by Ben Barnes

Energy Affordability: Will Solar Sharer reduce energy costs?

Energy affordability has been a hot topic for the last few months. Whilst the first term of the Albanese Government could be characterised as being focused on shifting the narrative on renewables development, it seems likely that its second term will need to consider how to deal with affordability, for both households and businesses.

Since the election we have had a steady stream of indicators pointing to pressure on electricity prices. These pressures include advice from the Australian Energy Market Operator (AEMO) that transmission costs are likely to double from where they were two years ago, the Australian Energy Regulator (AER) made a draft decision for the next regulatory period that would see revenues for some Victorian network businesses rise by almost 40 per cent from the current five year determination period, and further delivery delays for new generation is keeping the spot and contract markets stubbornly high.

On the flip side, the Government has sought to counteract these price pressures through measures such as the highly successful Cheaper Home Batteries subsidy which will allow those already benefiting from rooftop PV to shift their consumption into the evenings, and last week’s Solar Sharer announcement, purporting to give customers in three states free electricity for three hours. More on that below.

While not yet announced, media this week is suggesting that an extension of Energy Bill Relief is again on the cards, with a possible announcement later this year. While we would say that the very high costs of universal bill relief might be better targeted towards vulnerable consumers in need of support, the potential extension isn’t surprising when you think about the politics. When the ABS’s full year inflation statistics were released for 2024 in January this year, it noted energy costs reduced by a quarter, directly as a result of the Commonwealth’s energy bill relief and other State based subsidies. Absent relief, energy costs would have only fallen by a couple of per cent[i]. Illustrative of the significant impact of bill relief on Australia’s overall Consumer Price Index, in its most recent dataset the ABS blamed a 9 per cent quarterly jump in energy costs on just a one-month delay in the application of bill relief in NSW and the ACT. It’s not surprising that a government facing a sharp bump in inflation might find it difficult to wean itself off continuing rebates into 2026.

So what is the likely direction of travel for energy prices in the medium term, and is there anything industry and consumers can do to minimise the impacts?

Our analysis is anticipating electricity prices to remain high over the coming years. This is the price that the success of the transition is publicly measured against, and is an important marker for affordability. But it certainly isn’t the only marker that should be considered here.

As the transition progresses, there is a material risk that the residential energy market will increasingly split into two, with vastly different outcomes for the two customer cohorts. This risk is something governments and industry need to actively manage and is discussed further below.

Households with solar and batteries will likely see energy bills decline. For the 4.2 million households with rooftop solar, electricity, when the sun is shining, will be effectively free, enabling significant savings if high consumption loads can be shifted from the evenings into the middle of the day. For the approximately 110,000 households who have installed a battery since 1 July under the Cheaper Home Batteries Program, and those who paid full price before that date, electricity costs from the grid will likely be negligible. Not only will they also get free solar in the day, but any loads they are unable to shift should, for the most part, be served by stored energy in their battery. In a few years, electric vehicles might be able to play the role of a stationary battery, avoiding the need for duplicative household investment as Australia’s road fleet shifts from internal combustion engines towards EVs.

So what about those who can’t install consumer energy resources like solar and batteries in their home, and don’t have an EV? The Commonwealth Government says it’s here to help by mandating retailers give customers the opportunity to opt into a tariff that delivers free electricity for three hours in the middle of the day, by introducing a new Default Market Offer (DMO) tariff called Solar Sharer. The premise is that when the sun is shining, wholesale electricity prices are very low or negative, so retailers should pass that benefit onto consumers. The second stated benefit is that shifting loads from peak periods to periods where there is a glut of solar and excess grid capacity will reduce overall system costs for all consumers. The announcement seeks to regulate a product that several retailers – including AGL, Red Energy, GloBird Energy, and OVO Energy – already offer today.

Is solar sharer good policy?

Depending on which commentator you read, this is either the best thing to happen to households in Australia or the worst. In my view, it’s probably a bit of both, but on the whole, I think this is likely to be an ineffective policy for Australian households and is unlikely to bridge the gap between those with Consumer Energy Resources (CER) and those without (often referred in energy circles as the haves and have nots). Whether it drives behavioural change and results in lower overall system costs is yet to be seen, but that would be a positive outcome if it eventuated.

