Virtual power: Fast becoming a reality?

Earlier this month Origin Energy revealed it was targeting growth in its Virtual Power Plant program of 2000MW - up from around 200MW – drawing on batteries, solar PV installations, demand response and electric vehicle chargers. Indeed right across the Australian Energy Council’s membership VPPs are being looked at was a way of managing DER in the grid and providing new products to customers.

It underlines that VPPs have been identified as playing a key role in the future energy mix in Australia with the Australian Energy Market Operator (AEMO) expecting an increasing role for distributed energy resources in its draft 2022 Integrated System Plan (ISP).

This has been supported by the revolution in domestic solar PV with more than 3 million homes and business now with installed systems. There was an estimated 25GW of rooftop solar at the end of last year with the installation of 3GW in each of the past two years. Despite this the potential for aggregated distributed energy resources (DER) remains nascent.

VPP trials show that aggregated DER can provide not just generation, but demand response, contingency frequency control and ancillary services (FCAS) and potentially network services

AEMO was positive about the results of its series of VPP trials which we look at in more detail below.

Hurdles to overcome, based on the findings of a new Institute for Energy Economics and Financial Analysis (IEEFA) report, include the current lack of dependable revenues for customers or VPP providers and development costs, particularly for start-ups. The costs include the need to develop aggregation software systems and associated hardware to aggregate DER, determine when to use the capacity behind-the-meter (BTM) or when to export and to which markets.

While IEEFA believes the margins for operators are currently thin, it does anticipate the opportunity for strong growth with changes in the grid, and notes that this has not stopped an estimated 20 commercial VPP products being made available in the National Electricity Market (NEM). Below we take a closer look at the report and recent VPP developments.

Why VPPs

A VPP has the potential to be a capital and cost-efficient way to create replacement capacity, For example Origin is looking to the coordination of distributed assets to replace some of the Eraring power station’s capacity when it exits the market and to firm renewable assets “at a very low cost”. It also sees the benefits of VPP for retailers by creating lower churn and “deeper engagement” while seeking to “fulfill customers’ expectations for lower costs, decarbonisation and energy autonomy”.

The first major VPP project was undertaken by AGL in South Australia in 2016. Supported by ARENA, this included the sale and installation of 1000 batteries in Adelaide with a total 5MW capacity. This participated in the market operator’s demonstrations for wholesale market and contingency FCAS using a cloud-based platform.

Simply Energy has also been involved in an ARENA supported project, VPPx, involving 1361 households providing 6MW of capacity to the SA grid and integrating with a distributed energy market platform. The project found there are economic benefits to all stakeholders and led to Simply Energy developing a new VPP offer which it launched in May 2021.

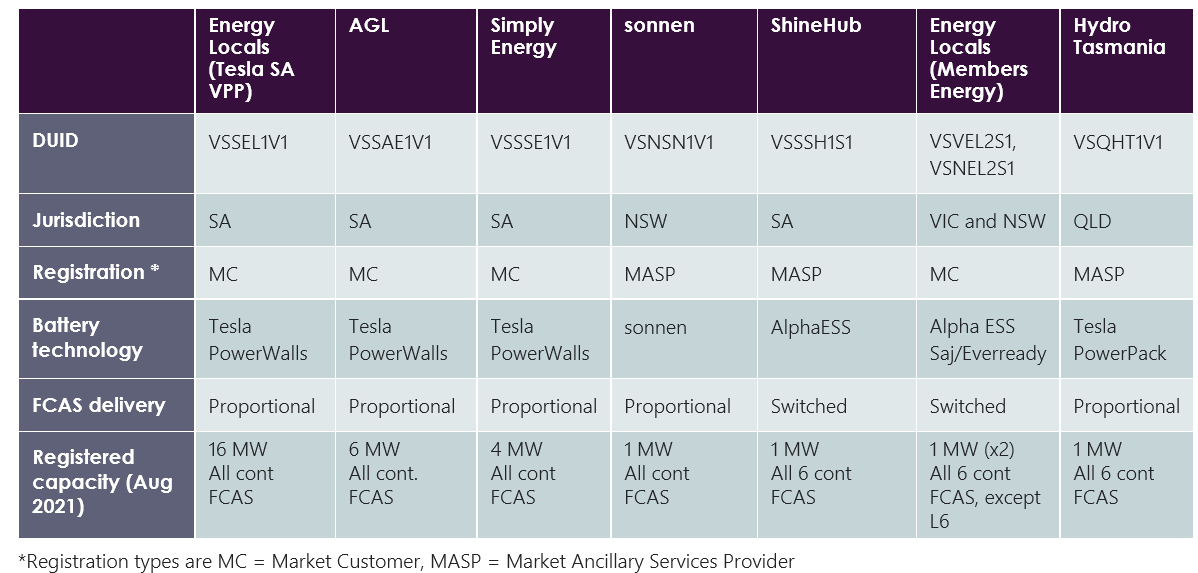

The Australian Energy Market Operator (AEMO) established a VPP demonstration program and trials in 2019 and participants in these are shown in figure 1. They included:

- VPP portfolios across all mainland NEM states.

