by Australian Energy Council

Electrification & Heat: Discussion paper released

The Australian Energy Council today releases the latest in its series of discussion papers examining the challenges and opportunities in the decarbonisation of the economy. The AEC has proposed an interim economy-wide emission reduction target of 55% from 2005 levels by 2035 and the papers consider options for decarbonisation beyond electricity into sectors such as stationary energy and transport. These are sectors where large decarbonisation opportunities exist now through electrification.

2035 was selected as it is the midpoint to 2050 and provides an opportunity for early decarbonisation to be shared beyond the electricity industry, which is already rapidly decarbonising. Even using current technologies and electricity grid emissions intensity, electrification already has lower lifetime costs and will result in lower emissions than burning liquid or gaseous fuels. The progressive decarbonisation of the electricity sector will only further reduce emissions in these sectors.

This latest paper considers Electrification & Heat - the potential electrification of heat sources in both the residential and industrial context.

There are four main ways we use energy: for illumination, movement, changing temperature, and to power an ever-growing range of electrical devices and tools.

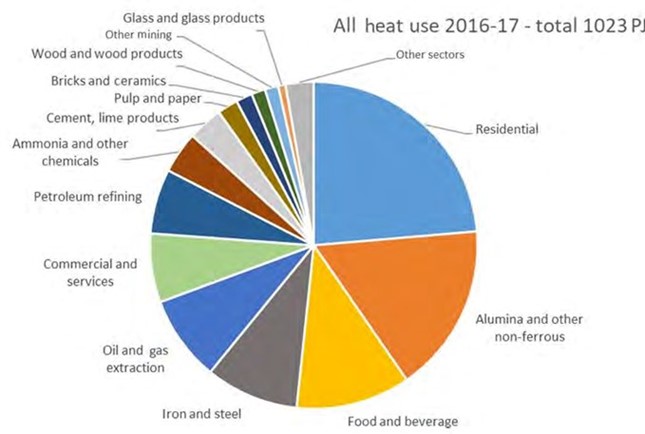

When Australia’s energy consumption is reallocated according to end-use around 1279 PJ per annum or 30 per cent of all energy is used to produce heat, compared to 20 per cent consumed as electricity. Because of thermal losses, this energy produces around 1023 PJ of actually consumed heat. Most of this heat (730 PJ) is consumed by industrial processes: metals refining, processing of food and beverages, production of ammonia, cement, pulp and paper, oil, gas and other chemicals. The remaining heat demand is from households and commercial applications.

Heat market in Australia, by sector 2016-17

Source: ARENA

There are two basic uses for heat. The first is amenity based – to heat air and water in buildings for comfort and convenience. The second is industrial – to supply heat for a range of processes from baking bread to making steel. Amenity heat is lower in temperatures required (mostly below 100 degrees) compared to industrial heat, which can range from around 100 degrees to more than a thousand degrees.

Electrification of both amenity and industrial heat is closely linked to the plant and equipment used to produce it. Electrification of residential heat requires replacement of long-life assets like water heaters, space heating systems and cooktops. These are major asset changes for households, and, in the case of cooking, can require even more expensive repair or renovation of kitchens. The same applies to retrofitting heating in commercial buildings and in industrial applications.

This means electrification of heat requires two components: the availability of the replacement energy as electricity and considered measures to support the replacement of these major capital assets. Not all industrial uses of heat are easily electrified, particularly high-temperature heat which uses combustion to achieve the very high temperatures needed to trigger chemical reactions. Decarbonisation of these processes may be more suited to replacement fuels like biomethane and hydrogen.

Electricity can be converted into heat using resistance (like an electric kettle or conventional hot water system) or at lower temperatures by using heat pumps, which extract heat from ambient air and can deliver around four to five times the useful heat from each unit of electrical energy. This means there are opportunities to exploit significant energy cost savings where gas combustion (which in contrast actually loses 10-40 per cent of heat in the combustion process) can be replaced by electrical heat pumps: residential water and air heating, and in some lower temperature industrial applications.

This means there is a strong case to move immediately towards substituting natural gas in domestic and commercial situations where:

- The dominant use of natural gas is for low intensity space and water heating. In this scenario, using heat pumps instead of gas is more economic and environmentally efficient for the customer and society.

- The residual, but much smaller, use of natural gas for cooking can readily be converted to resistance heating, thereby removing the need to retain gas connection.

In industrial high intensity heat applications, natural gas appears to not be greatly substitutable with electricity. In time, as they become more available, biomethane and hydrogen may be the appropriate decarbonisation pathways.

Further papers in the series will be released over the coming weeks and will consider:

- Zero emissions dispatchability

- Hydrogen - industry development and integration of hydrogen with electricity

- Regional transitions (where coal plants are closing)

- Implications for transmission investment

- Implications for distribution investment.

Related Analysis

Judicial review in environmental law – in the public interest or a public nuisance?

As the Federal Government pursues its productivity agenda, environmental approval processes are under scrutiny. While faster approvals could help, they will remain subject to judicial review. Traditionally, judicial review battles focused on fossil fuel projects, but in recent years it has been used to challenge and delay clean energy developments. This plot twist is complicating efforts to meet 2030 emissions targets and does not look like going away any time soon. Here, we examine the politics of judicial review, its impact on the energy transition, and options for reform.

Climate and energy: What do the next three years hold?

With Labor being returned to Government for a second term, this time with an increased majority, the next three years will represent a litmus test for how Australia is tracking to meet its signature 2030 targets of 43 per cent emissions reduction and 82 per cent renewable generation, and not to mention, the looming 2035 target. With significant obstacles laying ahead, the Government will need to hit the ground running. We take a look at some of the key projections and checkpoints throughout the next term.

Certificate schemes – good for governments, but what about customers?

Retailer certificate schemes have been growing in popularity in recent years as a policy mechanism to help deliver the energy transition. The report puts forward some recommendations on how to improve the efficiency of these schemes. It also includes a deeper dive into the Victorian Energy Upgrades program and South Australian Retailer Energy Productivity Scheme.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.