by Rhys Thomas

The 82 per cent national renewable energy target – where did it come from and how can we get there?

In recent weeks there has been a wave of headlines about Australia’s energy transition – while some preached opportunity, others raised caution. Of particular interest to those inside the energy beltway was whether Australia can reach its official, yet also unofficial, target of 82 per cent national renewable electricity generation by 2030.

In this article, we do a deep dive into how this target came to be and what obstacles must be overcome for Australia to achieve it.

Where did 82 per cent come from?

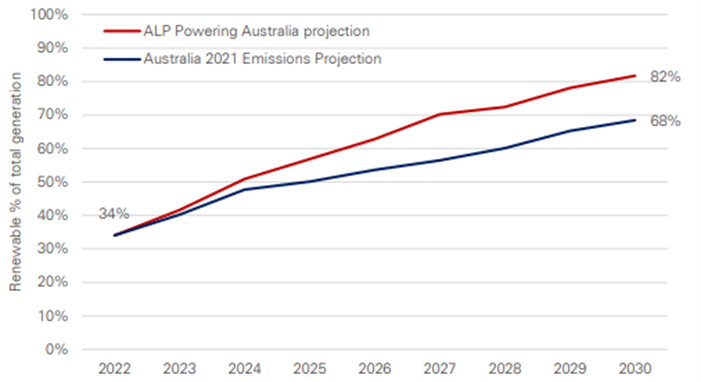

The figure first emerged through modelling the Labor Party did while in Opposition. In the lead up to the 2022 Federal Election, the ALP commissioned RepuTex, an energy economics consultant, to model the impacts of its Powering Australia Plan. Key to this was Labor’s Rewiring the Nation policy – a $20 billion fund to accelerate investment in electricity transmission projects. RepuTex predicted that the successful implementation of this policy would increase overall renewable generation in the National Electricity Market (NEM) to 82 per cent by 2030. In turn, this increased NEM renewable penetration would help Australia reach its updated 43 per cent by 2030 total carbon pledge.

82 per cent of the NEM was thus calculated as a beneficial outcome of the Rewiring the Nation policy rather than reverse (i.e. the policy being presented as a means to achieve a specific renewable target).

Figure 1: Forecast Generation of Renewable Energy in the NEM

Source: Reputex (p9)

When formally announcing its Powering Australia Plan in December 2021, the ALP did not give this figure huge prominence. It was not mentioned in its official media release nor did it receive any attention on the Powering Australia website.

It was, however, referenced in media activity surrounding the announcement, such as this speech by Labor leader Anthony Albanese which described Powering Australia as “Labor’s plan to boost renewables to 82 per cent of the grid by 2030”. This speech did not clarify that the ‘grid’ referred only meant the NEM.

82 per cent gains a life of its own

While it is never easy reading political tea leaves, it seems 82 per cent was never intended to be a target or policy in itself, emerging primarily from political and media repetition from the above speech. With the nuance soon lost in the maelstrom of election campaigning, many journalists and lobby groups started talking about a nationwide 82 per cent renewable share as official government policy.

Figure 2: Responses to release of Powering Australia Plan

Source: Smart Energy Council Media Release

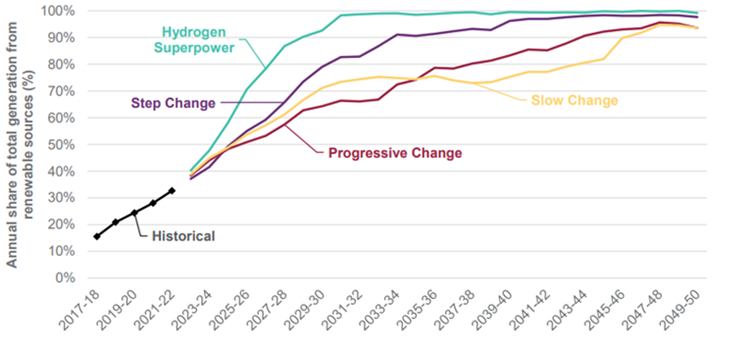

Somewhat incidentally, the 82 per cent outcome was bolstered by the publication of the Australian Energy Market Operator’s (AEMO’s) Integrated System Plan (ISP) in June 2022. The ISP’s Step Change scenario, the scenario which AEMO sees as most likely to occur, forecast renewable generation in the NEM to reach 83 per cent in 2030-31.

Figure 3: Annual Share of Total Generation From Renewable Sources (Each Scenario, Optimal Development Path)

Source: AEMO Integrated System Plan (p45)

This alignment does seem coincidental. The ISP’s inputs and assumptions reflect long and rigorous stakeholder engagement that occurred before the change of government in May 2022.