Why? Well the first reason is that for the most part, as is seen in the various free window offers already available today, the price outside of the three-hour window is not free, and it seems reasonable to assume that consumers who haven’t to date invested in solar and batteries are less likely, or able, to want to shift their loads to the middle of the day. The second reason is that the mandated offer will not be a market offer, but rather a default offer that consumers will need to opt into. Default offers to date have tended to be priced at a higher rate than comparable market offers, incentivising customers to shop around. The Government says it will lower the cost of the DMO and “ensure consumers on a standing offer pay a fair price that does not build in additional costs over the efficient cost to electricity retailers for providing an essential service”.[ii] The changes are slated as making the DMO more like the Victorian Default Offer, which whilst closer to a competitive offer than the DMO, still remains a middle of the road offer should a household wish to shop around.

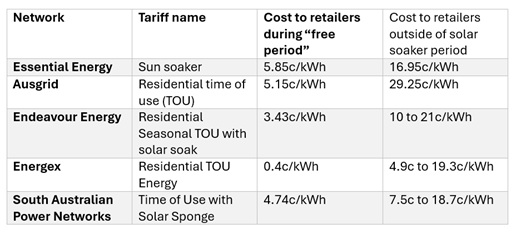

So, what does that all add up to? In effect, for a household to benefit from the Solar Sharer, they have to be willing to decide whether to opt into the new DMO as opposed to the market offers already available, and make an assessment as to whether or not they are able to shift enough of their load into the middle of the day to offset the higher costs outside of the period. While the AER will have a role to set the prices, it is important to remember that just because a free period is announced, it does not mean costs evaporate. Wholesale and network costs will still be incurred by retailers during the three-hour “free” window. The below table shows the cheapest network tariff currently available during the middle of the day, and its cost to retailers in 2025/26.

Wholesale costs are another material cost that retailers will incur during the free period that will need to be recovered elsewhere. Without trying to model the outcomes for future years, taking a quick look at the spot price outcomes over a 12-month period can give you an idea of the average wholesale price for a three-hour window in the middle of the day[iii]. Not surprisingly, the average spot prices differ over the three DMO jurisdictions, resulting in different risks for retailers.

In South Australia and Queensland, over the year, average spot prices for the middle of the day hovered around $0 a MW/h (~$3 MW/h in Queensland, and a few cents below $0 MW/h in South Australia). But in New South Wales, the average spot price in the middle of the day was ~$31/MWh, a not immaterial figure of around 3c per kWh. When digging a bit deeper and considering seasonality, average spot prices in NSW in December and June during the Solar Sharer window were around $65, dropping below $0 in September. There are other costs that will need to be recovered, but for the sake of this article, at a high-level retailers in New South Wales will incur costs of at least 7c per kWh that will need to be recovered during high priced windows.

It's important to note that prices over the last 12 months were low both because of high renewable output, and low demand. It will be interesting to see whether the demand profile shifts materially with an incentive to consume more in the middle of the day, which during some parts of the day will have a material impact on the spot price, and ultimately the types of generators that will need to be dispatched to deliver enough supply.

One thing this data illustrates clearly, is that as the transition progresses and more and more batteries are connected to flatten out the daytime load, energy prices, and ultimately, its affordability, will swing significantly as the energy mix changes and weather plays a much greater role in determining renewable energy output. In windy, sunny years, expect wholesale prices to be very low, but in years where wind and solar output is lower than average, expect the spot price to jump materially.

So what will help with energy affordability?

In short, there is no silver bullet, but industry acknowledges the need to lean in and work with Government in identifying policy levers that that will allow consumers to benefit from the transition to a reliable, affordable and decarbonised energy system.

