by Carl Kitchen

A changing of the guard: Gas generation projections

All the focus on the market operator’s latest assessment of gas supplies[i] for eastern Australia was on the previously forecast gas shortfall for Victorian and NSW now being pushed out by three years to 2026, because of the expected development of the Port Kembla Gas Terminal (PKGT).

There was caution around the certainty of the long-term outlook for gas usage, with industrial demand expected to be flat or falling in the next 20 years. There is a shift in the demand outlook flowing from the expectations for gas-fired generation in the National Electricity Market (NEM). This is primarily the result of the much stronger growth in renewables. The Australian Energy Market Operator (AEMO) also points to the development of new transmission to support renewables, as well as investment in power system stability to support growth in wind and solar.

While there is this expectation that gas for gas-fired power generation will decline, the value of that generation to the grid in providing flexible, quick response power is likely to increase. AEMO expects gas-fired generation demand to become more “peaky” and to switch to peaking in winter instead of summer. We take a closer look at the assessment of gas-fired generation.

Gas-fired generation assessment

The level of gas-fired generation in the NEM in the longer-term unsurprisingly will depend on the ultimate generation mix, along with factors like the cost of gas and alternative technologies. It will be impacted by the amount of renewable generation that comes into the system, as well as the timing of coal-fired plant retirements.

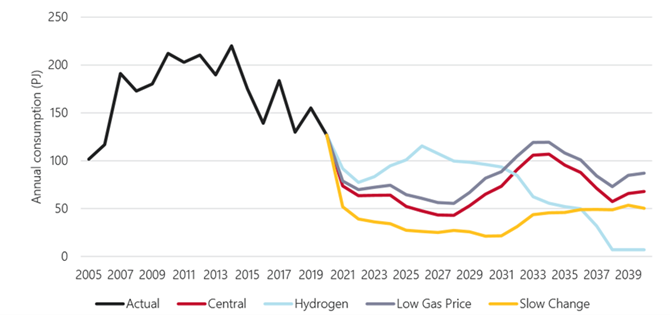

Last year gas used for generation fell 23 per cent (to 127PJ) compared to the previous year – the lowest level in more than a decade. Key factors were a drop in underlying demand of 1.5 per cent, particularly due to the impact of COVID-19 on economic activity, as well as the large volume of renewables that came into the grid.

More than 3GW of new large-scale wind and solar was commissioned and the output from these sources as well as rooftop solar increased to 20 per cent of underlying demand. At the same time there was a slight increase in hydro generation.

Operational demand - essentially demand met from the grid - was also down as rooftop solar increased its role in supplying households.

AEMO expects gas-fired generation to become more dependent on weather conditions, given the need to increasingly be used to firm renewables or respond to extreme events. Both open cycle gas turbines (OCGT) and reciprocating engines are able to ramp up quickly as we have reported previously (see Barker Inlet: A new technology responding to the market) which makes them suited to deal with changes in supply and demand while gas-fired plants can also provide supply for extended periods.

Regardless of the role of gas-fired generation in supporting the grid, as renewable generation capacity grows, gas-fired plant is expected to be under more pressure. Even without the impetus that the New South Wales Electricity Infrastructure Roadmap (which is expected to drive more renewables) AEMO has forecast more than 4GW of renewables to be operational in the next two years and annual gas-fired consumption to fall to 74PJ in 2021 and 64PJ the following year in its central scenario, which is around half the level last year.

Transmission developments are also expected to see further reductions for gas fired generation in the medium term, while coal plant retirements could lead to periodic jumps in gas generation in its support role. In the long-term the growth in renewables, storage and network augmentation is projected to keep gas-fired consumption lower than we have traditionally seen.

The scenarios considered for gas-fired generation are shown in Figure 1.

