by Peter Brook

High prices cured high prices

Introduction

On 17 November 2022 the Australian Energy Council (AEC) published an EnergyInsider which identified how energy markets were beginning to correct following massive price increases in coal and gas which peaked in September last year. The paper also observed the 36 per cent reduction in Victorian Electricity Flat Calendar 2023 futures from their October 2022 peak Despite the beginnings of a correction starting to show, there was public commentary that government should intervene in these markets. In his opening statement to Senate Estimates on 8 November, the Treasury Secretary, Stephen Kennedy, also suggested,

“…in the current circumstances….interventions that address the higher domestic thermal coal and gas prices are likely to be optimal”.

The AEC EnergyInsider concluded with what subsequently turned out to be prescient advice,

“It would appear from the very recent direction of movement of international and local commodities that the “current circumstances” being referred to by Dr Kennedy may be already, or very soon, behind us. If so, it could be a great relief for all parties in averting his call for a very problematic intervention. Certainly, the government should not take any irreversible decisions whilst markets are moving favourably.”

This paper continues the analysis by looking at the latest market prices, both internationally and locally. Based on our analysis of publicly available data, the downward trend in prices has continued across gas, coal and electricity markets. In summary, the power of markets has been exhibited despite the globe emerging from a one in a hundred-year pandemic, the first major land war in Europe since World War Two and Europe having had to find new energy sources following the cessation of gas purchases from Russia.

Thermal Coal and Gas Markets

In mid-November 2022 thermal coal prices were $344 USD/t, which represented a significant decline from the peak of $458USD/t in early September. Prices then rallied and increased to $400 USD/t by the end of November before a rapidly accelerating decline commenced in early January. The price is now $220 USD/t or $316 AUD/t. Apart from the factors mentioned above, the thermal coal prices which spiked prior to Russia’s invasion of Ukraine were also influenced by Indonesia’s December 2021 announcement that it would ban coal exports in January 2022. This saw a sharp fall in its exports before the world’s biggest thermal coal exporter recommenced exports. Since the end of the ban it has been exporting at record levels.

In May 2022, coal prices were $450 AUD/t and futures were above $500 AUD/t, in our paper Inflation, interest rates, commodity prices and electricity prices we estimated fuel costs for a generator to be AUD$127/MWh based on 0.4 tonnes of black coal being used to produce 1MWh of electricity and a 70 per cent export exposure. Based on the current price of $316 AUD/t the fuel cost estimate is now $88/MWh.

Figure 1: Thermal coal futures in USD/t and AUD/t

Source: https://au.investing.com/commodities/newcastle-coal-futures-historical-data

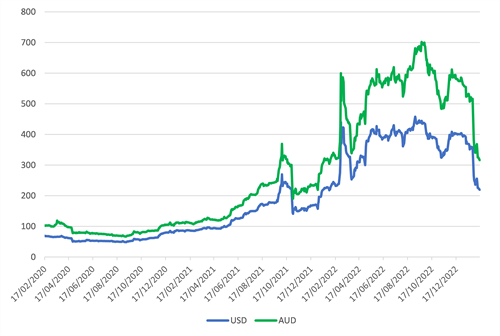

In the lead up to the northern winter, gas prices in Europe and Japan saw an enormous spike in September 2022 to $135 AUD/GJ and $95 AUD/GJ respectively. Japanese prices did not reach the same heights as Europe. A key reason was that European countries commenced programs to switch to LNG supplies to replace piped Russian gas and purchased every available cargo. In contrast Asian countries were able to switch between LNG and other fuel sources more easily.

At the time the previous paper was published (mid-November) European and Japanese gas markets had eased to $48AUD/GJ and $37AUD/GJ. From this point until mid-December they recommenced trending up and peaked at $65 AUD/GJ in Europe, as did Japanese prices which peaked at $AUD 52/GJ. From this point, they have steadily decreased and appear to have stabilised. Now, both European and Japanese prices are currently around $25 AUD/GJ.

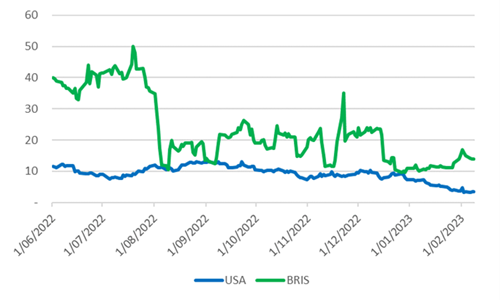

In contrast Australian gas prices spiked in June to August due to other factors. With respect to Brisbane gas prices, in mid-November they were $12 AUD/GJ. Subsequently they rose sharply to peak at $AUD35/GJ then stabilised around $22 AUD/GJ and finally fell further to around $15 AUD/GJ.

