by Carl Kitchen

GenCost verdict: Onshore wind and solar remain lowest cost generation

The latest iteration of the CSIRO’s GenCost report released last week has again highlighted that solar and onshore wind remain the lowest cost new build generation available. This remains the case even when integration costs (storage and new transmission) are factored into the overall cost modelling.

The report also quantifies the cost of global supply chain constraints which have impacted the raw material costs for manufacturing, as well as the transport costs involved in getting new generation installed. Those constraints have led to an estimated average 20 per cent increase in technology costs compared to a year ago. The capital cost of building all new generation has jumped. While the average estimated increase in technology costs is 20 per cent it ranges from 9 per cent for solar PV and up to 35 per cent for wind generation (see figure 1). There is an expectation that the current inflationary cycle impacting technologies has peaked in 2022-23, but also that it will take until 2027 to return to normal under current global climate policy commitments. It could take to 2030 if more ambitious commitments that encourage faster technology deployment are undertaken.

Figure 1: Increase in current costs of technologies

Source: CSIRO GenCost 2022-23

The differences in technology costs are based on the level of their exposure to various cost inputs.

The CSIRO assessment also considers storage costs and includes capital cost estimates for longer duration adiabatic compressed air storage (A-CAES) at 12 hours and a new estimate for concentrating solar thermal (CST) at 15 hours – both are amongst the highest cost storage technologies, along with 48-hour duration pumped hydro.

As with generation technologies, storage capital costs have increased and this is estimated to have resulted in a 13 per cent increase for one hour duration batteries and by as much as 28 per cent for 8-hour duration batteries. Pumped hydro costs are up an estimated 17 per cent.

The report considers small nuclear reactors (SMRs), but only projects the technology’s costs from 2030 based on the expectation that there could not be any deployment in Australia before that date, as well as floating offshore wind technology costs. Offshore wind is relevant given current proposals for projects and the declaration of offshore wind zones in Victoria and New South Wales. Nuclear (SMR) is at the higher end of the cost curves based on current policy settings and remains a high-cost technology even under the Global Net Zero Emissions (NZE) by 2050 scenario[i]. In contrast offshore floating wind turbines are expected to come down the cost curve based on this more ambitious scenario as more turbines are installed globally. Nuclear will also require SMRS to be deployed globally and in large enough capacity to achieve economies of scale and lower capital costs.

Integration costs for renewables

Unsurprisingly the report finds that additional costs increase as renewable generation’s share grow with expenditure required on storage and transmission, particularly to strengthen existing links in the National Electricity Market (NEM). It also notes that as transmission costs assessed have been updated, saying “…they have tended to increase in cost”. Aside from the modelling this has been a notable feature of new transmission projects, such as EnergyConnect and Transgrid’s HumeLink, with the actual costs increasing beyond earlier estimates. A NSW Parliamentary inquiry was told the cost of HumeLink had increased by about 30 per cent in real terms and would now be $5 billion. EnergyConnect was originally expected to cost $1.5 billion and increased to $2.3 billion, a 50 per cent increase. Given these factors the CSIRO comments that as transmission costs are updated and have increased this has “likely led to a reduced reliance on transmission to balance supply in the modelling”.

REZ expansion costs appear to be required at similar levels for each additional 10 per cent increase in VRE share and in each state, other transmission costs (those to strengthen existing links rather than REZs) have a rising trend in the NEM with the highest expenditure in New South Wales and Victoria based on their central role in the NEM and access to pumped hydro. The cost of REZ transmission expansions adds $6-$8/MWh as renewable share increases from 60 to 90 per cent; other transmission adds $5-$6/MWh with costs accelerating as renewables increase. Storage adds $9-$14/MWh. Based on previous estimates of transmission costs and actual outcomes, these are likely to increase beyond these figures.

The CSIRO has calculated that in 2030 the NEM will need to have 0.26kW to 0.39kW of storage capacity for each kW of variable renewable generation installed

Overall integration to support renewables are estimated to be $25-34/MWh. Figure 3 shows the changes in the costs of various technologies to support renewables as their share of capacity increases in the NEM, while figure 3 shows the LCOE for various technologies and renewables, including their integration costs.

Figure 2: Levelised costs of achieving 60%, 70%, 80% and 90% annual renewable energy share in NEM

Source: CSIRO GenCost 2022-23

Figure 3: LCOE of technologies 2030

Source: CSIRO GenCost 2022-23

Below we show the CSIRO’s cost assessment for major generation and energy storage technologies across various scenarios and compared to last year’s estimates.

Black coal supercritical

Figure 4: Black coal plant projected capital costs

Source: CSIRO GenCost 2022-23

Coal with CCS

Cost reductions are assumed to occur because of deployment of carbon capture and storage technology in other industries rather than in the energy sector and there is considered to be only a negligible amount of generation from this source over the CSIRO’s projection period.

