by Justine Lovell

EU hydrogen blending: Is it the right mix?

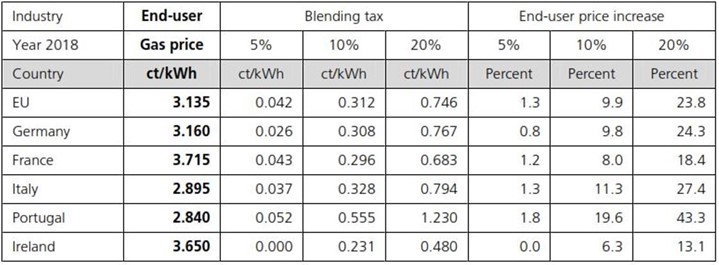

A recent study on the use, limitations and cost of hydrogen blending in the European gas grid shows that adding 20 per cent hydrogen to the grid would increase industry costs by an average of 23.8 per cent across the European Union (EU), and up to 43.3 per cent in Portugal.

Due to smaller user volumes households would see prices, on average, rise 11.2 per cent across the EU, and 15.9 per cent in Portugal.

The report by Fraunhofer Institute for Energy Economics and Energy System Technology (IEE), for the European Climate Foundation, assesses the technical feasibility, emission savings and cost impacts of adding hydrogen to the existing gas transport network, through “hydrogen blending” (which the report defines as, “the blending if hydrogen with natural gas at the level of the gas grid”).

Why hydrogen blending?

Natural gas currently accounts for at least 22 per cent of the EU’s greenhouse gas emissions. While hydrogen demand in the EU is currently mostly produced by using natural gas or coal (“grey hydrogen”).

The European Commission (EC) wants to make the EU a pioneer in the use of green hydrogen, that is generated using renewable energy. In 2020, the EC presented its hydrogen strategy with an aim to make widespread use of green hydrogen possible “across all hard-to-decarbonise sectors” from 2030 onwards.

The EU, made up of 27 member states, is planning to install 40GW of electrolysers by 2030, which would produce around ten million tonnes, or about 132TWh, of green hydrogen annually. However, to achieve 2050 climate targets (previously covered here) the EU would need to decrease emissions by reducing the use of natural gas in the buildings, industry and power sectors where the fuel currently plays a major role.

The scenarios

To capture the impact of gas demand, the study analysed three scenarios:

- EU scenario: Follows EC’s plan for a 55 per cent reduction of greenhouse gas emissions by 2030, and neutrality by 2050. The report states, this scenario presumes a mixture of increased policy ambitions with respect to energy efficiency, decommissioning of renewable energies, conversion of the transport sector, and expanding carbon pricing. With regards to the gas market, the EU scenario states a modest reduction and shift from natural gas to biogas and hydrogen by 2030, which progresses continuously until 2050.

- GfC scenario: Aims for the targets of the European Commission, while keeping a larger role for gas on energy supply through carbon-low and carbon-free gasses like natural gas with CCS and blue hydrogen (hydrogen that is generated from fossil energy carriers, particularly natural gas, with CCS).

- PAC scenario: Promotes a “fast-as-possible” exit from fossil energy carriers, with a complete exit from natural gas usage by 2035.

“No regret” sectors

According to the study blending 20 per cent green hydrogen - the maximum proportion that could safely be burned in domestic boilers - to Europe’s distribution networks will increase end-user costs by up to 43 per cent due to its complexities. Yet it would only reduce carbon emissions by 6-7 per cent due to the lower heating value of hydrogen compared to natural gas.

Yet some have also pointed out that 20 per cent hydrogen blending in Europe is by volume not energy. Hydrogen is 1/3 as dense as methane, so in energy terms, a 20 per cent Hydrogen blend equates to around 7 per cent hydrogen in energy terms.

Britain’s gas grid is currently preparing to accept a blend of up to 20 per cent hydrogen by 2023 as part of decarbonisation efforts.

Yet the agency argues that other uses of that hydrogen could see greater reductions in emissions and focus should be on “no-regret” sectors. It suggests higher greenhouse gas emission reductions (up to 50 per cent) can be achieved by using it in sectors where there are currently few alternatives for decarbonisation, such in the transport sector and industrial applications, and for the replacement of grey hydrogen.

