by Kieran Donoghue

SA pioneering Australia’s energy transformation

The operation of a relatively isolated, high intermittent generation grid in South Australia is revealing new challenges about how we will need to manage these systems in the future. To date seven impacts or risks have been identified from this evolving system:

- Increased spot price volatility

- Increased contract price for baseload generation

- Accelerated retirement of firm generators leading to peak capacity concerns

- Tight domestic gas markets aggravate already marginal operating conditions for firm gas generators in high intermittent operational conditions

- Increased power quality risks during periods of low demand

- Possibility that minimum demand could be met entirely by unscheduled intermittent generation (e.g. rooftop solar PV generation) by as early as 2023

- Reduced system responsiveness to sudden losses of generation.

The energy industry has been investigating some of the potential ramifications and challenges of these new operating conditions. The Australian Energy Council has commissioned three reports from independent expert analysts that look at different aspects of electricity supply in South Australia. We have also written a covering paper that brings all the analysis together and proposes areas for further investigation.

In December 2015 Deloitte reported to the Energy Supply Association of Australia on the consequences of deteriorating returns for conventional generation in increased intermittent generation systems. Deloitte warned that South Australia may have insufficient capacity to meet peak demand events, although this was prior to the reversal of planned mothballing of gas fired capacity. It also observed that market conditions in South Australia did not support investment in new flexible gas fired generation.

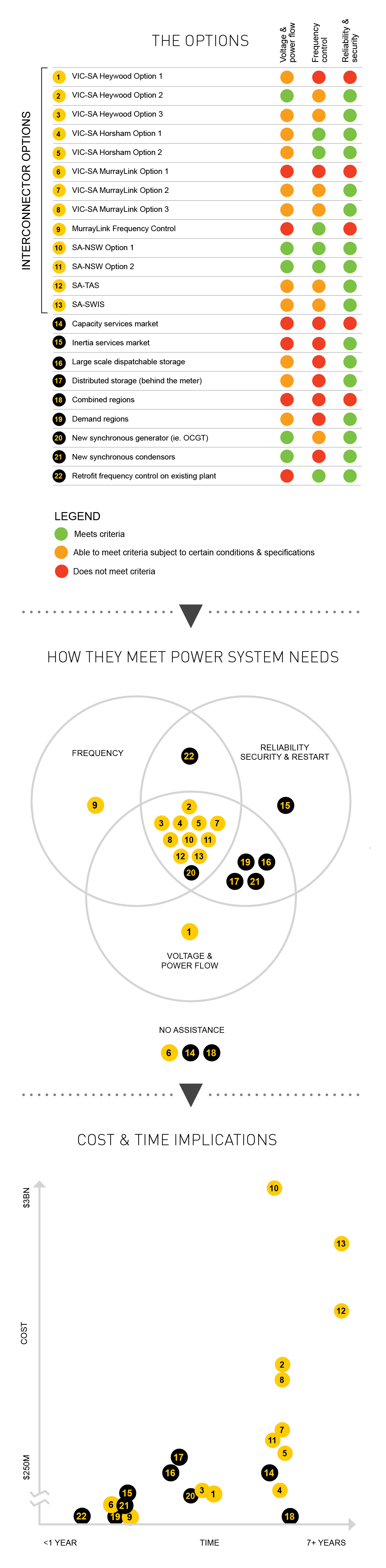

In September 2016 ACIL Allen was commissioned by the Australian Energy Council to explore a range of possible solutions to improve power quality in South Australia. They found that some proposed interconnector options could be effective in addressing a range of technical issues, but they are either very expensive or have long lead times, or both. A combination of lower cost options to procure incremental inertia, frequency and voltage control and additional dispatchable capacity could collectively provide a quicker outcome. The challenge would be to do so without undermining overall investment signals.

Figure 1: Solutions to high renewable integration in South Australia, ACIL Allen 2016 (View larger version of the diagram)

