by Carl Kitchen

High priced events: A snapshot

After low first quarter prices in the National Electricity Market (NEM), concerns about price spikes have taken centre stage more recently with price volatility due to factors like supply tightness with operational issues at dispatchable plant in Queensland and Victoria.

There have also been high gas prices more recently with reports of average Victorian gas prices reaching 10-year highs. That has been brought on by a series of events - cold weather has played a part along with the operational issues at Callide and Yallourn and gas being required to help fill the generation gap. On the supply front, production has been down from the Longord plant in Victoria putting pressure on other supply sources, such as the Iona gas storage facility in the state’s west[i].

In May there were high priced events which led to familiar questions about what is behind the changes. One small retailer Enova even approached the Australian Competition and Consumer Commission (ACCC) asking it to investigate the price spikes.

The Australian Energy Regulator (AER) is already required to look at high priced events and report on the factors that contribute to prices going above $5000/MWh (the market cap price was $15,000/MWh until 30 June this year and is now $15,100[ii]). The AER’s detailed reports provide insight into the workings of the market, and the many and varied factors that can impact prices. Below we take a look at three recent events – 17,18 and 21 May - and the AER’s recently released assessments of what was behind them.

17-18 May

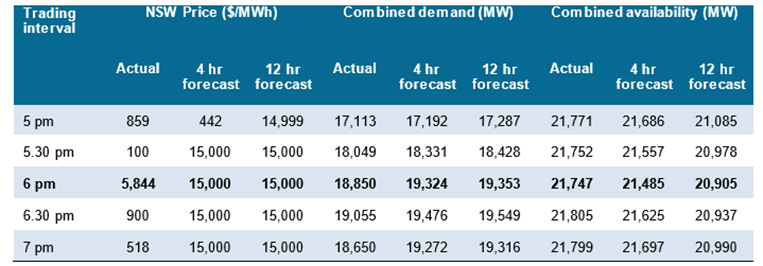

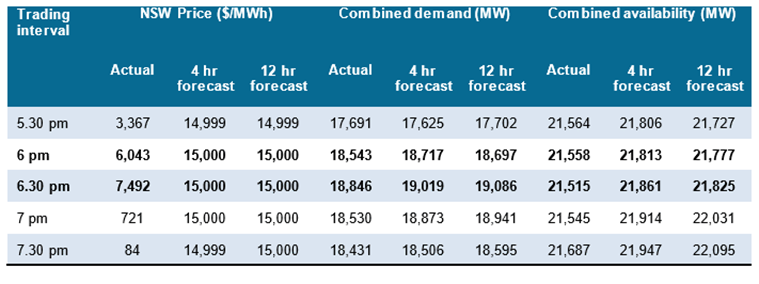

On 17 May the spot price in New South Wales (NSW), Victoria and South Australia (SA) was $5,844 for the 6pm trading interval. The following day the spot price in the three states was $6,043MW/h and $7,492/MWh for the 6pm and 6:30pm trading intervals respectively. Prices had actually been forecast to be $15,000/MWh for all the high priced intervals but were below $7500/MWh.

The tables below show the forecast and actual prices for 17 and 18 May.

Table 1: 17 May

Source: AER

Table 2: 18 May

Source: AER

On 21 May the spot price in NSW was above $5000/MWh for the 5pm and 5:30pm trading intervals. Prices were actually forecast to be higher from midday on the day.

For the 17-18 May events key factors were:

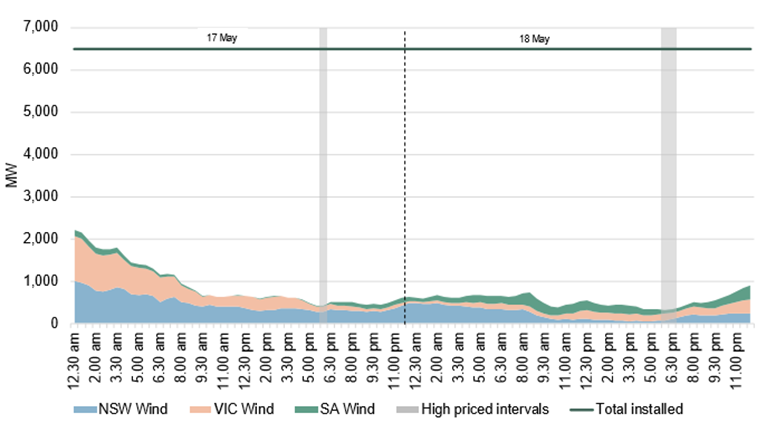

- Very low wind generation with only 320MW-430MW generated out of an installed capacity of 6510MW. The capacity factor for the wind farms was between 5 and 7 per cent at the times of high prices. Figure 1 shows the installed wind capacity and actual generation.