AEMO’s Step Change scenario (just like the RepuTex scenario before it) are both the results of economic modeling. These models build plants according to estimates of relative costs. They do not, and cannot, reliably consider all the complexity of practical matters that afflict the real world, such as supply chain limits and planning approval delays. Indeed, economic modelling is precisely useful because it paints a picture of what could happen if the economy was unconstrained by such practical limitations, prompting focus on such constraints.

Perhaps this was internally understood because AEMO’s ISP did not lead to any immediate shift in government rhetoric toward 82 per cent becoming a target. The figure was not part of the targets enshrined in the Climate Change Act and was sparsely mentioned other than during international engagements – the Minister for Climate Change and Energy, Chris Bowen, talked about Australia “working towards” 82 per cent in a speech to the United States and, when signing a global offshore wind alliance, noted how it can “support Australia’s ambition to get the grid to 82% renewable energy by 2030”.

82 per cent - ambition or target? NEM or national?

This is where things start to get confusing. Both the RepuTex and ISP scenarios were modelling (rather than recommending) renewable generation levels by 2030 and were NEM only.

But then in December 2022, when the Federal Government published its first Annual Climate Change Statement, it highlighted Australia’s achievement of “committing to an 82% national renewable electricity target by 2030”.

More explicitly than that, Australia’s Emissions Projections (published at the same time) included the following policy assumption:

A national renewable electricity target of 82% by 2030: It is assumed that the share of renewable energy is increased to 82% of electricity generated in Australia’s electricity grids (National Electricity Market, Western Australia’s Wholesale Electricity Market, the Darwin-Katherine Interconnected System, and the North-West Interconnected System) by 2030, supported by Rewiring the Nation.

So somewhere along the way a NEM-only projection has transformed into a concrete national target. Unlike the 43 per cent carbon target, however, it is not legislated nor is there an expectation that it will be.

What difference does it make?

The difference between a projection and target may sound semantic, but it has policy implications. Having a target (albeit not in law) will compel action because it places political responsibility on the government to design policies to get there. In fact, the recent addition of an environment objective into the National Energy Objectives requires policymakers to consider “the achievement of targets … that are likely to contribute to reducing Australia’s greenhouse gas emissions”. This clause has been interpreted to cover jurisdictional renewable energy targets, even if they are not in law (they just need to be a “public commitment”).

The downside to all this is, of course, politicisation – bureaucracies and policymakers may implement inefficient policies to meet what is ultimately an arbitrary figure.

The difference between a NEM-only and national scope is more substantial and only increases the already enormous amount of effort and resources needed to reach 82 per cent. This difference is probably best illustrated through recent data contained in the AEC’s Electricity Gas Australia publication:

During financial year 2021-22, there were 30 new projects with a total capacity of 1,923 MW of solar, 1,420 MW of wind and 547 MW of battery storage commissioned across the National Electricity Market (NEM). No new projects were commissioned in Western Australia or the Northern Territory during the year.

So is 82 per cent achievable?

Much has already been made about the extraordinary levels of investment required to transform the NEM electricity grid, with AEMO putting this figure at $320 billion to achieve its Step Change scenario. In raw technology terms, about 16TWh of renewables must be built within the next decade to meet the 2030 target (just in the NEM). Recent data from the University of NSW indicates that Australia’s renewable deployment is about half this, at about 8.5TWh of solar and wind generation. Unfortunately, every year of under-deployment makes the target less achievable.

Contrary to what is sometimes said, the build rate is not constrained by political will or investor appetite. Rather, it is simply a reality of the social, technical, and engineering challenges that come with such a whole-of-society transformation.

The challenges here are many:

Supply-chain limitations on the minerals and complex equipment required to build and connect large-scale renewables.

Normal limitations that come through global competing demand and cost have been exacerbated by Covid-19 disruptions, Russia’s invasion of Ukraine, and growing ESG requirements, particularly around modern slavery. A Clean Energy Council report from late last year about Addressing Modern Slavery in the Clean Energy Sector said “the main points of exposure include the manufacture of components and the extraction of raw material”.

