by Ben Skinner

The Wholesale Demand Response Mechanism: Leading a horse to water

After being first recommended in 2011 by the Australian Energy Market Commission’s (AEMC) Power of Choice Review, and followed by a decade-long passionate debate, the Wholesale Demand Response Mechanism (WDRM) was finally implemented on 24 October 2021. Two years later we look back and see if it was worth all the effort.

The WDRM is some peculiar accounting derived from North American electricity markets. When a WDRM load self-curtails, their retailer is charged by Australian Energy Market Operator (AEMO) as if the load stayed on, meaning AEMO over-recovers some funds. These funds are credited to a WDRM agent, who will share them with the customer. The accounting is complex, requiring deemed consumptions profiles, but if it works out the way intended, it results in the same outcome as if the retailer had managed the Demand-Response (DR) in the conventional way.

So why bother creating a complex system just to achieve what was always possible? The push for a WDRM arose from a belief that energy retailers were suppressing DR against their own self-interest. This is despite the fact a customer with DR can readily switch to another retailer – the belief rests on the entire retail sector being in on the game. By introducing a new party who is supposedly more friendly to DR, reluctant retailers would be bypassed so DR could thrive.

After two years only one WDRM agent is active, and, despite 2022 having the highest prices in the history of the National Electricity Market (NEM), the peak DR activated through WDRM was only 30MW, and has been even less in 2023. To say this is underwhelming is understatement. The industry put itself through a decade-long argument about whether to build a WDRM, and then invested real systems dollars in what appears to be a white elephant.

With hindsight, given the strange theory that justified it, this outcome was entirely predictable. It might also tell us that while DR looks great in theory, in practice we shouldn’t expect it to play more than a niche role. The prosaic truth is that customers simply have more important things to care about. Retailers have always known this, but economists tend to assume away practicalities when contemplating the elegance of a supply/demand chart.

Today we see what learnings we can take from the saga that gave us the WDRM.

Demand Response and the Wholesale Market

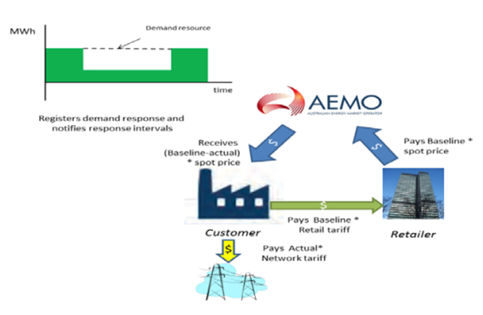

When a retailer engages a customer, it takes responsibility for the spot purchases from the AEMO on its behalf. The spot price is notoriously volatile, so the retailer normally deals with this by hedging against that volatility. However, it can also get the customer to reduce consumption in those periods when prices spike – this is conventional DR. Because the retailer avoids high spot prices it gains a benefit, which it shares with the customer.

Figure 1: Conventional Demand Response

Source: AEC

The process is simple, and because it is physically metered, entirely accurate. The retailer and the customer will have to discuss how much load was actually curtailed and the sharing of the benefit, but that is entirely between them to negotiate. DR has always happened in the NEM through this simple approach.

When economists look at the NEM’s brief summer demand peaks, they see an inefficient use of capital. Surely more large customers could voluntarily interrupt their load at these times and address that inefficiency? In the NEM, DR exists in the hundreds of megawatts, but economists want to see it in the multiple Gigawatts to flatten out the peak.

But why do we not see Gigawatts? After all, the NEM’s high price cap should create a strong incentive to make load responsive.

It is often incorrectly assumed that if a retailer is hedged, or owns its own generation, it lacks incentive to use DR. But that is false as a hedged retailer’s marginal profitability improves when DR is used during high prices just as much as an unhedged one. Indeed, if it has confidence in the DR ahead of time, a retailer can reduce the amount of hedging it has to buy, which is highly advantageous to it.

Nevertheless, this incorrect assumption persists and gave rise to the WDRM.

