by Justine Lovell

US energy markets: Predicting future performers

The US Energy Information Administration recently released its latest Annual Energy Outlook 2018 (AEO), which projects key trends likely to affect the US energy markets over 2017-2050.

The US has been a net energy importer since 1953, strong domestic production coupled with flat energy demand are expected to spur the US to become a net energy exporter by 2022[i]. This change occurs even earlier in some of the report’s ‘sensitivity cases’, which assume larger growth in natural gas production.

Modelling

The AEO’s projections are modelled on different assumptions, as future market events cannot be confidently predicted.

The report includes sensitivity cases (e.g. Low and High Economic Growth; Low and High Oil Price; Low and High Oil and Gas Resource Technology), which include different assumptions to reflect possible future events in the US energy markets, changes in technologies, and developments in resources.

Here, we mainly focus on the report’s baseline – or ‘reference case’. The reference case assumes trend improvements in known technologies. It does not predict future energy policy and acts on the assumption of current laws and regulation (therefore the phasing out of current solar and wind policies are included within its projections). More information about the report’s assumptions is available here.

Consumption and emissions

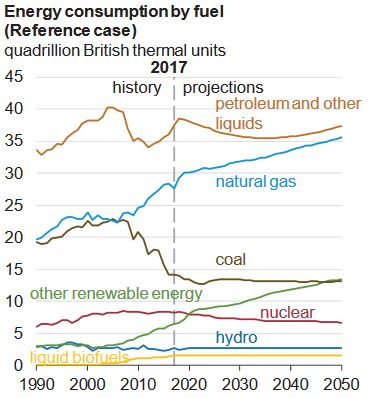

US energy consumption increases an average of 0.4 per cent per year, totalling around 13 per cent by 2050 (less than the annual rate of expected population growth of 0.6 per cent). Projections show that the consumption mix shifts over 2017-2050; natural gas is a standout performer and has the greatest growth rate on an absolute basis (figure 1).

Figure 1

Source: EIA, Annual Energy Outlook 2018

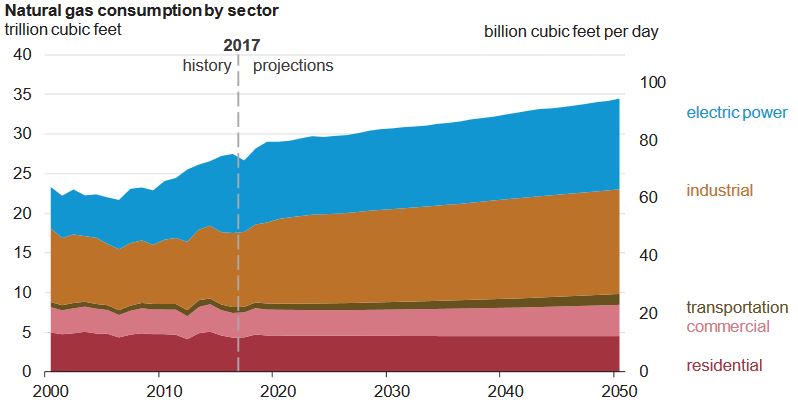

The industrial and electric power demand sectors are responsible for driving the growth of natural gas consumption (figure 2). The industrial sector accounts for the most natural gas consumption growth through to 2050. Electric power consumption increases, but at a slower rate. The report assumes that this growth is assisted by the scheduled end of renewable tax-credits in mid-2020. Consumption in the residential and commercial sectors remain relatively flat.

Non-hydroelectric renewable consumption grows the most on a percentage basis (figure 1). The report predicts that a combination of reductions in technology costs, coupled with state and federal policies to encourage the use of renewables, is expected to reduce the costs of renewable technologies, which in turn will support their wider adoption.

