by Australian Energy Council

Storage across the NEM

In a speech in March this year, AEMC Commissioner Tim Jordan stated: “…by AEMO’s current calculations, outlined in the ISP, 61 GW of storage capacity is needed by 2050 under the Step Change scenario. That’s 17 times current levels.” Federal and state governments have announced various policies to stimulate battery investment, but challenges to their development are starting to emerge.

Here we take a look at current proposals for storage across the NEM and their implications.

What does AEMO say?

AEMO’s Electricity Statement of Opportunities (‘ESOO’) was published last month, and forecasts in its Central scenario some large storage projects to be operational by the end of 2032-33:

- Kidston Pumped Hydro Energy Storage (250 MW/2,000 megawatt-hours [MWh]) in Queensland from February 2025/26.

- Snowy 2.0 (2,040 MW/350,000 MWh) in New South Wales by December 2029.

- More than 5,241 MW/11,054 MWh of utility-scale batteries, including Eraring Big Battery, Hazelwood Battery Energy Storage System (BESS), Orana BESS, Swanbank BESS, Torrens Island BESS, and Wooreen BESS.

Converting decommissioned power stations into large-scale battery storage is proving an efficient way to capitalise on existing electrical infrastructure (e.g. switchyards). The AEC has produced a guidance report highlighting considerations for this type of project.

In addition to the ESOO-listed projects, which are considered advanced in nature, there are many new projects hoping to progress towards completion:

- In December 2022, ARENA announced funding for eight grid scale batteries worth $2.7 billion, which will a capacity of 2.0 GW / 4.2 GWh. ARENA states that these projects represent a tenfold increase in grid-forming electricity storage capacity currently operational in the National Electricity Market. The specific projects and their proponents are:

- AGL: a new 250 MW / 500 MWh battery in Liddell, NSW.

- FRV: a new 250 MW / 550 MWh battery in Gnarwarre, VIC.

- Neoen: retrofitting the 300 MW / 450 MWh Victorian Big Battery in Moorabool, VIC to enable grid-forming capability.

- Neoen: a new 200 MW / 400 MWh battery in Hopeland, QLD.

- Neoen: a new 200 MW / 400 MWh battery in Blyth, SA.

- Origin: a new 300 MW / 900 MWh battery in Mortlake, VIC

- Risen: a new 200 MW / 400 MWh battery in Bungama, SA.

- TagEnergy: a new 300 MW / 600 MWh battery in Mount Fox QLD.

- In February 2023, Infradebt, backed by Mike Cannon-Brookes, announced $1 billion to finance the construction of six to eight batteries with a total capacity of 1.5 to 2 gigawatts. The first two projects to be financed are:

- Neoen: a new 100MW / 200 MWH battery in the ACT

- Genex Power: a new 50MW/100MWh BESS in Queensland

While there is no shortage of projects, it is still a long way away from the $64 billion of storage investment AEMO forecasts is needed in its Step Change scenario. This might be one reason why governments are stepping in.

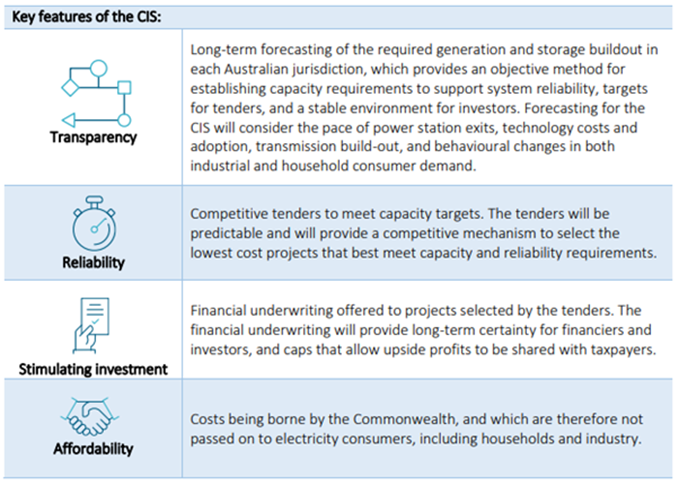

The Capacity Investment Scheme

In December 2022, energy ministers agreed to support the design of a Capacity Investment Scheme (CIS) in order to encourage investment in new dispatchable capacity into Australia’s energy grid. In August 2023, the Department of Climate Change, Energy, Environment and Water commenced consultation on the Capacity Investment Scheme.

The CIS aims to add $10 of investment to secure 6GW of “clean dispatchable capacity to the grid by 2030”. On 29 June 2023, the Commonwealth and NSW governments announced that the CIS would support an additional 550MW of firmed renewable generation in the state. In the announcement, both governments cited the 3.3GW of capacity submitted to the NSW 380MW firming tender round as evidence of an appetite to install additional firmed renewables in NSW.

The scheme will operate through a series of competitive tenders, where the commonwealth will offer long-term underwriting agreements for an agreed revenue “floor” and “ceiling” or “collar” arrangement. In its August 31 submission to the Capacity Investment Scheme consultation paper, the AEC identified several complexities that arise because of the collar arrangement, namely:

- difficulties developing a financial model to determine the implications of different strike prices for the cap and floor, in order to inform a competitive tender;

- difficulties for the government and AEMO Services in comparing the implied value of competing offers as tenderers are able to adjust numerous variables;

- potentially perverse incentives in relation to triggering collars;

- lowered market operational incentives when the collar is triggered or near its triggers;

- difficulties in accurately measuring total revenue from the broad range of revenues and costs

- the capacity is exposed to;

- incentives to structure arrangements, especially contracting, to minimize measured revenue;

- an unknowable and unlimited government trailing financial exposure to the collar.

