by Jo De Silva

Beyond the “loyalty penalty”: unlocking CER value is the real pathway to a services market

The Australian Energy Market Commission (AEMC) has now received submissions to its pricing review. The core message in our contribution was:: the transition to a services-oriented energy market will not be delivered by treating price differentials as the central problem. The real constraints are structural - whether customers can access, trust and share in CER value, and whether market institutions allow that value to be measured, stacked and allocated fairly.

The context matters: cost-of-living pressure and reform saturation

Electricity affordability remains front-of-mind for households, industry and governments. Retailers are already undertaking significant work to support customers in difficulty -within the framework of existing rules and with limited room to “absorb” system-wide affordability pressures given the reality of cost recovery and modest margins.

At the same time, the reform pipeline is crowded. The AEMC itself has illustrated how interacting reforms are layering complexity across the retail sector. As further measures are announced during this review process, the Australian Energy Council (AEC) urges caution about adding major new regulations before the impacts of recent changes are understood.

Importantly, the most recent market monitoring evidence shows competition combined with recent reforms is delivering more positive outcomes for customers. In its December 2025 report, the Australian Competition and Consumer Commission (ACCC) noted “signs that competition and recent policy reforms… are leading to more positive outcomes”, and found customers can save around $100–$250 per year by switching away from default-offer range plans under typical usage assumptions.[i] (The same report also observed that around 20 per cent of electricity customers switch retailers in any given year.[ii]

This matters because the AEMC’s vision of innovation -tailored offerings, new service models, and more sophisticated products—is most reliably delivered through competition, not by constraining it.

Defining the problem: “loyalty penalty” vs “search rewards”

The AEMC’s draft report places significant weight on “loyalty penalties” as a barrier to the evolution of retail markets. The AEC accepts there is a legitimate community debate about fairness and essential services, and we recognise concerns where some customers pay materially more than others.

However, in a real-world competitive market, the existence of price differentials is not, by itself, evidence of market failure. It can also be the other side of the coin: “search rewards”-the benefit customers receive when they spend time comparing and switching. Those search rewards are not merely private benefits., they are part of the discipline mechanism that pressures retailers to reduce costs and sharpen offers, with broader system benefits.

The ACCC’s own analysis demonstrates two things at once:

- Some customers on older plans pay more: customers on plans more than 3 years old were paying an average of $221 more than customers on new plans.[iii]

- And there are already significant reforms underway that will likely constrain loyalty penalties from 1 July 2026, including protections for post-benefit-change customers and discount rule changes, plus enhanced “better offer” communications from September 2026.[iv]

The risk in the AEMC’s recommendation 1 (“same plan, same price”) is that it implicitly targets the price differential itself, rather than the outcomes we actually care about: affordability, transparency, customer confidence, and innovation. Put bluntly, “ensure every customer is always on the best price” is only achievable by setting the search reward to zero, weakening switching incentives and, over time, the competitive pressures that help keep costs down.

This is not theoretical. The ACCC shows that a substantial cohort remains above default-offer benchmarks (including customers paying more than 10 per cent above default offers).[v] ( The appropriate response is not to flatten competitive dynamics, but to sharpen the tools that help customers engage and ensure protections for those who cannot.

Why a services market is not “blocked” by loyalty penalties

The AEMC wants to move toward a services market. The AEC shares the desire to move in that direction of travel: a future where retailers and aggregators orchestrate complexity behind the scenes, offer simplicity and predictability, and integrate CER into products customers actually want.

But the draft report appears to assume that once price differentials are constrained, the system will more naturally pivot to services. The AEC does not think that follows.

A services market requires that customers can benefit from their CER and that the system can unlock and share CER value across multiple value streams. That is where the real barriers sit:

1) Network value must be measurable, stackable, and shareable

CER value is increasingly location- and time-dependent (congestion, export constraints, local peaks). If customers cannot see what their flexibility is worth -and if intermediaries cannot reliably monetise that value -then services remain a story, not a business model.

This is why we emphasise the distinction between:

- Network tariffs as relatively stable price signals (with strong community preference for “postage stamp” simplicity), and

- Dynamic, locational signals better delivered as network support payments (targeted, time-specific incentives that can underpin VPP value propositions).

