by Graham Pearson

Do generators earn adequate revenue?

Electricity markets are always evolving to address new and emerging issues. Settings change, new policies are implemented, and the market adapts to how and when consumers use energy.

The Wholesale Electricity Market (WEM) has seen its share of reforms and changes over the last few years. There have been amendments to the Access Code, the WEM Rules have been completely updated, the Economic Regulation Authority (ERA) has looked at market power mitigation measures and, more recently, the Market Advisory Committee has launched a review of the Reserve Capacity Market (RCM). In the meantime, Western Power has begun to deploy a fleet of network connected batteries and the growth of rooftop PV and behind-the-meter storage goes unabated.

Most new policies are considered in isolation but, together, these reforms and settings can have a substantial impact on generators and their revenues. To better understand the implications of these changes on generators, the Australian Energy Council (AEC) engaged Marsden Jacobs Associates (MJA). The WEM has always incorporated an explicit capacity reward mechanism alongside a payment for dispatched energy. With the Energy Security Board deeply engaged in developing such a design for the National Electricity Market (NEM), MJA’s investigation is particularly pertinent across Australia. Here we look at MJA’s key findings and consider whether generators in the WEM receive adequate revenue to support the dramatic transition underway.

The current state of play

There has been a constant stream of new policies and reforms over the last few years. These are individually consulted with market participants but when combined, the changes raise significant concerns about revenue adequacy and investment signalling for generators in the WEM. To consider this issue further, the AEC engaged MJA to provide an assessment of the:

- Current and proposed revenue streams for generators in the WEM;

- Whether they provide revenue adequacy; and

- Then make recommendations to enhance revenue adequacy and minimise investor uncertainty.

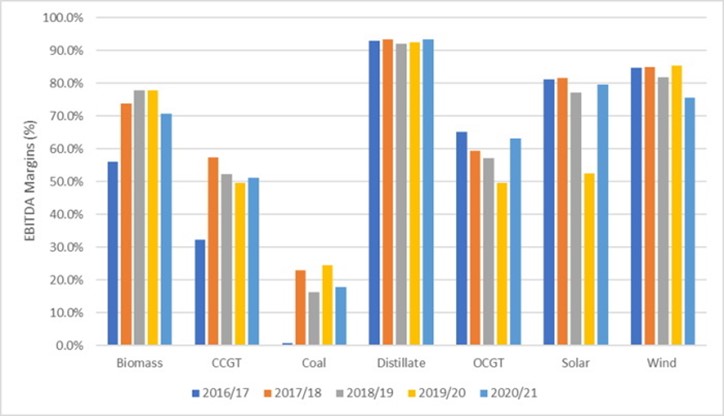

The starting point for MJA was to assess whether each generator type in the South West Interconnected System (SWIS) has received adequate revenue between 2016/17 and 2020/21. They did this by calculating the EDITDA margin. The EBITDA margin does not imply that a generator is financially viable and recovering their full capital costs, but if the plants can at least cover their operating costs and contribute to their capital costs then they are likely to remain in operation.

MJA concluded that the WEM has provided adequate revenue for most plant types in the period (see Figure 1).[1] Renewable generators had high EBITDA margins driven by their relatively low variable costs, while Open Cycle Gas Turbine (OCGT) units had declining EBITDA margins until an uptick in 2020/21. Perhaps not surprisingly, coal generators had the lowest EBIDTA margins. Coal generators have seen sales being eroded by intermittent generation and they are also especially sensitive to small reductions in revenue caused by an increased number of starts and a higher cost for starts.

Figure 1: EBITDA Generator Margins in the WEM by Financial Year (June 2021 dollars)

Source: Marsden Jacob 2022

MJA’s assessment of previous revenue adequacy paints a good picture. Based on their assumptions, all generators have received enough revenue to cover costs over the last few years and stay in business. But what does the future look like? Will there be adequate revenue for generators over the coming decade?