Figure 2: Gas prices in $AUD/GJ (Daily)

Sources: FX rates – RBA

https://au.investing.com/commodities/lng-japan-korea-marker-platts-futures-historical-data

https://www.investing.com/commodities/dutch-ttf-gas-c1-futures-historical-data

European gas demand (excluding storage filling) is estimated to have fallen by 12 per cent in 2022 – helped by a mild winter and government measures to reduce gas demand. Furthermore, the EU is now targeting a further reduction of 15 per cent in gas demand between August 2022 and March 2023.

Figure 3 illustrates the impressive reductions in gas consumption across European countries.

Figure 3: European sectoral demand reductions 2022 compared to average 2019-21

Source: https://www.bruegel.org/dataset/european-natural-gas-demand-tracker

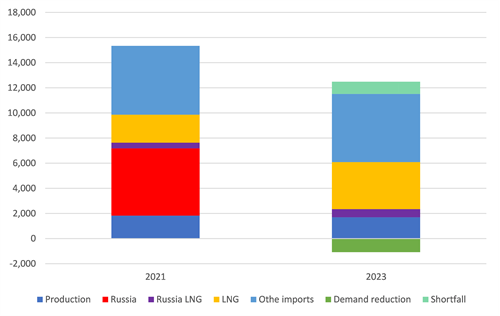

According to the International Energy Agency (IEA) the 2023 outlook for Europe is challenging but it believes it can recover from the industrial demand destruction that occurred in 2022 through measures that are currently underway such as renewables, nuclear, hydro, fuel switching etc. and expanding upon these in 2023. Figure 4 illustrates the how the cessation of Russian pipeline gas changes the composition of gas supply for Europe.

Figure 4: European gas consumption and supply sources 2021 actual and 2023 forecast (PJs)

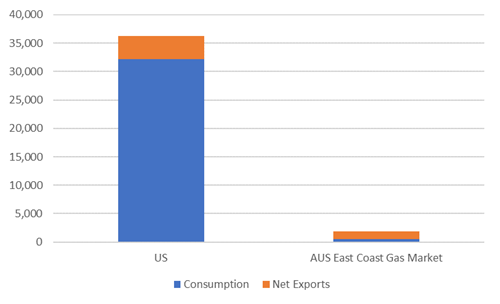

The US was previously the world’s third largest LNG exporter and was expected to become the largest in 2023. By 2025 the US LNG export capacity is expected to increase by over 50 per cent to be 6,000 PJ/year. The US has low domestic gas prices however it is a very different market to Australia’s. The US gas market has the following characteristics:

- it is connected by pipelines to Canada and Mexico, both of which are major producers of oil and gas;

- net exports represent 11 per cent of production, whereas in Australia’s east coast gas market they account for nearly 70 per cent of production;

- it has successfully exploited its vast shale oil and gas resources at relatively low cost; and

- it is continually bringing new fields online.

Figure 5 illustrates how the Australian East Coast Gast Market (ECGM) is dwarfed by the US gas market.

Figure 5: US and Australian East Coast Gas Market import consumption breakdown (PJ)

Source: AER and US Energy Information Agency

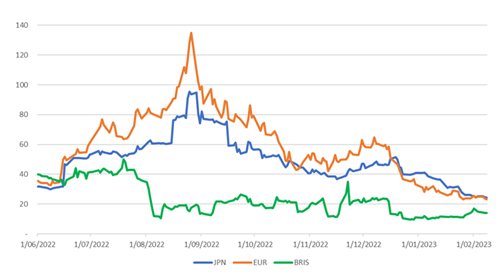

Figure 6 illustrates how US and Brisbane’s gas prices compare. Interestingly, the two have reached parity on a number of occasions. Nevertheless, since the beginning of 2023 US gas prices have decreased significantly and this has created a noticeable spread between the two gas prices.

Figure 6: US and Brisbane gas prices in $AUD/GJ (Daily)

Sources: https://au.investing.com/commodities/natural-gas-historical-data

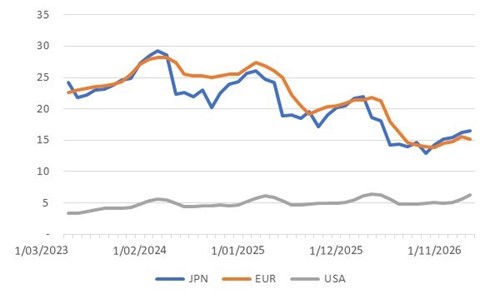

Figure 7 displays gas futures prices out to 2026. Both Europe and Japan exhibit a continuing downward trend to the point where they are around $15 AUD/GJ by the end of 2025. In contrast US prices are relatively flat at around $5 AUD/GJ.