The Power of Choice Review

This broad review of customer engagement in the NEM was carried out by the AEMC in 2011-2012 and made many far-reaching and significant recommendations, including competitive metering and the sharing of customer data with third parties. It also recommended:

“Task AEMO with developing a rule change proposal to establish a new demand response mechanism that allows consumers, or third parties acting on consumers’ behalf, to directly participate in the wholesale market and to receive the spot price for the change in demand.”

This came from a view that retailers were failing to exploit DR, and that if instead the benefit stream were to come directly from AEMO to the customer, or a “third party acting on consumers’ behalf”, then more DR would emerge. The implication of the above comment is that retailers are not “acting on consumers’ behalf”, despite customers being able to easily switch retailers. Instead, yet another intermediary should become involved who will, for some reason, be more benevolent to the customer than the retailer the customer had chosen to represent them.

Figure 2: Broad design of WDRM

Source: AEMC Power of Choice Review Final Report

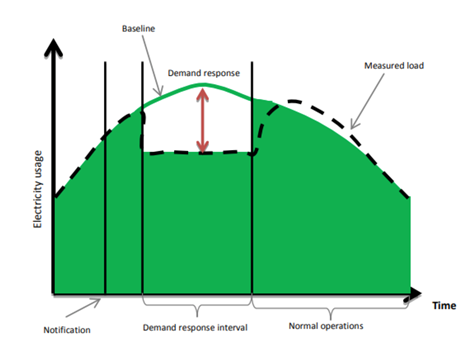

The idea was that retailers would be charged, by AEMO, as if the demand response did not occur, i.e. they are settled on a hypothetical “baseline”. Then, because actual metered consumption is lower than this baseline, AEMO would collect a surplus. This surplus would be passed to the customer, or more likely, a third-party agent who manages the whole process. Importantly, retailers could not veto the arrangement from their customers, even though they are responsible for all other wholesale purchases on behalf of that customer.

Figure 3: Baselining

Source: AEMC Power of Choice Review Final Report

The obvious challenge is that this baselining represents a hypothetical consumption that cannot be metered. It must be guessed by looking at the consumer’s consumption patterns on similar days and rest of that day. Customer consumptions are rarely stable, and errors are common, such as a factory’s unrelated outage being misinterpreted as DR. And it introduces incentives for gaming, such as happened in the US with the turning on the floodlights of an empty baseball park in order to lift a baseline ahead of a price spike.

A tortuous journey and a culture war

Things did not go smoothly after Power of Choice. AEMO discovered developing the WDRM in 2013 was complex, with considerable costs, and faced industry opposition. AEMO dutifully developed a design, but they did not follow Power of Choice’s recommendation of sending it back to the AEMC as a rule change. AEMO were unsure that the benefits exceeded the costs, so instead passed it to the Energy Council (NEM Energy Ministers) to decide what to do.

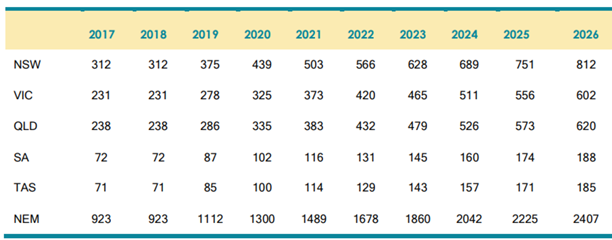

Ministers then engaged a cost-benefit advice that anticipated costs of $112m over 10 years, but also forecast a take-up that, in hindsight, looks quite absurd.

Figure 4: 2014 Estimation of WDRM (MW) take-up assuming 2017 implementation

Source: Cost-benefit analysis of a possible Demand Response Mechanism, Oakley Greenwood

With this optimistic outlook, in 2015 the Energy Council proposed the WDRM, inter alia, as a formal rule change to the AEMC, who in 2016, agreed to the inter alia but rejected the WDRM in no uncertain terms:

In light of the absence of any regulatory barriers in the Rules to the uptake of demand side participation, the Commission has not made a rule to implement the proposed demand response mechanism. The Commission acknowledges that demand response can be of benefit where it is an efficient form of market response to price signals. However, the proposed mechanism is costly and adds little benefit to consumers, because the benefits of demand side participation can, and already are, accessible under current arrangements. While the Commission acknowledges that there may currently be commercial reasons that complicate access to demand response for some consumers, implementing a market wide mechanism in the Rules, at considerable cost to all consumers, is not the appropriate vehicle to address these reasons. Nor would it encourage an efficient level of demand response.