Figure 2

Source: EIA, Annual Energy Outlook 2018

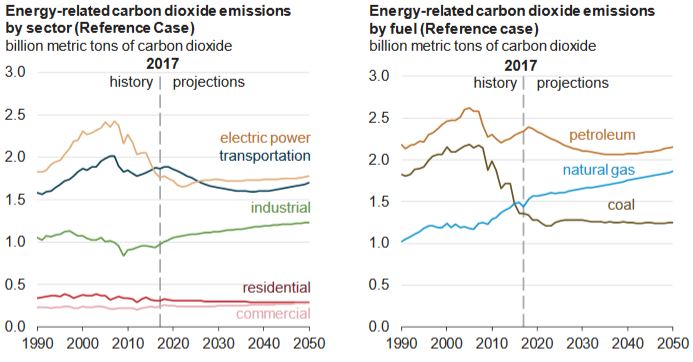

Energy-related carbon dioxide (CO2) emissions remain mostly flat through to 2050 (figure 3). Natural gas emissions grow at 0.8 per cent per year, while coal emissions decline at a rate of 0.2 per cent.

Figure 3

Mirroring consumption trends, emissions from the industrial sector increase the most (0.6 per cent annually), which can be explained by the relatively low cost of natural gas prompting an increase in usage and emissions.

For the electric power sector, emissions remain predominately flat to 2050. This is expected to be a result of a good natural gas market and government policies that encourage the uptake of renewables.

Figure 4

Source: EIA, Annual Energy Outlook 2018

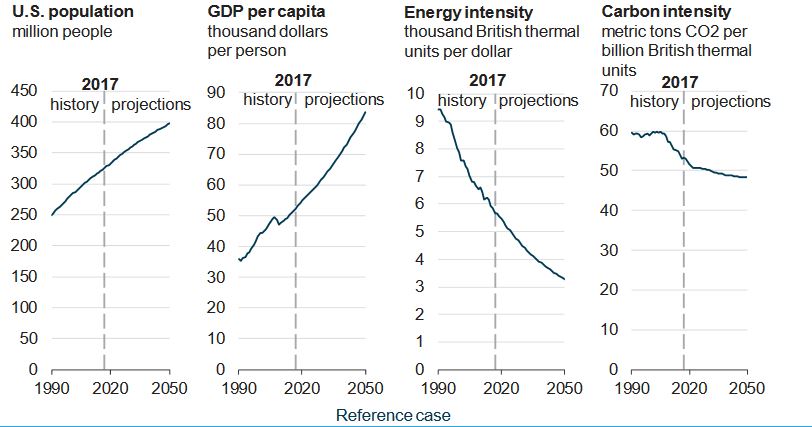

While both the country’s population and economy are projected to rise through to 2050, there is a decline in energy and emissions intensity “as energy efficiency, fuel economy improvements, and structural changes in the economy reduce energy intensity”.

By 2050, energy and carbon intensity are expected to be 42 per cent and 9 per cent lower respectively, when compared to 2017, which is expected to be due to the changes in the energy mix (figure 4).

Production

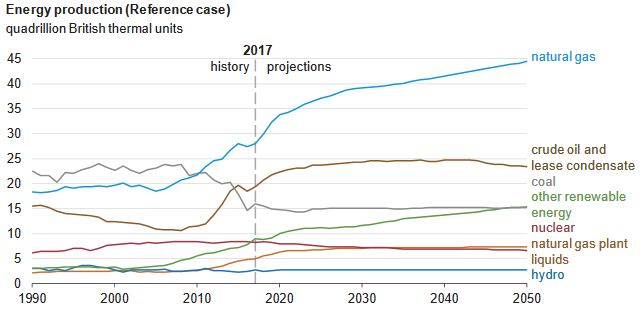

US energy production is projected to increase at a rate of 0.8 per cent annually, reaching around 31 per cent by 2050. This is led by increases in the production of non-hydroelectric renewables, natural gas and crude oil (figure 5).

Figure 5

Source: EIA, Annual Energy Outlook 2018 n.b. The growth modelled is largely dependent on technology, resources and market conditions, and assumes lower costs of producing resources and fast improvements in technology.

While US natural gas consumption grows, production surges at a higher rate. Natural gas forms the largest share of country’s total energy production, at almost 39 per cent by 2050. It is expected that shale gas and tight oil will account for more than three-quarters of natural gas by 2050.

Wind and solar generation grow the most on a percentage basis, accounting for 64 per cent of the total electric generation growth through 2050. Hydro, nuclear power and coal production remain relatively flat.

