissioning such plant. These developments will make it easier for small non-vertically-integrated retailers and business customers to sponsor the entry of new plant.

- Substantial reductions in the costs of utility-scale solar thermal plant and battery storage, in particular.

- More transmission investment across the NEM to reduce network constraints and facilitate the movement of power from ‘renewable energy zones’ to demand centres.

- Detailed changes to the operation of the NEM to change bidding incentives and promote dispatchable demand response from smaller customers.

- A new obligation on generators to notify the market of their intention to exit three years in advance of closure.

- Smarter metering and energy management systems combined with further increases in rooftop PV and distributed batteries to increase the real-time ability of demand to respond to high wholesale prices.

- The possibility of a liquefied natural gas (LNG) import terminal in the southern part of the NEM (there are currently three proposals for import terminals) helping to diversify fuel supplies and increase competition.

This combination of technological, economic and policy-driven changes is likely to have a very significant effect on participant short and longer-term decision-making and on medium-term price cycles.

These kinds of developments, according to the report, are likely to offer these major benefits from the perspective of policy-makers and regulators:

- They should help smooth wholesale price volatility in both the short term and in the medium to longer term;

- They should reduce the advantages of the vertically-integrated ‘gentailer’ business model; and

- They should encourage more competition in the NEM wholesale market.

When contemplating interventions, policy makers should be considering their application to the industry of the future, rather than that of the past.

[i] NEM structure in light of technology and policy changes, Report for the Australian Energy Council prepared by Rajat Sood, Frontier Economics, 13 December 2018

Related Analysis

Ireland’s Green Energy Rule: What Can Australia Learn From Its Approach to Data Centres?

A recurring theme at the Australian Energy Council’s inaugural Energy2050 Conference was the challenge of managing the rapid growth of data centres and their increasing electricity demand. While data centres present a significant economic opportunity for Australia, policymakers are grappling with how to support investment while minimising impacts on customers, the electricity system, and emissions. We take a look at Ireland’s recently introduced data centre policy and explore the lessons it may offer for Australia.

From Energy to Flexibility: Rewiring Australia’s Wholesale Markets for Net Zero

Australia’s path to net zero will depend not only on new technologies, but on fundamentally reshaping the markets that underpin the energy system. As coal exits, renewables, storage and consumer energy resources will drive a far more dynamic and decentralised National Electricity Market, where flexibility becomes the critical commodity. We explore the market reforms, investment signals and system changes required to deliver a secure, affordable and reliable Energy2050 future, themes that will also sit at the centre of the Australian Energy Council Conference 2026 in Sydney on 4 June.

Beyond the Rules: Lessons from the UK on Supporting Energy Consumers Experiencing Vulnerability

Customer vulnerability in the energy sector rarely follows a predictable path, often emerging through financial pressure, illness or sudden life disruption. The United Kingdom’s experience shows that early intervention, flexible support, trusted communication and coordinated care can significantly improve outcomes for households at risk. We explore what Australia can learn from the UK’s evolving approach to supporting customers experiencing vulnerability.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.