Figure 1: NEM GPG consumption actual and forecast, by scenario, 2005-40 (PJ)

Source: Gas Statement of Opportunities

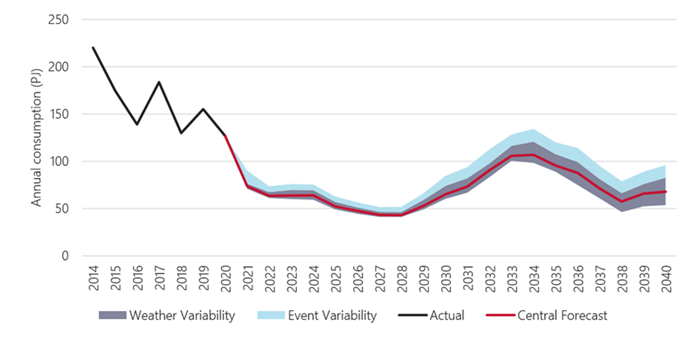

Despite the overall expected decline in gas for generation, weather patterns, extreme weather events and outages on power infrastructure could drive temporary increases in gas demand as shown below.

Figure 2: NEM GPG consumption actual and forecast, by scenario, 2005-40 (PJ)

Source: Gas Statement of Opportunities

Recent events that have led to the need for increased gas-fired generation include:

- The so-called Tasmanian energy crisis, resulting from an extended Basslink interconnector outage from December 2015 coinciding with low water storage levels for hydro generation, which led to the re-commissioning of the Tamar Valley gas-fired power station.

- The extended Loy Yang A and Mortlake unit outages in Victoria.

- Closure of the Hazelwood power station in Victoria in 2017 and coal shortages at Mt Piper and the extended outage of Loy Yang A2 in the Latrobe Valley drove an increase in gas-fired generation in New South Wales.

- The extended hot weather across south eastern Australia in the 2019-20 summer.

- The failure of the Heywood interconnector between South Australia and Victoria in early 2020.

The likely level of gas-fired generation that will be required in the NEM is debated. In February analysts Wood Mackenzie found there may be 10 times more gas for power generation required than assumed by the market operator and also warned of the risks of moving too quickly to rely on batteries to back up renewables. It expects gas generation to stay at around 10 per cent of the NEM by 2030[ii].

Frontier Economics in a report for the AGPA saw a critical role for gas-fired generation in supporting high levels of renewables at low cost. Frontier Economics notes that much of the benefit of gas-powered generation is based on retaining sufficient capacity in the system to ramp up and provide electricity during periods of low renewable generation. Like the market operator, it sees that while this might require periods of high gas generation at times, it won’t mean high gas consumption given its role.

[i] Gas Statement of opportunities, Australian Energy Market Operator, March 2021

[ii] Gas still to play critical role in generation: Woodmac, Australian Financial Review, 4 February 2021

Related Analysis

The gas transition: What do gorillas have to do with it?

The gas transition poses an unavoidable challenge: what to do with the potential for billions of dollars of stranded assets. Current approaches, such as accelerated depreciation, are fixes that Professorial Fellow at Monash University and energy expert Ron Ben-David argues will risk triggering both political and financial crises. He has put forward a novel, market-based solution that he claims can transform the regulated asset base (RAB) into a manageable financial obligation. We take a look and examine the issue.

Australia’s Sustainable Finance Taxonomy: Solving problems or creating new ones?

Last Tuesday, the Australian Sustainable Finance Institute (ASFI) released the Australian Sustainable Finance Taxonomy – a voluntary framework that financiers and investors can use to ensure economic activity they are investing capital in is consistent with a 1.5°C trajectory. One of the trickier aspects of the Taxonomy was whether to classify gas-powered generation, a fossil fuel energy source, as a “transition” activity to support net-zero. The final Taxonomy opted against this. Here we take a look at how ASFI came to this decision, and the pragmatism of it.

Gas in the NEM: Is there a case for a new and expanded RERT?

Gas-powered generation (GPG) will be essential to maintaining reliability in the National Electricity Market (NEM) as coal exits and the grid becomes increasingly reliant on variable renewable energy (VRE) and storage. However, current market settings and investment mechanisms are failing to support the GPG capacity needed for both regular firming and emergency insurance against high-impact, low-probability (HILP) VRE droughts. We take a closer look at whether a new and expanded Reliability and Emergency Reserve Trader (RERT) framework could provide a viable pathway to deliver insurance GPG outside the market without distorting competitive outcomes.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.