Demand and prices

Increases in energy efficiency has tempered US electricity demand, with the country experiencing flat growth for the past decade. Demand growth was negative during 2017, but it is projected to slowly increase through to 2050.

The AEO projects that electricity sales will grow 0.9 per cent annually - from 3.8 trillion kilowatt hours in 2017 to 5.1 trillion kilowatt hours in 2050[ii]. Growth in “direct-use generation” outperforms growth in retail sales, as the use of solar PV and natural gas-fired combined heat and power installations are more widely adopted.

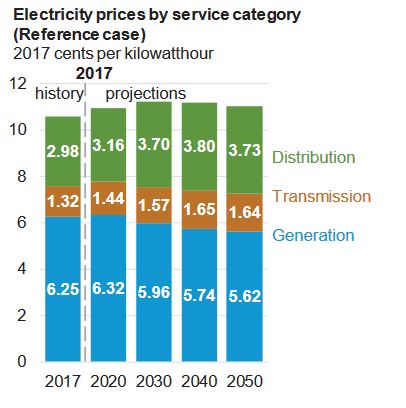

Average electricity prices are expected to remain low, moving between 10.6 to 11.0 cents per kilowatt-hour between 2017 and 2050 – a 3.7 per cent increase over 33 years (figure 6).

Figure 6

Source: EIA, Annual Energy Outlook 2018

When compared to 2017, the generation cost component of electricity prices is expected to decrease by 10 per cent by 2050, due to low natural gas prices and increased renewable generation (figure 6). Transmission and distribution cost components increase by 24 per cent and 25 per cent by 2050, respectively. The report states that this reflects the need to replace “aging infrastructure and upgrade the grid to accommodate changing reliability standards.”

Natural gas prices are projected to remain lower than $5 per million British thermal units through to the end of 2050. While the costs associated with adding new renewable electricity generation capacity are expected to steadily decline, especially for solar PV systems[iii].

As such, it is expected that the generation mix will be susceptible to the price of natural gas and the growth in electricity demand.

Projected energy mix

The US energy mix is projected to increase in the use of low, or no, carbon fuels. In the near term, fuel prices are anticipated to drive the share of natural gas and coal-fired generation.

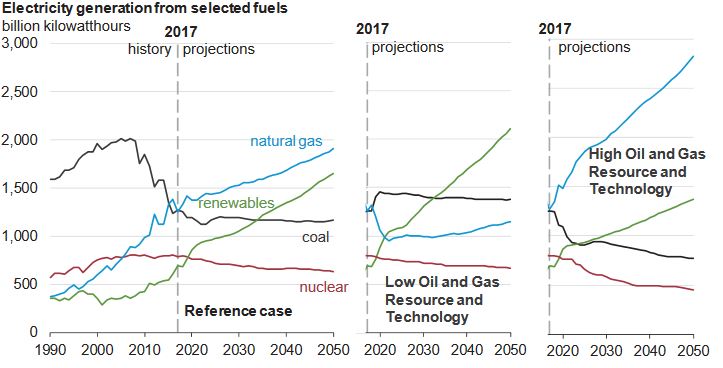

Natural gas and renewables are the primary sources of new generation capacity, which is helped by low natural gas prices and decreased renewable costs. Almost all new electricity generation capacity is from natural gas and renewables after 2022.

Natural gas generation is projected to soar, especially after the scheduled end of renewable tax credits in mid-2020. Shown in figure 5, natural gas dominates the reference case. However it especially thrives in the High Oil and Gas Resource and Technology case that assumes low natural gas prices, higher natural gas-fired generation, and less growth in renewables and coal-fired generation.

The higher natural gas prices in the Low Oil and Gas Resource and Technology case leads to increased levels of coal-fired generation.

Figure 7

Source: EIA, Annual Energy Outlook 2018

In the longer term, the AEO projects that the relatively low cost of coal will determine the decline of coal-fired generation. Coal capacity falls by 65 GW between 2017 and 2030, before levelling off to near 190 GW through to 2050. The report projects that high gas prices could slow the pace of coal retirements, and conversely, retirements are likely to increase if gas prices fall.