- A total registered capacity of 31 MW (equivalent to a small scheduled hybrid solar farm plus battery). All VPPs used batteries in their portfolios.

- Approximately 7,150 consumers signed up (almost 25 per cent of customers with registered batteries in the NEM).

Overall, the trials showed that VPPs could deliver FCAS, respond to energy price signals, and deliver local network services “at times simultaneously”. AEMO also noted that VPPs have been able to support the power system during numerous major contingency events over the last two years, including separation events between South Australia and Victoria as well as trips of major generating units.

AEMO reported VPPs in the trial increased market share of contingency FCAS to 3 per cent of market share in April 2021, up from 0.6 per cent in April 2020.

According to AEMO Manager DER Market Integration, Matt Armitage, household batteries showed they could play a role in FCAS.

“Evidence indicates that household batteries are highly effective at providing contingency Frequency Control Ancillary Services (FCAS), with VPP’s supporting the power system during major contingency events in the National Electricity Market over the last two years.

“Consistent with previous reports, VPPs are also highly capable of responding to energy market prices in real time and can deliver local network services, at times delivering more than one service simultaneously,” he said.

AEMO also reported though that while VPPs are very capable of responding to energy market prices in real time, “their behaviour is largely dominated by serving the household first and maximising the self-consumption of rooftop PV”.

Figure 1: Participants in AEMO VPP Demonstrations

Source: AEMO

According to IEEFA almost all participants in AEMO’s trial are continuing to offer VPP products to households and providers such as EnergyAustralia and Origin also offering commercial VPP products to residential customers. Meanwhile in WA, Synergy has established a schools VPP pilot program involving 17 schools, which is the state’s first VPP. While in WA Synergy has established a schools VPP pilot program involving 17 schools, which is the state’s first VPP.

Commercially available VPPs have been participating in the wholesale market, FCAS markets and the Reliability and Emergency Reserve Trader scheme (RERT) and have also occasionally provided distribution network support services, including thermal, voltage or peak demand management. The IEEFA report notes that aggregated household DER can’t participate in the NEM’s wholesale demand response mechanism currently and has only been involved in the RERT in trials.

VPPs are coordinated using cloud-based gateway via an inverter with embedded energy management capability or a dedicated device to provide on-site gateway to manage behind-the-meter DER.

The future of retail?

The IEEFA sees VPPs as the future of retail, arguing that the acceleration in DER and electric vehicles will be an important factor in driving this, along with improved profitability from aggregated DER as a result of increased solar and battery capacity, particularly from EVs, falling costs and broader use of DER with demand response capabilities.

It expects that with more household supply and storage sitting behind the meter it will be hard for retailers without VPP to be profitable. It also flags that sales from the grid will continue to fall “eroding gentailer” profitability while exports from DER will increase along with opportunities for aggregators. But it also notes that the highest value use of DER can be expected to be behind the meter, as a means to reduce power bills by avoiding network and other costs. So into the foreseeable future VPP revenue for customers will continue to be small compared to behind-the-meter savings from solar and battery storage. It estimates average household bill savings from VPP involvement is around $200 annually, much less than savings from households storing solar output.

And AEMO has also sounded a note of caution, saying the rapid growth of DER in Australia’s energy system leaves open new types of cyber security threats, which could ultimately pose a threat to power system security. Another challenge that would need to be overcome.

While it seems clear VPPs will continue to develop and grow as more domestic and commercial properties have rooftop solar installed and the cost of batteries fall and the scale of available storage increases and energy markets evolve, the extent to which it will represent the future of retailing remains debatable.

Related Analysis

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Green certification key to Government’s climate ambitions

The energy transition is creating surging corporate demand, both domestically and internationally, for renewable electricity. But with growing scrutiny towards greenwashing, it is critical all green electricity claims are verifiable and credible. The Federal Government has designed a policy to perform this function but in recent months the timing of its implementation has come under some doubt. We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.