NEM supply got tighter with the closures of Northern Power Station in 2016 and Hazelwood in 2017. The 2017 Finkel Report , only 7 months after the above strong words of rejection, put the WDRM right back on the table with its recommendation 6.7:

The COAG Energy Council should direct the Australian Energy Market Commission to undertake a review to recommend a mechanism that facilitates demand response in the wholesale energy market. This review should be completed by mid-2018 and include a draft rule change proposal for consideration by the COAG Energy Council.

In 2017 and 2018 the AEMC conducted the Reliability Frameworks Review where it was discussed as an option to assist managing peak demand. In 2018 the ACCC Retail Electricity Pricing Inquiry made the WDRM its recommendation 21.

In August 2018, the WDRM was re-proposed as a rule change to the AEMC. One might have expected it to have been proposed by a large customer, or their representative, the Energy Users Association of Australia. Instead, it was proposed by a trio of progressive think-tanks, the Public Interest Advocacy Centre, the Total Environment Centre, and The Australia Institute. And, under new leadership, AEMO discarded its 2013 doubts and strongly embraced it.

By now the WDRM saga had moved beyond its dry self into something of an absurd culture war, with the industry on one side and its critics on the other. In a 2022 conference, John Thwaites, formerly chair of the panel that led to the regulation of Victorian retail prices, went as far as linking the delays in implementing the WDRM to the lack of an environmental objective in the National Electricity Law.

Meanwhile the customers for whom it was intended remained out of the debate, which should have been taken as an indication of their interest in the WDRM itself.

Reducing system costs

The industry certainly feared having to invest in systems changes, but also, perhaps believing those ambitious forecasts, saw business risks arising due to baseline settlements and threats through the bypassing of the retailer business model. Seeing so many powerful forces lined up in support of the WDRM, under duress and far too late, the Australian Energy Council (AEC) proposed a minimalist alternative rule of a DR register. This was rejected, and the AEMC ultimately made the WDRM rule broadly along the Power of Choice design.

AEMO’s 2013 WDRM detailed design spread over 102 pages of changes to registrations, metering, settlements, B2B systems, prudentials and reporting. One of the biggest sources of WDRM systems costs came from every retailer having to change their billing systems such that it could calculate a customer’s retail tariff from a baseline volume, rather than metered volume.

Late in the process, the AEMC adjusted the 2013 design by instead having AEMO recover this payment from the customer rather than having the retailer do it, using a “reimbursement rate” as a proxy for a retail tariff. This unintuitive, yet ingenious, alteration somewhat increased AEMO’s systems build costs, but greatly lowered retailers’, and therefore the overall systems costs of the WDRM. It also allowed AEMO to accelerate the implementation timetable, as it didn’t have to wait for retailers to change their systems.

Indeed, with this altered design, retailers had negligible up-front costs, with their risks and costs only emerging upon WDRM usage, which, as we know now, turned out to be a non-issue.

Nevertheless, AEMO’s build costs remained material, but, if it led to an expansion of DR in the way predicted back in 2014, it would surely be worth those costs?

You can lead a customer to a mechanism but you can’t make it drink

The WDRM was originally proposed into the Power of Choice review by energy services company, Enernoc, now Enel X. In 2023, two years after implementation, Enel X remain the only registered Wholesale Demand Response Service Provider. They have registered a maximum response of 67 MW, however not all of this is available at any one time, and the use briefly peaked at 30MW.

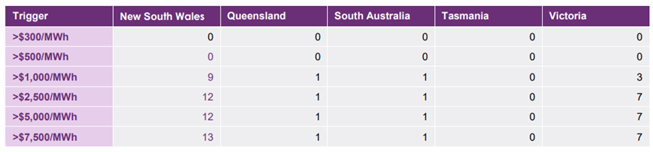

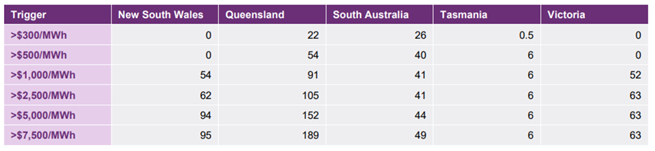

AEMO’s 2023 Electricity Statement of Opportunities (ESOO) has provided a very underwhelming forecast of the use of WDRM at increasing price triggers. At high prices, they expect 22MW will be dispatched out of a demand that peaks at 35,000MW.