The energy transition

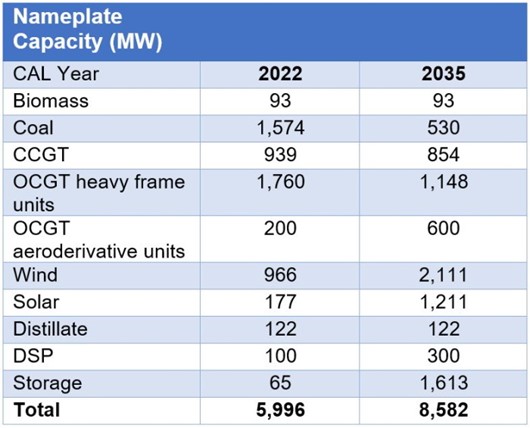

To answer these questions, we first need to consider the current generation mix and how that is expected to change over time.

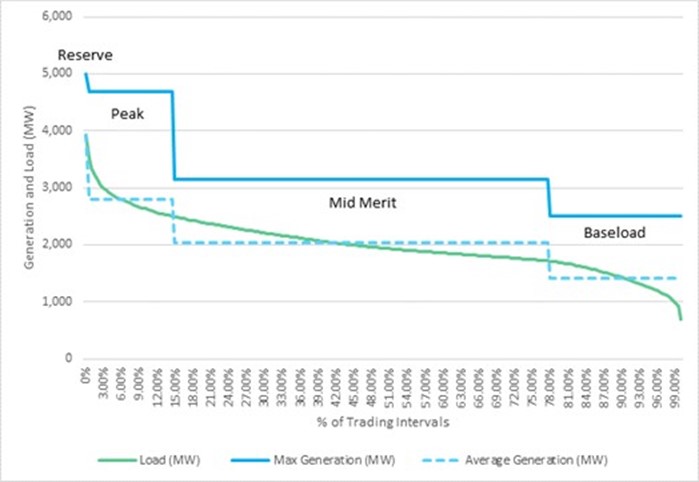

MJA assessed the suitability of the existing fleet by categorising generation into baseload, mid-merit, peaking and reserve, and then overlaying a load duration curve. Figure 2 shows that there is a large surplus of generation capacity in 2022 with Capacity Credits exceeding the Reserve Capacity Target by 9.9 per cent in the 2021/22 Capacity Year. The capacity surplus is most acute for baseload generation (i.e. coal, combined cycle gas turbines (CCGT), etc.) with capacity being 77 per cent higher than demand. Mid-merit plant capacity, which also features renewable generation, is 55 per cent above demand, while peaking plant capacity is 68 per cent higher than demand.

Figure 2: Generation Capacity by Operating Cycle and Load Duration Curve for CAL 2022

Source: Marsden Jacob 2022

The generation fleet in the WEM, with excess capacity and inflexible generation, does not appear to match current requirements. However, this could be set to change as private sector and government commitments of net zero emissions by 2050 are leading a transition towards more intermittent and dispatchable generation.

MJA compared the current generation fleet with the likely future generation fleet that is required to achieve the emission reduction targets and meet the reliability criteria while minimising wholesale costs. Large amounts of new storage capacity must be introduced to satisfy demand and maintain supply reliability, while significant investment in intermittent wind and solar generation is needed to meet emission reduction targets.

Put simply, the electricity system needs to transition quickly to achieve net zero emissions by 2050. To get there, adequate revenue must be available to keep existing generators in the market as part of the transition and incentivise investment in new firm generating sources to maintain future supply reliability.

Future revenue adequacy

MJA undertook an assessment of future revenue adequacy for all generators by comparing levelised costs with levelised revenue from the energy, capacity and Essential System Service (ESS) markets between 2022 and 2031.

A key input in determining revenue adequacy for new generation is the floating Reserve Capacity Price (RCP): the clearing price of the capacity “auction” held every year. MJA forecasts that the RCP will remain low due to current excess capacity, averaging just $75,000 per MW per annum until CAL 2027, but the RCP then jumps to $170,000 per MW per annum in 2031 as capacity reduces. In contrast, the ESS price is forecast to fall because of increased competition between gas plant and new storage entrants.

The results of MJA’s assessment are fascinating. There is debate underway in the NEM about the merits of a capacity mechanism and whether it would incentivise coal to stay in the market. .The MJA report shows that the RCM alone may not be sufficient to keep coal in the WEM with revenue well below costs. Elsewhere, forecast revenue for CCGT plants and OCGT aeroderivative units is only just sufficient to cover costs. In terms of renewable generation, wind is economic but hardly recovering excessive amounts of revenue. Solar is not economic without Large-scale Generation Certificate (LGC) revenue because rooftop PV is depressing the dispatch weighted price for energy delivered in the balancing market.

