by Panos Priftakis

Powering up the potential for storage

Energy storage is not new. Pumped storage, for example, has been used for decades. What is new is developments with technologies like lithium-ion batteries, which are forecast to continue to fall in cost and, as a result, are expected to make energy storage increasingly accessible and viable for broader uses.

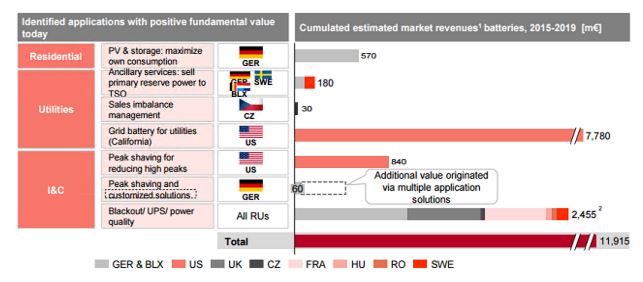

Two recent reports consider this potential, as well as possible barriers both in Australia and the UK. The reports come at a time when German utility E.ON, has indicated it is targeting potential revenues of 12 billion euros by 2020 from developing energy storage applications. The vast bulk of this is expected to come from providing grid batteries for utilities in the US and power back-up support for the industrial and commercial sector[i].

Source: E.ON presentation, Energy Storage Europe, November 30, 2015

Released in December the Australian Energy Market Commission’s (AEMC) final report “Integration of Energy Storage – Regulatory Implications” argues that it has the potential to greatly expand consumer choice, while networks and generators are also likely to derive value from storage solutions with storage offering an alternative to network augmentation and potentially helping to smooth the intermittent nature of renewable generation.

Last week UK-based consultancy Eunomia released, “Investing in UK Electricity Storage”, which points to barriers it says should be addressed to support long-term investment and wider deployment of storage in the UK.

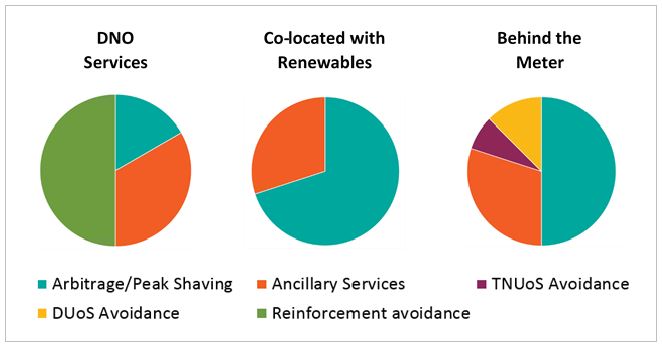

Eunomia projects that as technology and installation costs fall there will be exponential year-on-year growth to over 1.6GW in 2020 in the UK. Behind-the-meter applications are expected to be the major component, but distribution network operator services and co-location of storage with renewables are flagged as other likely drivers (see figure 1).

As greater reliance is placed on dispersed, intermittent sources of electricity that can’t simply be switched on when needed, changes in consumption patterns, higher power bills and more pressure is placed on distribution networks “there is a growing, critical need for more flexibility within our electricity network”.

Eunomia notes that intermittency is not the only challenge posed by renewables - the increasing deployment of distributed generation is causing new challenges with ever-larger areas of the distribution network reaching maximum capacity.

“Increased deployment of distributed generation on the grid not only limits the capacity for new generation but also increases the risk of voltage fluctuations, overheating and network faults.”

Demand patterns are also changing and still higher peaks can be expected if the transition to a lower carbon energy system translates into greater electrification of heat and transport.

Electricity storage can provide greater flexibility to the grid network, absorbing or releasing energy to smooth intermittent generation patterns and demand variability. “It can also help to manage the implications of potentially more variable patterns of consumption, such as frequency imbalance, and offer an alternative to conventional network reinforcement to the grid. Price differences between peak and off-peak and the wider offer and take up of time of use tariffs will make opportunities for storage as a method of reducing electricity bills increasingly attractive".

The key question for any investor will be the payback period for the capital costs and the report points to several revenue and cost saving streams available. These are set out in figure 1.

Figure 1: Indicative revenue and savings streams from battery storage

Note:

1. Revenues from Transmission Network Use of System (TNUoS) and Distribution Use of System (DUoS) avoidance are project-specific and will vary depending on energy consumption and location.

2. DNOs are only currently able to access very limited revenues from arbitrage or ancillary services, but this is likely to change in the near future

Co-location

“Many commentators seem to regard electricity storage as the panacea to the post-subsidy environment for renewables. Integrating electricity storage with solar PV or wind appears to offer the opportunity both to raise revenues and potentially overcome grid constraints. Yet the economics associated with integrating storage technologies with renewables remains challenging,” the report says.