Figure 5: WDRM forecast at increasing price trigger levels

Source 2023 Electricity Statement of Opportunities

Whilst still not large, AEMO’s prediction for conventional, retailer-controlled DR swamps WDRM.

Figure 6: WDRM plus Conventional DR forecast at increasing price trigger levels

Source 2023 Electricity Statement of Opportunities

The NEM’s total take up of price-responsive DR (figure 6) is often unfavourably compared to much larger shares of DR in US capacity markets and even AEMO’s success in recruiting emergency DR through the Reliability and Emergency Reserves Trader (RERT) function.

Being an energy-only market, the NEM’s price-responsive DR only creates value when it is actually used. However, in capacity markets and the RERT, registered DR is paid upfront regardless of whether it is used. After that they are exercised only as a last resort, which means that in most years, the DR will earn a fixed fee, despite never being called. If it is called, but fails to respond, penalties are capped at the annual availability fee. This means there is no downside for a customer against entering such an arrangement. This is certainly attractive from the customer’s standpoint, but it is doubtful how reliable this DR would be were the power system to suffer an unexpected crisis.

Accepting that price-responsive DR will probably not play a great role in the NEM, why is WDRM even less successful than retailer controlled DR? The fact is that DR was never resisted by retailers. There is no reason to expect that one intermediary, a WDRM agent, would achieve anything better than another, the retailer. In the unlikely event a customer’s retailer were disinterested in exercising its DR capability, they can just find another retailer who does, rather than complicate things with yet another intermediary. The WDRM’s original commercial proponent presumably also reached that conclusion and in 2020 registered as a retailer itself.

Conclusion

The WDRM is a concept which never stood up to impassionate scrutiny but was nevertheless pursued on the back of “us versus them” myths. After thousands of pages of regulatory study, consultant work and submissions, its outcome is clearly not worth the decade of policy distraction that the industry and its stakeholders subjected themselves to. Fortunately, a last-minute design change mostly limited the damage to AEMO systems costs.

Nevertheless, some stakeholders are still not cutting their losses on the folly that was the WDRM. The recent NSW Electricity Supply and Reliability Check Up has observed this low take up and in recommendation 35 proposes that the NSW government itself participate in the WDRM in order to at least demonstrate it.

One has to wonder long we will keep bringing this horse to water when it doesn’t want to drink.

Related Analysis

From Energy to Flexibility: Rewiring Australia’s Wholesale Markets for Net Zero

Australia’s path to net zero will depend not only on new technologies, but on fundamentally reshaping the markets that underpin the energy system. As coal exits, renewables, storage and consumer energy resources will drive a far more dynamic and decentralised National Electricity Market, where flexibility becomes the critical commodity. We explore the market reforms, investment signals and system changes required to deliver a secure, affordable and reliable Energy2050 future, themes that will also sit at the centre of the Australian Energy Council Conference 2026 in Sydney on 4 June.

Is increased volatility the new norm?

This year has showcased an increased level of volatility in the National Electricity Market (NEM). To date we have seen significant fluctuations in spot prices with prices hitting both maximum price caps on several occasions and ongoing growth in periods of negative prices with generation being curtailed at times. We took a closer look at why this is happening and the impact this could have on the grid in the future.

Is there a better way to manage AEMO’s costs?

The market operator performs a vital role in managing the electricity and gas systems and markets across Australia. In WA, AEMO recovers the costs of performing its functions via fees paid by market participants, based on expenditure approved by the State’s Economic Regulation Authority. In the last few years, AEMO’s costs have sky-rocketed in WA driven in part by the amount of market reform and the challenges of budgeting projects that are not adequately defined. Here we take a look at how AEMO’s costs have escalated, proposed changes to the allowable revenue framework, and what can be done to keep a lid on costs.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.