As highlighted above, under the current industry structures those with CER will likely see relatively low energy costs over time and given that, policymakers shouldn’t focus their efforts on supporting that cohort. It goes without saying that if you own a property with a relatively sunny roof you should install solar panels. It is the number one driver of cheaper electricity at the household level. Batteries are probably a more marginal investment for most consumers, so if you are thinking of taking advantage of the Cheaper Home Batteries Program, first do the numbers to make sure the capital cost and expected lifespan of the battery stack up. For those with high evening consumption and excess solar in the daytime, there might be benefits in buying a battery.

For everyone else, particularly renters and apartment dwellers, before jumping onto the new Solar Sharer DMO it will be important to consider whether enough load can be shifted from higher priced peak periods into the middle of the day to come out on top. This will likely benefit those with EVs or large and easily shiftable loads. You will likely pay more in the peak periods to offset the costs avoided in the daytime, and unless you have an EV to charge, or large loads you can easily shift, you are unlikely to benefit from this type of an offer.

At a household level, the most impactful thing to reduce energy bills is to reduce your energy consumption, and this doesn’t have to mean reducing consumer comfort. Smarter usage of air conditioning and heating, reducing air gaps driving heat loss, using thicker curtains or external blinds to keep heat in or out, and switching to lower consumption appliances can make a real material difference to energy bills.

Of course, the energy price is important, so always seeking out a cheaper deal by using one of the excellent government run comparison sites can help – Victorian Energy Compare in Victoria, or Energy Made Easy everywhere else in the NEM.

Finally, governments and retailers have a really critical role to play in providing genuine support to vulnerable consumers – a growing cohort as the cost-of-living crisis looks to stretch into another year. If customers are struggling to pay their bills, contacting the retailer to let them know can unlock a range of support options tailored to your needs. The AEC is working closely with retailers on what additional measures might provide meaningful support to customers to improve affordability in a sustainable manner. But there will be more to come on that in the new year.

For governments, targeted subsidies and rebates are the most important tool to support those who most need it. The AEC strongly supports the recent recommendation from the AEMC to automate concession access for eligible Australians. As an additional step, flexible concessions that can scale up and down depending on whether or not the weather has led to a high or low-cost year is a tool that a future government might be able to effectively leverage to manage affordability for those doing it tough.

[i] https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia/dec-quarter-2024.

[ii] https://consult.dcceew.gov.au/consultation-on-reforms-to-the-default-market-offer.

[iii] Note the time of day the DMOs three free hours will occur is not yet prescribed. This analysis assumes 11am-2pm is chosen in NSW and QLD, and 10am-1pm in SA as the cheapest possible window.

Related Analysis

Efficient Pricing in an Uncertain Energy Market

Electricity prices are once again front of mind for Australians, and with cost-of-living pressures mounting, expectations for fair and transparent pricing are entirely reasonable. But as reforms to the Victorian Default Offer and Default Market Offer evolve, a more complex challenge emerges: how to keep prices in check without undermining the stability, competition and investment needed to sustain the energy system over time. Striking that balance is at the heart of current reform debates, and will ultimately determine whether today’s affordability measures support or weaken the system in the long run. Read more.

The Shadow of the Safety Net: Who Pays for Fairness?

Fairness is a defining Australian value, and it sits at the heart of Victoria’s Getting to Fair strategy aimed at improving equity in essential services. While the Australian Energy Council strongly supports helping people in vulnerable circumstances, funding social equity programs through energy bills risks creating hidden cross-subsidies that place additional pressure on households already struggling with affordability. We take a look at why a more transparent, tax-funded model, combined with retailers acting as delivery partners, may provide a more sustainable and genuinely fair pathway to supporting vulnerable customers.

Beyond the “loyalty penalty”: unlocking CER value is the real pathway to a services market

The Australian Energy Market Commission pricing review has sparked debate about fairness and competition, with the AEC cautioning against treating price differentials as the core problem. Recent evidence from the ACCC suggests competition and recent reforms are improving customer outcomes with the AEC arguing that a true shift to a services-based market will depend on unlocking and fairly sharing CER value, not weakening the competitive dynamics that drive innovation. We outline our position on the review. Read more.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.