Figure 3: Levelised Revenue and LCOE for Mid Merit Plant in the WEM (June 2021 dollars)

Source: Marsden Jacob 2022

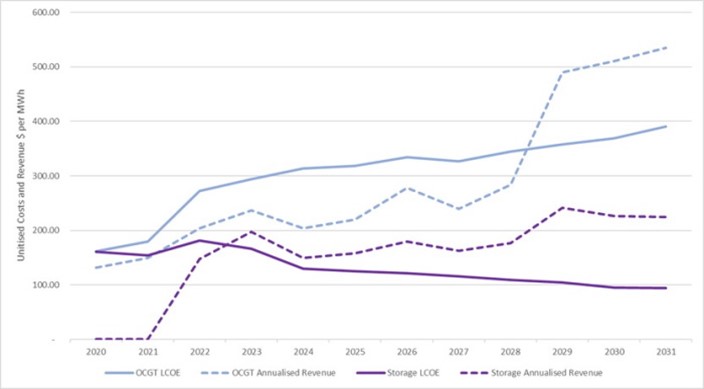

Battery storage is where things start to get really interesting. MJA’s modelling shows that 4-hour storage is marginal until around 2024/25 and then after that annual revenue starts to increase and 4-hour storage becomes economic.

Figure 4: Levelised Revenue and LCOE for Peaking Plant in the WEM (June 2021 dollars)

Source: Marsden Jacob 2022

Given that new entrant OCGT heavy frame units are not profitable, and OCGT aeroderivative units and CCGT plants are only marginally profitable, there is the potential for under-investment in these generator types if they are not able to recover costs. Equally, an investor in 4-hour battery storage would have to take a long-term view and bank on settings becoming favourable to proceed with a project now.

The main cause of the ‘missing money’ for these generators is the low RCP. Negative prices also play a role in contributing to the problem.

But here’s the twist. Battery storage is required in the future market. 4-hour storage is expected to be economic in a few years, but in the meantime the SWIS will continue to evolve and modelling by MJA indicates that battery storage requirements will begin to exceed four hours. By 2040, the period within the day at which peak demand is experienced will increase to 5 hours and, even now, peak demand can occur for up to 6 hours.

As MJA notes, the problem is that long duration battery storage will be required for reliability but:

“The ESR Obligation Duration, the Capacity Price formula and linear derating method does not provide an economic return for storage facilities exceeding 4 hours. The annualised capital cost of 4-hour storage facility is $159,000 per MW per annum, whereas the annualised capital cost for an 8-hour storage facility is $275,000 per MW per annum. If the capacity price is set at the BRCP, then 4-hour storage facilities will be economic. However, an 8-hour facility will not be economic. For example, even if the ESR Obligation Duration increases to 8 hours, the facility will only receive $159,000 per MW per annum on its nameplate capacity. Additional revenue from the Balancing Market will help to cover costs, but the increased penetration of storage in the WEM will likely reduce price spreads (i.e., price arbitrage benefits) post 2031. By this time, it is likely that the ESS market is saturated with storage facilities, which implies that storage facilities will earn no income from ESS markets.”[2]

In summary, even if the market is in balance and capacity prices increase, investment in long duration battery storage will not be incentivised by current market settings in the WEM.

How can this be fixed?

In their report, MJA considered what measures could be adopted to ensure revenue adequacy and minimise investor uncertainty. They made three key recommendations.

Firstly, MJA say that there should be long-term 15-year capacity contracts for new entrant generation and storage at gross cost of new entry (CONE).[3]

The current capacity pricing mechanism only provides annual prices two years ahead for generators. It can be as low as zero at 30 per cent excess capacity, and 50 per cent of the benchmark reserve capacity price (BRCP) at 10 per cent excess capacity (which is the current level). MJA argues that investors need to be able to secure long term capacity prices that cover a substantial portion of gross CONE, with the balance provided by the energy and ESS markets plus LGCs for renewable generation.

Market Participants seeking price certainty are now able to nominate themselves to be a Fixed Price Facility during the certification process. Fixed Price Facility prices are pegged to the RCP of the first Reserve Capacity Cycle in which they make their capacity available and after that the RCP from the first cycle is increased by the Consumer Price Index for each subsequent cycle. Fixed Prices are valid for five years.