The AEC is not convinced the AEMC should be prescribing definitive views on what the “right” network tariffs look like. Tariff design is a trade-off problem; rigid prescriptions risk unintended distributional outcomes and may not actually create the network value pathways needed for services.

2) Trust, transparency, and low-effort participation are foundational

A services market works when customers believe: “My retailer is maximising value for me, fairly, with minimal effort from me”,requires clear benefit-sharing models, data portability, and consumer protections that build confidence. This is particularly important in a community where energy hardship is widespread: Energy Consumers Australia estimates nearly 1 in 5 households are vulnerable to, or experiencing, energy hardship.[vi]

3) Market architecture must support innovation without collapsing the economics

Innovation requires investment and risk-taking. If reforms compress margins and remove acquisition dynamics, the result may not be “more services”; it may be less experimentation, especially from smaller retailers whose growth models rely on competitive acquisition pricing.

Academic research on “fairness regulation” in pricing also highlights the risk of unintended outcomes- such as reduced undercutting and higher prices -if interventions are not carefully calibrated.[vii] This is not an argument against protections; it’s an argument for precision, sequencing, and evidence-based design.

Costs are real: the “same plan, same price” problem in practice

One core analytical weakness in the “same plan, same price” approach is that it tends to treat plans with the same label as identical over time. In reality, the cost stack moves -particularly wholesale hedging, policy costs, and network charges that reset annually.

Two simple case studies illustrate why blunt equivalence rules can backfire:

Case study 1: Falling cost environment.

A retailer prices a mass-market offer based on contract prices at the time. Six months later, hedging costs fall, and the retailer can offer a better acquisition price. Under strict “same plan, same price”, the retailer would have to reprice the entire existing cohort to the new lower price—despite the higher cost-to-serve embedded in historical hedges. The rational outcome is the retailer doesn’t launch the sharper offer, and customers lose a competitive option.

Case study 2: Rising cost environment.

If costs rise, and the retailer must increase the acquisition price to remain viable, “same plan, same price” can force price rises onto earlier cohorts or discourage the retailer from offering the plan at all—again reducing competitive choice and innovation.

These dynamics are not edge cases. They are routine outcomes of managing risk in electricity markets.

International experience: mixed evidence, and caution on unintended consequences

Other sectors and jurisdictions have tried to address loyalty penalties through pricing fairness rules.

In UK insurance, the Financial Conduct Authority introduced rules that require renewing home and motor insurance customers to be quoted prices no higher than equivalent new customers, as part of reforms aimed at ending “price walking”.[viii] While there are benefits, the UK has also seen ongoing evaluation and debate about market impacts and product redesign.

In UK energy, Ofgem has kept a prohibition on “acquisition-only” tariffs during and after the wholesale price crisis, and in late 2025 decided to extend the Ban on Acquisition-only Tariffs beyond March 2026 (to March 2027).[ix] Ofgem itself has acknowledged the trade-offs: protecting consumers and market stability on the one hand, and potentially dampening competitive switching incentives on the other.

The lesson is not “do nothing”. It is: major interventions in pricing dynamics are blunt instruments. If Australia goes down that path, we must do so with very clear objectives, careful calibration, and a strong implementation plan that avoids weakening the very competition we also rely on to drive innovation.

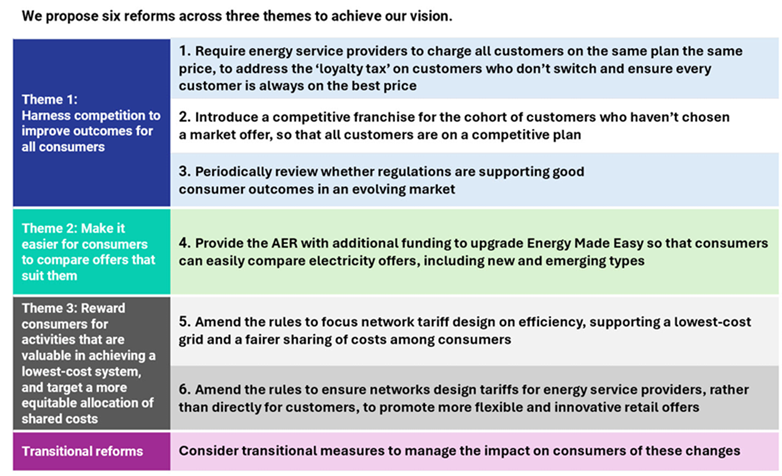

AEC views on the draft recommendations: what we support, what needs work

The AEMC’s recommendations are shown in figure 1 below.