Cheap gas is also expected to trigger the retirement of 20 per cent of nuclear capacity. In the reference case, if natural gas prices decrease, nuclear capacity reduces from 99 GW in 2017 to 79 GW in 2050, with no new plant additions after 2020[iv].

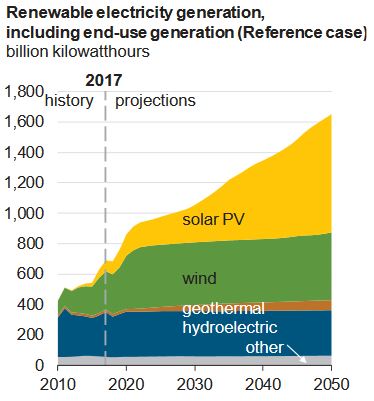

The AEO replaces coal and nuclear with natural gas, wind, and solar capacity. Low gas prices could limit the growth of renewables, but across all cases, they are still expected to steadily rise. Renewables are expected to grow 139 per cent, reaching 1650 billon kilowatthours by 2050. Wind and solar generation form 94 per cent of this growth.

Figure 8

Source: EIA, Annual Energy Outlook 2018

From 2020-2050, utility-scale wind capacity is anticipated to grow 20 GW, and solar PV, 127 GW. Generation from solar PV is expected to reach 14 per cent of total US electricity generation by 2050. The AEO projects that around 53 per cent of this total will come from utility-scale systems and 47 per cent from small-scale systems. While the growth of renewables will also lift utility-scale energy storage capacity by 34 GW.

Another strong trend identified by the AEO is the growth of battery powered vehicles, which we looked at in a previous article, found here.

Conclusion

The AEO’s energy market projections are subject to much uncertainty, for example, its reference case projections do not include the Obama administration’s Clean Power Plan, as there is a plan to dismantle it (the report does, however, look at the Clean Power Plan as a side case). As such, the future of the US energy markets will be highly susceptible to changing government policy over the projection period, as well as changing developments in technology and resources.

[i] EIA, Today in Energy, 6 February 2018

[ii] In this modelling, the average electricity growth rates in the high and low economic growth cases deviate the most from the reference case – high economic growth case is around 0.3 per cent point higher than the reference case, while low economic growth case is 0.3 per cent lower.

[iii] EIA, Today in Energy, 6 February 2018

[iv] Lower natural gas prices in the High Oil and Gas Resource and Technology case lead to lower wholesale power market revenues for nuclear power plant operators, accelerating the closure of an additional 24 GW of nuclear capacity by 2050 compared with the level in the Reference case. Higher natural gas prices in the Low Oil and Gas Resource and Technology case decrease the financial risks to nuclear power plant operators, resulting in fewer retirements of nuclear capacity (4 GW) through 2050 compared with the Reference case.

Related Analysis

International Energy Summit: The State of the Global Energy Transition

Australian Energy Council CEO Louisa Kinnear and the Energy Networks Australia CEO and Chair, Dom van den Berg and John Cleland recently attended the International Electricity Summit. Held every 18 months, the Summit brings together leaders from across the globe to share updates on energy markets around the world and the opportunities and challenges being faced as the world collectively transitions to net zero. We take a look at what was discussed.

Great British Energy – The UK’s new state-owned energy company

Last week’s UK election saw the Labour Party return to government after 14 years in opposition. Their emphatic win – the largest majority in a quarter of a century - delivered a mandate to implement their party manifesto, including a promise to set up Great British Energy (GB Energy), a publicly-owned and independently-run energy company which aims to deliver cheaper energy bills and cleaner power. So what is GB Energy and how will it work? We take a closer look.

Delivering on the ISP – risks and opportunities for future iterations

AEMO’s Integrated System Plan (ISP) maps an optimal development path (ODP) for generation, storage and network investments to hit the country’s net zero by 2050 target. It is predicated on a range of Federal and state government policy settings and reforms and on a range of scenarios succeeding. As with all modelling exercises, the ISP is based on a range of inputs and assumptions, all of which can, and do, change. AEMO itself has highlighted several risks. We take a look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.