The AEC has taken the view that the collar’s complexities outweigh its benefits to the market.

A simpler alternative might be one that provides only fixed competitive grants upon completion or paid progressively according to availability. Under this model, the government would have no trailing liabilities, and, after completion, all ongoing market risks would be retained by the capacity.

Figure 1: Key features of the CIS

Source: Capacity investment Scheme Consultation Paper

The CIS will utilize the AEMO ISP and the ESOO to produce its own reliability modelling, though it seems certain elements of the modelling process could be improved to reflect the reality that the delivery of firm output is for the purpose of customers, and best located at load centres. The current proposed structure of the CIS allows states to specify that projects must be located within a declared Renewable Energy Zone (REZ). It would seem preferable for locational incentives to arise only through market design.

It is important to note that the CIS has proposed a minimum project size of 30MW (AEMO registered capacity). As part of the consultation process, DCCEEW is seeking feedback on the evaluation criteria it should implement to assess a project’s contribution to system reliability – that is, the project’s potential contribution to avoid unserved energy events and to the reliability standard.

$62 billion Queensland Energy and Jobs Plan

On 28 September 2022, the Queensland government announced its $62 billion Queensland Energy and Jobs Plan which included plans for two new pumped hydro plans delivering up to 7GW of storage capacity. The plants are to be owned and run by a new entity called “Queensland Hydro.” The two new plants are called Borumba (proposed to be constructed near the Sunshine Coast) and Pioneer-Burdekin (proposed to be constructed near Mackay).

An assessment and early works are scheduled at Borumba in the 2023 calendar year. The Queensland government has stated that it would like the Borumba project operational in 2030, though recent delays to Snowy 2.0 have made some wary about this prospect. Sensibly, the government has flagged that some coal-fired generation will need to remain in the grid until Borumba is commissioned.

Pioneer-Burdekin is listed as ideally operational in 2032. The Queensland Supergrid Infrastructure Blueprint suggests that Pioneer-Burdekin will be commissioned in two 2,500MW stages, with the second opening in 2035. The blueprint also highlights a significant amount of wind and solar generation in close proximity to Pioneer-Burdekin.

The plan also included a $500 million investment in grid-scale community batteries. This funding will support local communities to store exported excess rooftop solar.

Separately, the government is working on a Queensland Battery Industry Strategy. A consultation paper was released earlier this year. The Government has also flagged an Energy Storage Strategy for release in 2024.

This generation has not been factored in to AEMO’s ESOO or ISP to date.

Expect delays

While this pipeline of projects shows promise, the latest ESOO does deliver some slightly sobering news around timing and in particular, the likelihood of delay.

“AEMO has observed that the initial target delivery dates provided by developers of new generation and storage investments often have not accounted for delays that could occur during the project financing, planning, development and delivery stages of projects. To ensure the accuracy of its reliability outlook, AEMO now applies delays to reflect observed development and delivery risks of new projects in the reliability forecast.”

This emphasis on the risk of delay in storage projects to backup existing and additional renewable generation suggests it is front of mind for the market operator. Recent media announcements underline the attention state governments are also giving to this risk. On 7 September, the NSW Government announced an additional $1.8 billion to support the NSW energy transition. $1 billion from this announcement was committed to establish the Energy Security Corporation. In relation to storage, the announcement says:

“The Energy Security Corporation will make investments in storage projects, addressing gaps in the current market, and improving the reliability of our electricity network as we transition to renewables.

This could include investing in community batteries and virtual power plants that will allow households and communities to pool electricity generated from rooftop solar, reducing their reliance on the grid and cutting their power bills.

Once established, the ESC will make investments in commercial projects, similar to the way the Clean Energy Finance Corporation operates.”

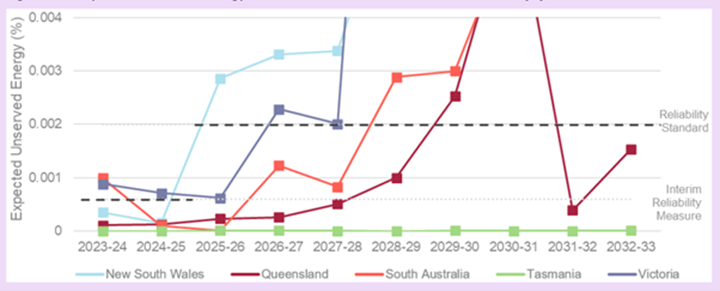

Given the reliability gaps identified in the graph below from the ESOO, governments, policymakers, and industry must work together to ensure storage projects stay on track as much as possible.

Figure 2 - Expected unserved energy, ESOO Central scenario, 2023-24 to 2032-33 (%)

Conclusion

From the volume of work being undertaken in this space, it is clear that reliability and levels of firmed capacity are front of mind for state and federal governments, departments, market operators and regulators. While there is enthusiasm for project implementation, there is perhaps a degree of clarity missing on preferences relating to technology. Different firming technologies have different reliability and flexibility characteristics, so it can be preferable to have a mix of technologies being implemented across the NEM – as determined by market design.

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Australia’s Home Battery Surge: A Question of Equity

Australia is a global leader in rooftop solar, with more than 4.3 million households and small businesses installing photovoltaic (PV) systems as of February 2026. Battery uptake has also accelerated, particularly since the introduction of the Cheaper Home Batteries Program in July 2025, which offers around a 30 per cent upfront discount for systems between 5 kWh and 100 kWh. More than 236,000 batteries had been installed by February 2026, although this likely understates the true figure due to reporting lags; the Federal Government has since indicated installations have surpassed 250,000 as of March 2026. Despite this rapid growth, an important question remains: who is actually benefiting from these subsidies?

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.