by Justine Lovell

Transitioning to Net Zero: Different transitions, different paths

While there’s been much debate about how to make the transition to Net Zero, a new report aims to quantify the potential risks and financial implications if Australia’s path to decarbonisation is delayed.

The CSIRO report - Exploring Climate Risk in Australia - looks at the economy’s exposure to climate-related transition risk, and aims to be a “first step” to identifying which industries will have greater risks if the transition to Net Zero is delayed.

The scenarios

The CSIRO in collaboration with KPMG and Energetics, contrasted a ‘Current Policies’ scenario - a “business-as-usual” approach with current policies and rising global greenhouse gas emissions - with a ‘Delayed Transition’, where decarbonisation begins in earnest from 2030, resulting in a more rapid transition towards Net Zero emissions over the final two decades.

It says while Australia’s target of Net Zero emissions by 2050 provides an economic signal for decarbonisation, the current 2030 target of 26-28 per cent reduction on 2005 emissions could result in significant decarbonisation in the final two decades, leaving some sectors and states exposed to increased challenges. When compared to the business-as-usual approach, Australia’s CO2 emissions would have to drop around twice as much under a delayed transition scenario.

Impacts of delay: Sectors

Emissions intensive sectors decline in the delayed transition scenario due to the slowed but then rapid growth in renewables, electrification, and negative emission technologies during the final two decades to 2050. The report notes the key drivers include:

- replacement of the coal-fired generation fleet with more decentralised renewable electricity generation capacity;

- increased renewable energy installations driven by households and businesses; and,

- mechanisms allowing large energy users to reduce their electricity demand when supply is constrained.

While the analysis shows elevated risks to emissions intensive industries under the delayed approach scenario - particularly coal and to a lesser extent gas - the most exposed industries such as coal mining, fossil fuel dependent electricity generators, agriculture, and manufacturing, have greater exposure and the most to lose if they postpone action.

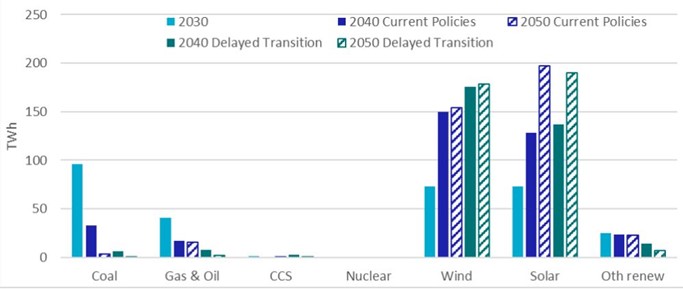

Figure 1: Australian electricity production TWh, by source in labelled period

Source: CSIRO, Exploring Climate Risk in Australia

Some of the report’s other key findings include:

- A delayed transition will likely require a high reliance on negative emissions technologies, such as direct air capture using ‘artificial trees’ or bioenergy with carbon capture and storage.

- A reliance on offsets (such as sequestering carbon in vegetation) could delay the transition to a low carbon economy if they are deployed in preference to decarbonisation and structural abatement.

- With a delayed transition, rapid decarbonisation delivers lower gross state product than under the current policies scenario in all states except the ACT.

- Methane emissions in the agricultural sector are also a key risk to Australia.

The report notes the impacts on industries like coal mining is “reasonably understood”, but there is less focus on other heavily affected industries, such as agriculture and emissions-intensive manufacturing. And while declines are shown in industries across mining, mineral processing, and agriculture, the sectorial impacts are “nuanced” - for example, according to the report:

- Coal mining and mineral processing, particularly ferrous metals, decline, yet the transition to a low carbon economy will require an increase in copper, nickel, lithium and other rare earth metals driven by batteries and electrification (more detail below).

- Hydrogen presents a significant opportunity for use within industrial processes such as steel production and decarbonising across industrial and residential heating uses.

The analysis also potentially understates some of the opportunities in emerging industries, such as hydrogen and commodities to facilitate low carbon industries. According to Dr Stuart Whitten, lead author of the report, the report “undersells” the physical risks of climate change, like extreme weather and climate-change events because they are difficult to predict. But it’s clear they will have negative economic consequences, with the latest Intergovernmental Panel on Climate Change (IPCC) report predicting that Australia can expect more hotter days, extreme fire weather, and heatwaves.

According to Dr Whitten there needs to be more awareness of how different risks interact with each other, especially when looking at connections across the globe, and says it’s worth highlighting the range of decarbonisation options already available:

“For example, increased electrification across the economy drawing on growth in renewables. Or reducing agricultural emissions through a range of crop and livestock practices. As more and more of these emerging technologies mature and are adopted by different sectors across our economy they will catalyse an even greater range of new opportunities that can make a material impact on emissions reduction.”

Impacts of delay: Across the states

Delaying action to Net Zero will leave the nation’s economy smaller according to the report, with the increased sectoral risks due to rapid decarbonisation flowing to households through increased cost-of-living.