Source: AEMC Pricing Review

In summary:

- Recommendation 1: We have serious concerns. The framing is anti-competition, and risks eliminating switching rewards, raising prices for customers currently on the best deals, and reducing innovation incentives.

- Recommendation 2: More pro-competition in concept, but radical in execution. We need far more detail on auction design and market impacts before forming a settled view.

- Recommendations 3 and 4: Sensible in principle but require careful design to achieve worthwhile outcomes.

- Recommendation 5: We are not convinced the AEMC should prescribe definitive views on “right” network tariffs; tariff design is a trade-off problem and should not conflate stable tariff signals with dynamic network support payments.

- Recommendation 6: Highly supportive—this remedies a long-standing ambiguity, provided the process is set up appropriately.

Next steps: more consultation, and a sharper focus on unlocking CER value

Given the number of reforms already in flight- and the material risks of recommendation 1 as currently framed - the AEC urges the AEMC to undertake further consultation before finalising the report. In our view, a second draft report is likely appropriate, alongside deeper testing of workable alternatives that preserve competition while strengthening protections for customers who cannot easily engage.

Most importantly, if the policy goal is a services market, then reforms must prioritise the practical enablers of CER value: interoperability, transparent benefit-sharing, data portability, and mechanisms that allow network value to be revealed and shared -without forcing customers into complexity.

Because the true barrier to a consumer-driven, services-oriented future is not simply whether customers switch plans often enough. It is whether customers can confidently participate -at low effort -in a system that actually pays them back for the value their CER creates.

[i] https://www.accc.gov.au/system/files/inquiry-national-electricity-market-report-december-2025.pdf

[vi] https://energyconsumersaustralia.com.au/our-work/surveys/consumer-energy-report-card-understanding-measuring-energy-hardship-australia

[vii] https://www.businessthink.unsw.edu.au/articles/loyalty-penalty-regulations-market-competition-impact

[viii] https://www.fca.org.uk/publications/policy-statements/ps21-11-general-insurance-pricing-practices-amendments

[ix] https://www.ofgem.gov.uk/consultation/renewing-ban-acquisition-only-tariffs-bat-after-march-2026

Related Analysis

Efficient Pricing in an Uncertain Energy Market

Electricity prices are once again front of mind for Australians, and with cost-of-living pressures mounting, expectations for fair and transparent pricing are entirely reasonable. But as reforms to the Victorian Default Offer and Default Market Offer evolve, a more complex challenge emerges: how to keep prices in check without undermining the stability, competition and investment needed to sustain the energy system over time. Striking that balance is at the heart of current reform debates, and will ultimately determine whether today’s affordability measures support or weaken the system in the long run. Read more.

The Shadow of the Safety Net: Who Pays for Fairness?

Fairness is a defining Australian value, and it sits at the heart of Victoria’s Getting to Fair strategy aimed at improving equity in essential services. While the Australian Energy Council strongly supports helping people in vulnerable circumstances, funding social equity programs through energy bills risks creating hidden cross-subsidies that place additional pressure on households already struggling with affordability. We take a look at why a more transparent, tax-funded model, combined with retailers acting as delivery partners, may provide a more sustainable and genuinely fair pathway to supporting vulnerable customers.

A New Year: New regulated offer; new records but some old challenges

A new year has brought major developments across Australia’s energy markets, with new regulatory interventions alongside record-breaking renewable generation. The Federal Government’s Solar Sharer Offer marks a significant shift in retail market design, while the wholesale market delivered historic renewable output and much lower prices, driven largely by strong wind and growing battery capacity. We take a look at what these changes mean for customers, retailers and the reliability of the power system, and where old challenges continue to resurface.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.