Given the likely variability in capacity prices resulting from the new capacity price formula introduced in the 2021-22 capacity year, it is unlikely that a 5-year fixed capacity price at the current low RCP will be enough to underwrite investment in new flexible generation and storage in the WEM. MJA suggest that investors who are willing to invest in long lived generation and storage assets in the WEM should be able to lock in a price at or near the gross CONE for a minimum of 15 years or 60% of the asset life. And there is precedent for longer-term contracts, with the UK Capacity Market offering 15-year contracts and the I-SEM in Ireland providing 10-year contracts.

The second recommendation made by MJA is for a technology-based capacity price based on net CONE to encourage long duration battery storage of up to 8 hours.

If the capacity price is set at gross CONE then an 8-hour facility will not be economic, however forecasts suggest that long duration battery storage will be required . To incentivise these facilities to enter the market and to make them viable a specific long duration storage capacity price category with prices based on Net CONE could be introduced in the WEM.

The third recommendation is for regular reviews of generator profitability under current and proposed market settings to ensure that the WEM is fulfilling its market objectives.

Many market settings and parameters are set independently and there is no certainty that they will encourage the right mix of plant in the SWIS or provide revenue adequacy. MJA notes that:

“Without undertaking this modelling, Energy Policy WA and the Economic Regulation Authority are unlikely to fulfill the Wholesale Market Objective to “promote the economically efficient, safe and reliable production and supply of electricity” or “encourage competition among generators and retailers in the South West interconnected system, including by facilitating efficient entry of new competitors”.

When establishing policies, price limits and measures, policy makers and regulators should be confirming that there is sufficient revenue in aggregate from all market mechanisms to encourage flexible generation and storage to meet future demand.”[4]

Is it time for a review?

MJA has produced a comprehensive report that assesses whether there is adequate revenue for generators in the WEM. The warnings in the report are clear: for many generators, there is only just enough revenue to cover costs as the market transitions to net zero by 2050 and long duration battery storage, which will be required for reliability, is not currently incentivised to enter the market.

Reforms are always going to be a part of any electricity market. Settings evolve and the way we use and deliver energy will change. How these policies and measures come together has a substantial impact on the viability of generators in the WEM.

MJA makes some insightful recommendations and highlights the importance of considering policies, price limits and settings in combination. Maybe now is the time for a wholistic review of generator revenue under current and proposed market settings in the WEM.

There are also pre-emptory lessons for the design of any explicit capacity mechanism for the NEM. It would be disappointing if the NEM adopted something close to the current RCP design, and then discovered it similarly failed to deliver the investment signals needed to provide reliability in this critical period as the traditional generation fleet turns over.

A copy of the MJA report can be found here.

[1] The EBITDA margins exclude market costs and LGC revenue.

[2] P73 of report

[3] The CONE is annualised capital and fixed O&M costs.

[4] P72 of report

Related Analysis

From Energy to Flexibility: Rewiring Australia’s Wholesale Markets for Net Zero

Australia’s path to net zero will depend not only on new technologies, but on fundamentally reshaping the markets that underpin the energy system. As coal exits, renewables, storage and consumer energy resources will drive a far more dynamic and decentralised National Electricity Market, where flexibility becomes the critical commodity. We explore the market reforms, investment signals and system changes required to deliver a secure, affordable and reliable Energy2050 future, themes that will also sit at the centre of the Australian Energy Council Conference 2026 in Sydney on 4 June.

Is increased volatility the new norm?

This year has showcased an increased level of volatility in the National Electricity Market (NEM). To date we have seen significant fluctuations in spot prices with prices hitting both maximum price caps on several occasions and ongoing growth in periods of negative prices with generation being curtailed at times. We took a closer look at why this is happening and the impact this could have on the grid in the future.

Is there a better way to manage AEMO’s costs?

The market operator performs a vital role in managing the electricity and gas systems and markets across Australia. In WA, AEMO recovers the costs of performing its functions via fees paid by market participants, based on expenditure approved by the State’s Economic Regulation Authority. In the last few years, AEMO’s costs have sky-rocketed in WA driven in part by the amount of market reform and the challenges of budgeting projects that are not adequately defined. Here we take a look at how AEMO’s costs have escalated, proposed changes to the allowable revenue framework, and what can be done to keep a lid on costs.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.