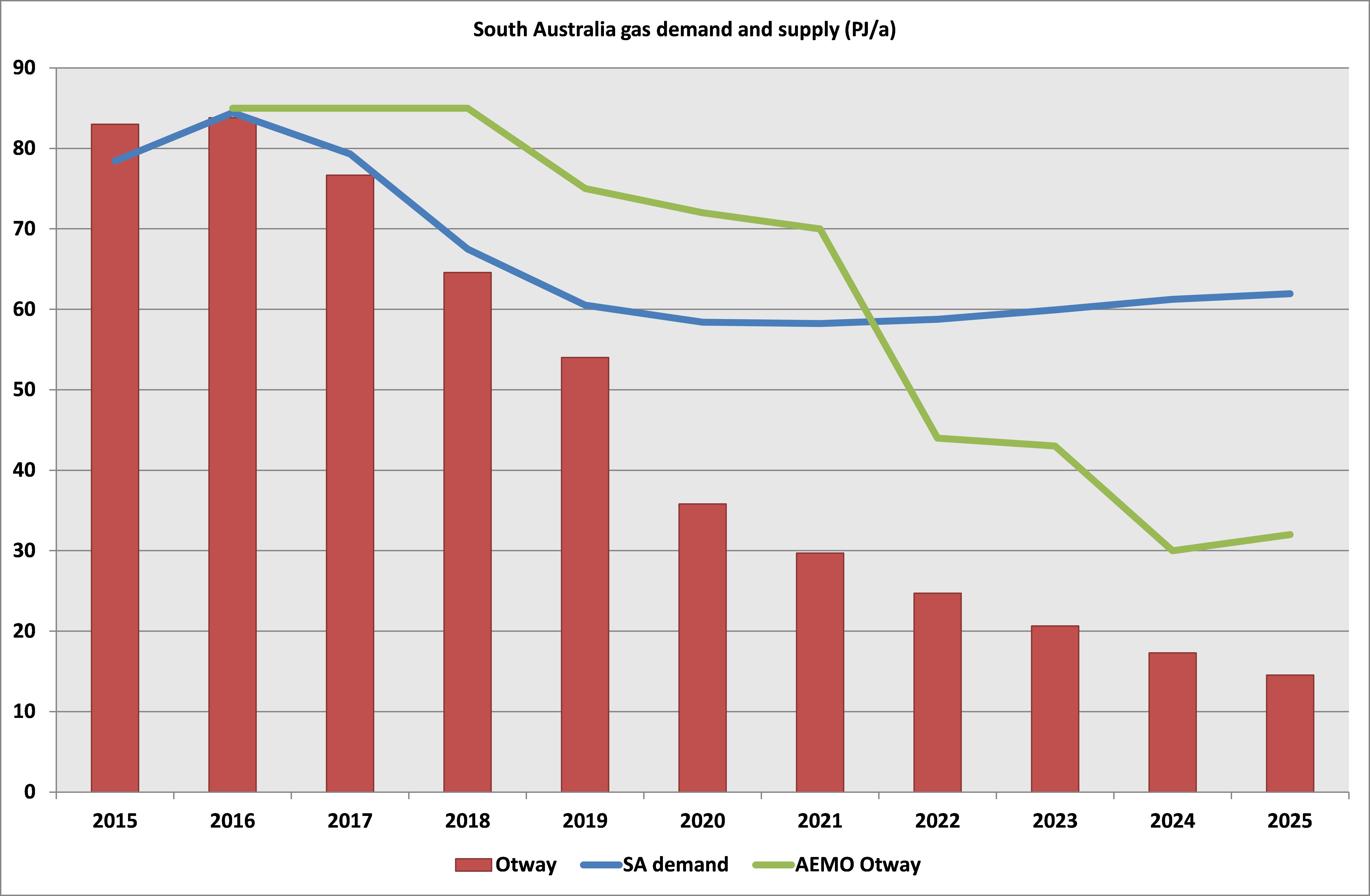

In July 2016 EnergyQuest examined the impact of natural gas supply on South Australian electricity generators, given the importance of gas as a fuel for reliable electricity supply in South Australia. They found that the South Australian gas market could be short by 2019, as the result of a growing domestic supply gap in the southern states over the next decade. This does not necessarily preclude gas being available to back-up intermittent renewables but it would imply high gas prices and difficulty in contracting more generally.

Figure 2: South Australian gas supply and demand PJ/annum

Source: AEMO, EnergyQuest: 2015 numbers are actuals

Further matters for investigation

Matters for investigation include:

- Improved design of renewable support schemes that account for their impact on the system;

- More tools for the market operator (AEMO) to procure contingent support in advance of threats to power system security

- Whether market structures need redesign to provide long-term signals for the right mix of services

- How to elicit greater demand flexibility.

Ultimately, these potential enhancements to the energy market and regulatory settings will still need to be underpinned by an enduring (i.e, bipartisan), stable and integrated climate and energy policy framework.

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Community Power Network Trial: Potential risks and market impact

Australia leads the world in rooftop solar, yet renters, apartment dwellers and low-income households remain excluded from many of the benefits. Ausgrid’s proposed Community Power Network trial seeks to address this gap by installing and operating shared solar and batteries, with returns redistributed to local customers. While the model could broaden access, it also challenges the long-standing separation between monopoly networks and contestable markets, raising questions about precedent, competitive neutrality, cross-subsidies, and the potential for market distortion. We take a look at the trial’s design, its domestic and international precedents, associated risks and considerations, and the broader implications for the energy market.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.