Figure 7: Gas price futures $AUD/GJ (Monthly contracts)

Source: www.cmegroup.com

Australian Electricity Markets

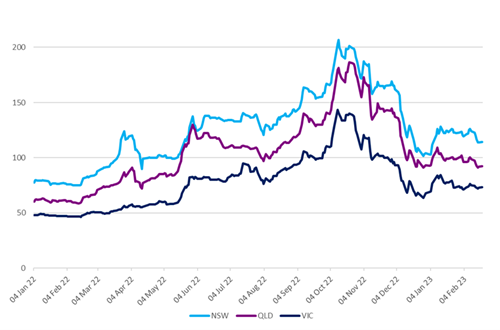

At the time of the earlier paper in mid-November NSW, Queensland and Victorian futures prices had dropped between 19-29 per cent from their mid-October highs. Following the 8 December announcement of the $125/t coal price cap the market fell sharply until the end of December where prices turned upwards and recovered some of that fall. Prices are currently sitting at around half their October peaks.

Figure 8: Electricity Flat Calendar 2024 Futures

Source: NEMFutures

Government intervention

On 8 December 2022 the government announced price caps on gas and coal. The $12/GJ gas price cap came into force on 23 December for gas and $125/t coal price cap implementation is occurring progressively. The gas intervention caused the wholesale contract gas market to stall as suppliers attempted to fully understand the new requirements and the implications for them. This in turn created challenges for industrial customers attempting to enter new retail contracts. The gas price cap applies to producers’ well-head offers and does not apply to gas delivered to the DWGM or STTMs. Prices in these markets are currently trading at $13-$16/GJ.

Beyond 12 months the government is seeking a compulsory Gas Code of Conduct which will require suppliers to sell gas at a “reasonable price”. How this “reasonable price” is to be determined is unknown. Gas suppliers have been reported as describing the cap as “interventionist”, and that:

- Australia’s previous record as an investment destination with low sovereign risk has been damaged;

- The risk of investing in gas exploration and development has increased; and

- Uncertainty surrounds the market and gas field developers have put some investment plans on hold.

While these negative consequences are to be expected with any price cap, it is much harder to establish whether the government interventions have provided any actual differences to what prices would have been had existing downward trends been allowed to continue. Especially when one considers the massive price declines in global gas and coal markets. Simple laws of economics suggest high prices in a competitive market will encourage more supply and dampen demand.

In essence the cap may have unnecessarily impaired additional domestic gas supply side responses to in the East Coast Gas Market. For ECGM gas prices to ultimately stabilise closer to those in the US, Australian producers will need to regain the confidence to develop more gas supply.

In conclusion it is worth reflecting on recent comments made by the chairman of Orica (a large gas consumer) published in the Australian financial Review on 16 February 2023.

“We’ve been here before – I remember the 1970s pretty well, [US president] Richard Nixon with his price controls, it didn’t work then. We had Gough [Whitlam] and Malcolm Fraser, it didn’t work too well there either.

So I am not sure that price controls by government, which by definition are picking winners, work in the long run.”

Related Analysis

Integrated System Plan – What Should We Expect?

The release of an expert study of last year’s autumn wind drought in Australia by consultancy Global Power Energy[i] this week raised some questions about the approach used by the Australian Energy Market Operator’s in its 2024 Integrated System Plan (ISP). The ISP has been subject to debate before. For example, there has previously been criticism that some of the ISP’s modelling assumes what amounts to “perfect foresight” of wind and solar output and demand[ii], rather than a series of inputs and assumptions. The ISP is produced every two years and with the draft of the next ISP (2026) due for release soon, it is useful to consider what it is and what it is not, along with what the ISP seeks to do.

Winter Bills: Is it cheaper to heat your house with gas or electricity?

As gas and electricity prices continue to fluctuate across Australia’s east coast, households and businesses are facing rising winter energy costs and growing uncertainty. Seasonal demand, household gas consumption, and the efficiency of electric heating systems, particularly when paired with rooftop solar, are playing an increasingly important role in shaping energy bills. Drawing on data from the Australian Energy Council’s Solar Report Q2 2025, this article explores how these factors affect costs and highlights potential savings for households of different sizes.

The energy transition and power bills: Why aren’t they cheaper?

With energy prices increasing for households and businesses there is the question: why aren’t we seeing lower bills given the promise of cheaper energy with increasing amounts of renewables in the grid. A recent working paper published by Griffith University’s Centre for Applied Energy Economics & Policy Research has tested the proposition of whether a renewables grid is cheaper than a counterfactual grid that has only coal and gas as new entrants. It provides good insights into the dynamics that have been at play.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.