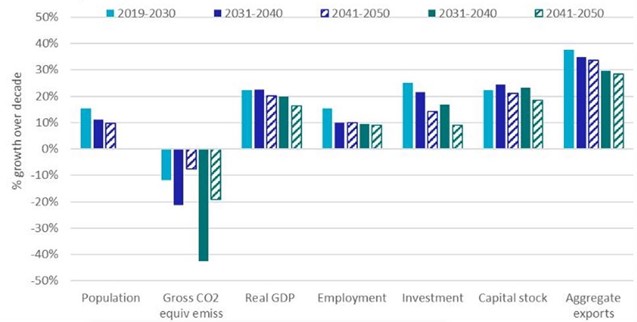

Figure 2: Australia, modelled percentage growth across labelled period

Source: CSIRO, Exploring Climate Risk in Australia

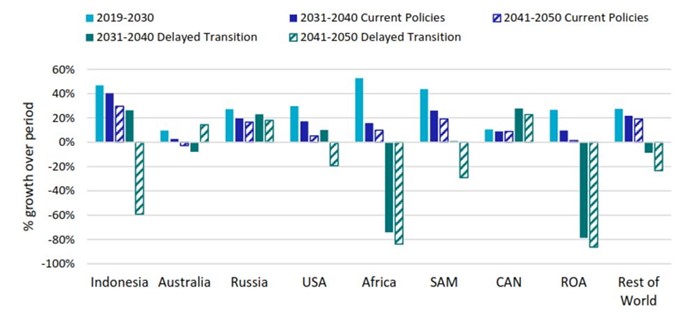

Impacts will vary across the nation, with some states more exposed than others. As a major supplier of thermal coal and gas, Australia is especially exposed to potential drops in export demand.

With a delayed effort, the need to rapidly decarbonisation between 2030-2050 would hit Queensland’s coal industry hardest with a “substantive” decline in exports due to the relative size of its export coal industry compared to the wider state-wide economy. New South Wales is similarly exposed, but coal exports form a smaller part of that state’s economy. Conversely, Western Australian iron ore and other mining are projected to grow.

However, the report notes:

“These impacts could be mitigated. Higher short-term decarbonisation targets coupled with domestic policy certainty could assist to smooth the transition, avoid shocks, allow coordinated transition plans to be developed for the most vulnerable industries, and enable higher confidence to attract investment in emerging low emissions industries and technologies.”

Figure 3: Coal exports, percentage growth over labelled period

Source: CSIRO, Exploring Climate Risk in Australia

By 2050, GDP per capita would be 5 per cent lower and there would be 1 per cent fewer jobs, under the delayed scenario. Relative to current levels, the overall economic impacts on household income and consumption are highest in New South Wales and Victoria. For example, higher input prices under the delayed transition scenario would hit the food manufacturing industry flowing through to higher cost-of-living for consumers.

What next?

While a lot of the public debate around Net Zero emissions has focused on changes to Australia’s electricity system, the report notes some challenges show less influence on the nation’s Net Zero trajectory.

The modelling shows Australia may not be as exposed in some areas, as first thought. According to Dr Whitten electricity generation had the clearest transition roadmap towards Net Zero, but industries such as mining and other emissions-heavy industries like mineral processing, are more exposed to risk:

“In the electricity sector, for example, we already have a strong transition plan … But in general, we can say that a faster transition will be a harder one for those fossil fuel intensive industries.”

Climate risk is complex, and according to the report the variability in results from its “relatively limited analysis” shows the importance of considering risks more generally and highlights the need for a more comprehensive transition risk assessment.

Regardless of the path taken towards Net Zero, the transition to decarbonise the economy would come at a cost - but the report claims a slower, orderly transition may cost less and improve future economic outcomes. And a lot of this risk could be mitigated:

“Higher short-term decarbonisation targets coupled with domestic policy certainty could assist to smooth the transition, avoid shocks, allow coordinated transition plans to be developed for the most vulnerable industries, and enable higher confidence to attract investment in emerging low emissions industries and technologies.

Related Analysis

Judicial review in environmental law – in the public interest or a public nuisance?

As the Federal Government pursues its productivity agenda, environmental approval processes are under scrutiny. While faster approvals could help, they will remain subject to judicial review. Traditionally, judicial review battles focused on fossil fuel projects, but in recent years it has been used to challenge and delay clean energy developments. This plot twist is complicating efforts to meet 2030 emissions targets and does not look like going away any time soon. Here, we examine the politics of judicial review, its impact on the energy transition, and options for reform.

Climate and energy: What do the next three years hold?

With Labor being returned to Government for a second term, this time with an increased majority, the next three years will represent a litmus test for how Australia is tracking to meet its signature 2030 targets of 43 per cent emissions reduction and 82 per cent renewable generation, and not to mention, the looming 2035 target. With significant obstacles laying ahead, the Government will need to hit the ground running. We take a look at some of the key projections and checkpoints throughout the next term.

Certificate schemes – good for governments, but what about customers?

Retailer certificate schemes have been growing in popularity in recent years as a policy mechanism to help deliver the energy transition. The report puts forward some recommendations on how to improve the efficiency of these schemes. It also includes a deeper dive into the Victorian Energy Upgrades program and South Australian Retailer Energy Productivity Scheme.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.