It points to efficiency of storage batteries leading to less electricity being exported than was generated, which will require a higher peak price to offset the “lost” value of power and the cost of the installation and to provide a sufficient margin.

“In today’s UK electricity market the basic price differential between peak and off-peak power sold by a wind or solar farm alone is unlikely to provide a sufficient driver.

Ancillary services such as Firm Frequency Response, Frequency Control by Demand Management and Enhanced Frequency Response could generate revenue for co-located infrastructure, but there remain limitations and barriers to this.

Overall, it finds co-location of electricity storage with renewable generation may not live up to the “hype” and is more likely to be attractive when also being driven by a site-specific requirement.

Integration into distribution networks

The rapid deployment of renewable electricity onto the distribution networks over the last decade is now running into significant physical constraints and present major challenges for Distributed Network Organisations (DNOs). Demonstrations had shown that batteries integrated into a network could overcome some of these issues, but widespread deployment is hindered by licencing with storage currently defined as a “generation” asset in the UK, which prevents them from owning and operating storage assets larger than 10MW.

While integration of smaller storage is available restriction also limit the investment DNOs can make in, or income they can receive from, non-distribution activities to 2.5 per cent of business revenue.

The barriers mean conventional network reinforcement works generally represent a more practicable approach to network management. Without rule changes, storage within networks is only likely to be feasible if contracted to third parties, the report notes.

Behind the Meter

Storage offers the potential for business to reduce power costs through reduced peak power consumption and avoiding transmission and network charges is making battery storage attractive for intensive electricity users, such as manufacturing sites, distribution centres and data centres. They can also generate revenues through ancillary services to the National Grid.

The report says that behind-the-meter applications are the most attractive area for investment in electricity storage, but argues that until wider deployment of electricity storage takes place in the UK, developers are unlikely to be able to secure debt to finance such installations. Innovative business models, it remarks, are needed.

For behind-the-meter applications such models might involve the developer or technology provider retaining ownership and maintaining the battery while sharing revenues from electricity and ancillary services with the host organisation, which shares the benefits of lower electricity costs.

To enable long-term investment and wider deployment, section 6.0 of the report, "What will Unlock UK Investment" proposes a number of measures.

AEMC’s Final Report

In its recommendations on the implications of energy storage for the regulatory framework, the AEMC argues that battery storage can largely be accommodated within the existing regulatory framework. It does also highlight some regulatory issues that may act as barriers and makes several recommendations. These are to:

- establish a level playing field by clarifying how regulated network businesses can use storage to meet network needs;

- remove barriers to parties using storage capability to participate in the National Electricity market (NEM), for example by selling electricity into the wholesale market or providing ancillary services;

- simplify and streamline the process for the connection of storage capability to the electricity network, both behind the meter and on the grid itself; and,

- clarify that the optimisation and control of storage functionality should, except for system security and safety reasons, be determined through market-based signals.

One of the main recommendations is to clearly delineate between regulated and non-regulated parts of the energy market “to support confidence in the competitive market for storage services”.

The AEMC says there are a number of ways network businesses can access the services enabled by storage capability and concludes that networks, “should only be able to own storage ‘behind the meter’ through an effectively ring-fenced affiliate that separates this service from the provision of regulated network services”.

The AEMC intends to continue to work collaboratively with the Australian Energy Regulator, the Australian Energy Market Operator and other stakeholders to progress the recommendations.

[i]http://analysis.energystorageupdate.com/eon-eyes-eu12b-sales-battery-projects?utm_campaign=ESU%2022JAN16%20Newsletter.htm&utm_medium=email&utm_source=Eloqua

Related Analysis

Certificate schemes – good for governments, but what about customers?

Retailer certificate schemes have been growing in popularity in recent years as a policy mechanism to help deliver the energy transition. The report puts forward some recommendations on how to improve the efficiency of these schemes. It also includes a deeper dive into the Victorian Energy Upgrades program and South Australian Retailer Energy Productivity Scheme.

The return of Trump: What does it mean for Australia’s 2035 target?

Donald Trump’s decisive election win has given him a mandate to enact sweeping policy changes, including in the energy sector, potentially altering the US’s energy landscape. His proposals, which include halting offshore wind projects, withdrawing the US from the Paris Climate Agreement and dismantling the Inflation Reduction Act (IRA), could have a knock-on effect across the globe, as countries try to navigate a path towards net zero. So, what are his policies, and what do they mean for Australia’s own emission reduction targets? We take a look.

International Energy Summit: The State of the Global Energy Transition

Australian Energy Council CEO Louisa Kinnear and the Energy Networks Australia CEO and Chair, Dom van den Berg and John Cleland recently attended the International Electricity Summit. Held every 18 months, the Summit brings together leaders from across the globe to share updates on energy markets around the world and the opportunities and challenges being faced as the world collectively transitions to net zero. We take a look at what was discussed.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.