Figure 1: Installed wind and actual output 17, 18 May

Source: AER

- There was around 4000MW of baseload generation unavailable with two-thirds of it going through planned and expected maintenance – planned during the normally lower demand periods (spring and autumn). The other third of unavailable capacity was unavailable due to plant issues, including a unit trip at Liddell power station, tube leak at a Yallourn unit.

- Solar generation was not available in NSW and Victoria, which reduced supply and saw demand increase as solar households drew from the grid supply.

- There was high demand for the evening peak because of colder conditions.

- Upgrades on the Queensland-NSW interconnector (QNI) meant the flow south was reduced by around 300MW based on its nominal limit of more than 1000MW

The AER notes that rebidding into higher price bands was not a factor.

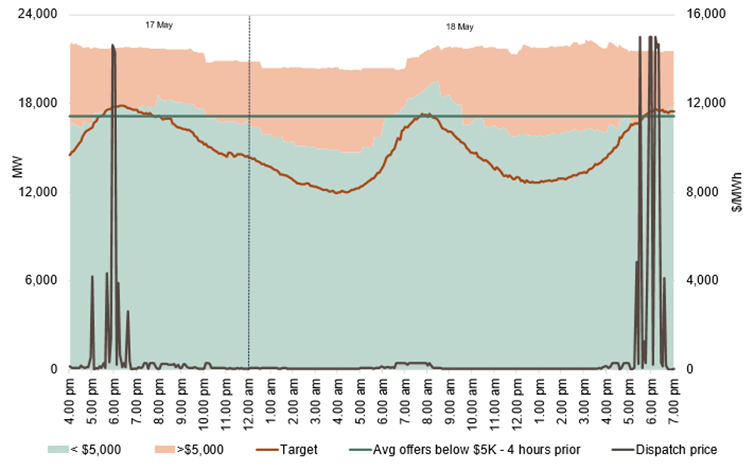

The graph below shows the combined offers above and below $5000/MWh from 4pm on 17 May until 7pm on 18 May for the three regions. For most of this time capacity priced above $5000/MWh was not needed while during the high priced periods only 17MW and 250MW of capacity priced higher was needed. The amount of capacity offered below $5000/MWh was more than the average forecast, so participants had rebid below the $5000/MWh price.

Figure 2: Spread of offers NSW, Vic, SA 17 and 18 May

Source: AER

For the 21 May high spot prices the AER found the main drivers were similar to those for the earlier days with reduced supply and higher demand.

Specifically key factors were:

- Almost 2800MW of baseload capacity was not available due to a combination of planned maintenance (this accounted for the bulk of the capacity at about 1800MW) and the report notes there was limited capacity from Liddell power station’s Unit 3 which had been offline since 16 May due to an unplanned outage. The unit experienced technical difficulties as it was being returned to service from that outage which meant it could not ramp up to full output as quickly as expected.

- Little renewable generation available – solar was dropping off given the time of day and wind output was only 208MW-237MW for the two trading periods. This was less than 12 per cent of the almost 2000MW of installed capacity in the state.

- There was limited supply available from Victoria or Queensland. Line outages around Canberra prevented generation out of Victoria and southern NSW being sent to the main load centres. The Capital to Kangaroo Valley 330kV line had planned outages that began on 17 May and there was a planned outage of the 330kV line between Lower and Upper Tumut. This area has a significant amount of generation and due to these outages the main transmission route to get to Sydney load centres was through the Yass-Marulan 330kV line and to avoid outloading this line constraints were invoked by the market operator. It limited the availability of low-priced capacity from southern NSW and imports from Victoria.

- The QNI interconnector upgrades meant flows from Queensland were 370MW less than the nominal limit of 1000MW (630MW).

- Demand during the evening peak was again high as a result of colder weather.

Again, rebidding did not contribute to prices over $5000/MWh. Up to 86 per cent of capacity was offered under that price and as little as 3MW of capacity over $5000/MWh was needed to meet demand.

The NEM has been described as a giant machine which operates from SAto Queensland and also incorporates Tasmania via the Basslink interconnector. Within the NEM electricity is generated and moved within and between regions and states, via interconnectors that link the grids in the five eastern seaboard states and the ACT. It is one of the world’s largest interconnected power systems.

It operates very efficiently, but as with any complex system (and as the latest reviews of recent high price events illustrate) variations will be reflected in fluctuations in the wholesale market price, which signals swings in the supply-demand balance at any point in time. If anything, we can expect the complexity of this interconnected system to increase as the grid transitions to lower emissions.

[i] Industry in shock as Vic gas prices hit record levels, Australian Financial Review, 10 July 2021

[ii] AEMC publishes the schedule of reliability settings for 2021-22, 25 February 2021

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.