The report points to the replacement of coal, diesel, bunker fuel, and aviation fuel, which have higher carbon contents than natural gas. It also states industries such as fertilisers, steel, shipping, and aviation, “would avoid lock-in risks, generate greater greenhouse gas savings for the investments made and avoid added costs being put on all gas consumers.”

Figure 1 shows the differing applications for direct hydrogen. It ranks each application’s energy efficiency – increased or reduced energy consumption, and therefore the renewable expansion requirements (covered in more detail below) - alongside infrastructure requirements.

Figure 1: Comparison of efficiency in regard to energy demand by sector (view larger image here)

Source: IEE, Limitations of hydrogen blending in the European gas grid

The report explains:

“Blending green hydrogen into the grid indiscriminately instead risks ‘wasting’ hydrogen by having it deployed to sectors like heating where more efficient and cost-effective solutions such as direct electrification using heat pumps are possible.”

The analysis shows that a 5 per cent blending target within the EU scenario would require around 50TWh of hydrogen - a large share of the total green hydrogen (132 TWh) available in 2030 under the EU’s hydrogen strategy. The agency suggests this 50 TWh could instead be used to meet demand in other “no-regret” applications.

“In view of the limited amounts of green hydrogen that will be available in 2030, it is important that these should find concrete applications with high CO2 reduction potential, instead of being ‘poured as if with a watering can’ into the natural gas network where it will offer limited CO2 reduction.”

Technically complex and costly

While the study agrees direct green hydrogen use has “clear advantages” for achieving climate targets, it also warns investment decisions must take “long-term efficiency into account”.

It highlights “technical challenges” of a gas grid that contains 20 per cent hydrogen, including potential issues with the origin of natural gas, transport pipelines, compressors, elastomer seals, gas meters, burners, storage sites and industries that would not be able to function with an H2/methane mix, such as glass and ceramics.

In the medium-term the limiting factor is the availability of green hydrogen – and the development of infrastructure needs to be considered, as additional renewable energy capacity must be built to cover the hydrogen production. Accommodating hydrogen into gas grids requires new investment, which will increase operating costs and impact end-user gas prices in the EU.

There’s also interconnected impacts; according to the agency hydrogen blending “represents a lock-in effect as area-wide adaptation measures would have to be financed that are neither necessary nor sustainable in the long term”.

Figure 2: End-user natural gas price increase for industrial customers because of blending

Source: IEE, Limitations of hydrogen blending in the European gas grid

Figure 2 shoes blending levels up to 5 per cent still results in modest price increases for all customer groups – an introduction in one country means all other countries need to take adjustment measures due to cross-border trade (or gas trade would have to be restricted, if technically allowed).

Key takeaway

While it’s clear that hydrogen blending has advantages, the agency highlights that policy makers face a choice of how to cost-effectively deploy the limited amounts of green hydrogen in the medium-term and targeting its application to ‘no-regrets’ sectors should be considered.

According to the report:

“Hydrogen blending is not a no-regrets option towards 2030. It is suboptimal because it does not specifically target end-uses for which hydrogen is generally agreed to be needed and imposes additional costs for lower greenhouse gas savings compared to using hydrogen directly. Therefore, H2 usage should be limited to areas where it is needed and cannot be substituted by electricity.”

Related Analysis

The ‘f’ word that’s critical to ensuring a successful global energy transition

You might not be aware but there’s a new ‘f’ word being floated in the energy industry. Ok, maybe it’s not that new, but it is becoming increasingly important as the world transitions to a low emissions energy system. That word is flexibility. The concept of flexibility came up time and time again at the recent International Electricity Summit held in in Sendai, Japan, which considered how the energy transition is being navigated globally. Read more

International Energy Summit: The State of the Global Energy Transition

Australian Energy Council CEO Louisa Kinnear and the Energy Networks Australia CEO and Chair, Dom van den Berg and John Cleland recently attended the International Electricity Summit. Held every 18 months, the Summit brings together leaders from across the globe to share updates on energy markets around the world and the opportunities and challenges being faced as the world collectively transitions to net zero. We take a look at what was discussed.

Australia’s Green Hydrogen Ambitions: Soldiering On Despite Adversity

Australia's green hydrogen sector is key to the nation's long-term decarbonisation plans, with ambitions to become a leading global producer and exporter. Despite strong government support and vast renewable resources, recent setbacks from major players like Fortescue and Origin have highlighted significant challenges to achieving a commercially viable industry. We take a look at challenges and opportunities facing the sector.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.