Figure 5: Coal plant with CCS projected capital costs

Source: CSIRO GenCost 2022-23

Gas with CCS

The report notes that there is a relatively small pipeline of projects planned globally using this technology (30 planned which are yet to make a financial investment decision, two under construction and one completed) and advance projects are for smaller volumes and/or low capture rates. Given this the modelling assumes the earliest date for commercial, high capture projects is 2035, so meaningful cost reductions don’t occur until after that date.

Figure 6: Gas plant with CCS projected capital costs

Source: CSIRO GenCost 2022-23

Combined Cycle Gas

Figure 7: CCGT projected capital costs

Source: CSIRO GenCost 2022-23

Open Cycle Gas

Figure 8: OCGT projected capital costs

Source: CSIRO GenCost 2022-23

Nuclear SMR

Global commercial deployment of SMRs is limited to a small number of projects. Any major shift in forecast costs would depend on more aggressive emission reduction policies and greater deployment of plants.

Figure 9: Nuclear SMR projected capital costs

Source: CSIRO GenCost 2022-23

Solar Themal

Solar thermal is considered to be integrated with solar and wind, with its key role being in evening and overnight generation.

Figure 10: Solar thermal projected capital costs

Source: CSIRO GenCost 2022-23

Large-scale solar

Figure 11: Large-scale solar projected capital costs

Source: CSIRO GenCost 2022-23

Rooftop Solar

Figure 12: Rooftop Solar Projected Capital Costs

Source: CSIRO GenCost 2022-23

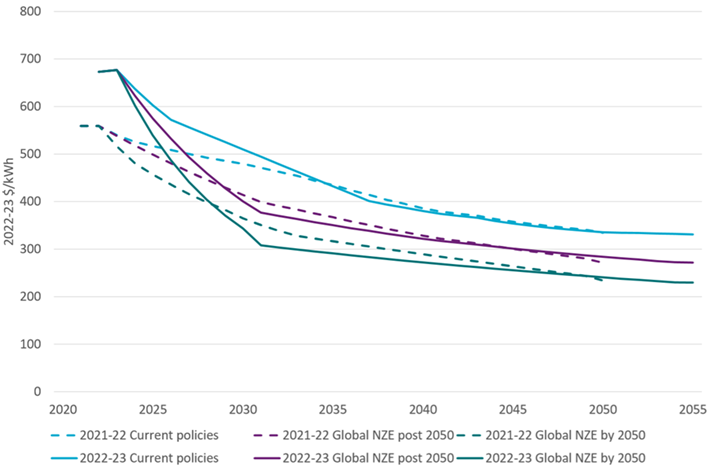

Onshore Wind

Figure 13: Onshore Wind Projected Capital Costs

Source: CSIRO GenCost 2022-23

Offshore wind (fixed and floating)

Figure 14: Projected costs for offshore wind - fixed and floating

Source: CSIRO GenCost 2022-23

Pumped hydro

Figure 15: PHES projected costs

Source: CSIRO GenCost 2022-23

Battery Storage

Figure 16: Battery storage projected costs

Source: CSIRO GenCost 2022-23

[i] Global NZE by 2050 is based on the International Energy Agency’s 2022 World Energy Outlook and under this scenario “there is strong climate policy consistent with maintaining temperature increases of 1.5 degrees of warming and achieving net zero emissions by 2050 worldwide. The achievement of these abatement outcomes is supported by the strongest technology learning rates and the least constrained (physically and socially) access to variable renewable energy resources”.

Related Analysis

Australia’s Home Battery Surge: A Question of Equity

Australia is a global leader in rooftop solar, with more than 4.3 million households and small businesses installing photovoltaic (PV) systems as of February 2026. Battery uptake has also accelerated, particularly since the introduction of the Cheaper Home Batteries Program in July 2025, which offers around a 30 per cent upfront discount for systems between 5 kWh and 100 kWh. More than 236,000 batteries had been installed by February 2026, although this likely understates the true figure due to reporting lags; the Federal Government has since indicated installations have surpassed 250,000 as of March 2026. Despite this rapid growth, an important question remains: who is actually benefiting from these subsidies?

Integrated System Plan – What Should We Expect?

The release of an expert study of last year’s autumn wind drought in Australia by consultancy Global Power Energy[i] this week raised some questions about the approach used by the Australian Energy Market Operator’s in its 2024 Integrated System Plan (ISP). The ISP has been subject to debate before. For example, there has previously been criticism that some of the ISP’s modelling assumes what amounts to “perfect foresight” of wind and solar output and demand[ii], rather than a series of inputs and assumptions. The ISP is produced every two years and with the draft of the next ISP (2026) due for release soon, it is useful to consider what it is and what it is not, along with what the ISP seeks to do.

Getting it right: How to make the “Solar Sharer” work for everyone

On paper, the government’s proposed "Solar Sharer Offer" (SSO) sounds like the kind of policy win that everyone should cheer for. The pitch is delightful: Australia has too much solar power in the middle of the day; the grid is literally overflowing with sunshine: let’s give households free energy during 11am and 2pm. But as the economist Milton Friedman famously warned, "There is no such thing as a free lunch." Here is a no-nonsense guide to making the SSO work.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.