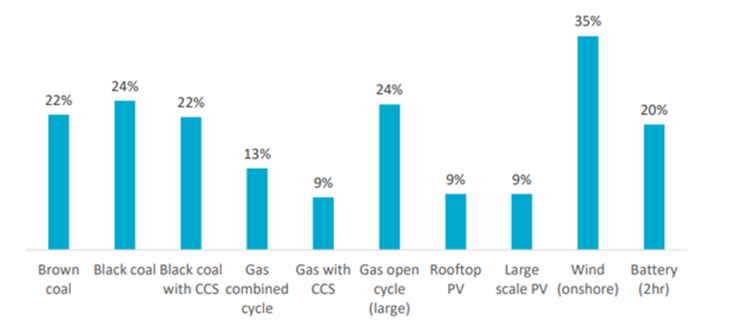

The impacts of these supply-chain constraints were corroborated in the latest CSIRO GenCost 2022-23 report, which found the capital costs for all energy technologies have increased, with the largest increase being for onshore wind. CSIRO does not expect these wind costs to return to normal until at least 2027.

Imported products also bring other time lags, such as lead times and finding foreign suppliers compliant with Australian Standards.

Figure 4: Annual Increase in Capital Costs by Technology

Source: CSIRO GenCost 2022-23 (p14).

Skill shortages, particularly with respect to electrical networks.

The energy infrastructure projects required to reach 82 per cent will create new employment opportunities. Many of these opportunities are nuanced and required advanced skills and experience in electrical engineering. Engineers Australia has cautioned that there is currently not enough engineering capability to meet this demand and “without immediate attention, skill shortages may become a significant impediment to the realisation of the energy transition”.

Compounding this is that the common antidote to domestic skill shortages, attracting skilled migrants, has been frustrated by Covid-19.

Land-use resistance to network infrastructure and extended permitting processes.

Farmer groups are increasingly vocal in their resistance to proposed transmission projects, raising concern about poor consultation and misuse of productive farmland. The Federal Government has announced a review into “community engagement practices related to the development of renewable energy infrastructure” to try and ensure there is a social licence for new electricity infrastructure projects.

If history is any guide, there will be other unplannable delays resulting from local community appeals. One such example is the relatively modest Brunswick Terminal Station 66kV expansion in Victoria. Originally proposed in 2006 after a very favourable cost-benefit analysis, when faced with a small but vocal local community, the expansion took over 10 years to come online due to coordinated court appeals.

Extended design, technical approval and build times for connection assets, stabilization equipment (e.g. synchronous condensers), long-distance transmission and pumped-hydro storage.

As conventional plants close, there is growing global demand for stabilisation equipment to provide the essential system services needed to keep the grid stable. This demand is not currently matched by supply, creating delays.

Slow progress in developing the necessary tools to understand the complex phenomena resulting from deep penetration of inverter-based resources on a large electrical grid.

At Australian Energy Week, AEMO CEO Daniel Westerman explained that its “operational technology is not keeping pace with advances on the power system”. Capability uplift is underway but will take some years to be fully implemented.

These challenges are not insurmountable. But whether they can be overcome by, let alone before, 2030 to reach the NEM only target is another question.

For non-NEM electricity grids, there are all these challenges and more.

- The absence of existing hydro generation in these grids means they are starting from a lower base point (the NEM has about a 10 per cent head start on total renewable generation thanks to legacy hydro).

- Variable renewables cannot be backed up by the flexible dispatchability of conventional hydro, and there appear to be no options for “deep” hydro pumped storages akin to the Snowy Mountains and Tasmania.

- Smaller grids with less capacity have even greater difficulty managing high renewable penetration because, being geographically concentrated, they cannot as easily take advantage of diversity in the timing of demand peaks and wind generation.

On top of all that, the largest non-NEM grid, the South-West Interconnected System (SWIS) of Western Australia, has a notoriously slow process for connecting new generators and building out constraints[1].

Conclusion

Nobody wants to be that person that says something cannot be done and setting a target helps keep the pressure on the government, industry and AEMO to deliver the energy transition. But, as 2030 gets nearer, it is important decarbonisation occurs at least cost, not any cost.

Regardless of the many practical difficulties above in achieving this target by 2030, we can nevertheless be confident that 82 per cent of national electricity generation, indeed more, seems certain to be achieved in the early 2030s.

[1] See section 3 of https://www.erawa.com.au/cproot/23089/2/AA5-Further-Access-Arrangement-Information-18-Jan-2023-redacted_Redacted.pdf

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Community Power Network Trial: Potential risks and market impact

Australia leads the world in rooftop solar, yet renters, apartment dwellers and low-income households remain excluded from many of the benefits. Ausgrid’s proposed Community Power Network trial seeks to address this gap by installing and operating shared solar and batteries, with returns redistributed to local customers. While the model could broaden access, it also challenges the long-standing separation between monopoly networks and contestable markets, raising questions about precedent, competitive neutrality, cross-subsidies, and the potential for market distortion. We take a look at the trial’s design, its domestic and international precedents, associated risks and considerations, and the broader implications for the energy market.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.