by Ben Skinner

Customer benefits don’t necessarily benefit the customer

A perennial discussion in energy market policy is the contest between what we are ultimately trying to achieve: “customer benefits” or “market benefits”.

When making market rules, or building monopoly assets, rules require that we assess “net market” benefits, not customer benefits. This may at first appear surprising, because after all, the energy market objective is the long-term interests of consumers. But when considered thoughtfully, the net market benefits approach makes a lot of sense whilst the alternative doesn’t.

Nevertheless a number of recent government policies have been justified on customer benefit assessments alone. We look at why that is an incorrect approach.

Drawing a boundary

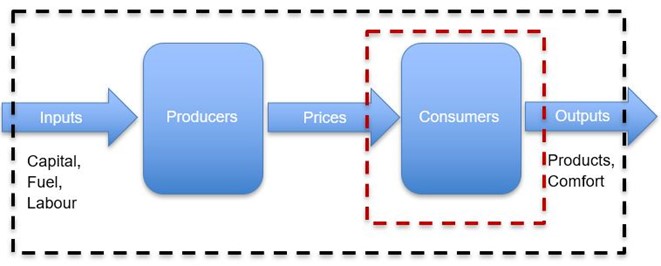

To understand the question, it helps to first think about an industry as a whole.

Figure 1: Industry boundaries

“Net market benefits” can be considered as the transactions that cross the wider black dotted rectangle (figure 1). Good policy should try to minimise the inputs and maximise the outputs: the industry’s overall productivity.

“Customer benefits” could be thought of as the transactions that cross the narrower red dotted rectangle. It’s certainly an important part of the market, but both sides of the market are actually better off, in the long-term, if policy makers focus on the black square rather than the red.

Supply/Demand curves

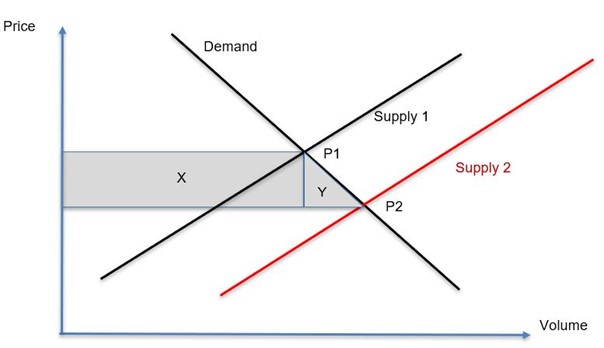

Such discussions always begat the dreaded supply/demand curve. Say a new government policy will subsidise more supply to a market. An economist would draw the following graph:

Figure 2: Effect of additional supply

The policy will move the supply line right from supply 1 to supply 2. The price would fall from P1 to P2, meaning customers could save from their existing costs the area X. The price fall would also encourage more consumption, creating the triangle of area Y. The “gross” customer benefit (the red box in figure 1) is X+Y.

However think also about existing suppliers’ revenue: due to the fall in price, this would fall by X. Therefore X is a “wealth transfer” from one group to another. It represents a shuffling of the deck chairs but has not actually improved the ship as a whole.

Y represents the net market benefit: we have put some new chairs on the ship’s deck. This is unquestionably good and is what policy makers and regulators should be striving for, not X.

It is easy to fall into the trap of seeing a virtue in maximising X for its own sake: falling into a romantic Robin Hood notion of redistributing from the producer to give to the consumer. But that is nonsense, as a successful economy relies on the profitability of both.

The magic of a market economy is that the profit motive drives all parties towards innovation and productivity initially for their own benefit, but that competition will, in the long-term, ultimately share the value of innovation to all.

How is this theory used in practice?

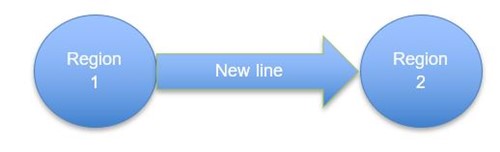

An example of the correct use of net market benefit theory is the Regulatory Investment Test (RIT) used to justify monopoly regulated infrastructure. Imagine we are considering building a line from a region that has surplus cheap generation into one with more expensive generation (figure 3).

Figure 3: Building monopoly networks

Let’s simplify by assuming demand is inelastic, i.e. even though prices will change, we don’t expect it to materially change the level of consumption.

The line may be beneficial to the industry as a whole by saving on input costs. The input savings that RITs recognise include:

- Replacement of expensive energy in Region 2 with cheaper Region 1 energy.

- If demand peaks are diverse, less generation capacity (i.e. reduced capital and labour inputs to the industry).

RITs also recognise improvements in industry outputs:

- If the line can prevent the occasional blackout in Region 2, then this can be assessed at the Value of Customer Reliability (VCR), a high value which represents the large consumer inconvenience of blackouts.

If these allowable net market benefits exceed the new input cost of building and maintaining the line, then the RIT passes.

This is a similar assessment to what a vertically integrated utility would have done in the pre-market days, using well understood “Resource Cost” modelling. And, if government sets a price or limit on pollution, the modelling can readily and accurately account for it by simply adding it to input costs.

Why not use customer benefits?

The customer benefits approach would be to limit the assessment to the red box in figure 1, which implies including the area X in figure 2. This involves assessing how much consumers would pay for energy with and without the line, i.e. how will prices change?

As stated previously, the area X is a wealth transfer between different parties that doesn’t add value to the industry as a whole. But at the same time the new line will definitely add new costs. If all we want to do is move deckchairs, then this seems a very wasteful way to do it.

Of course, policy makers want low prices. A properly competitive market should lead to the lowest efficient prices over the long run. If, for example, a policy reduces costs to suppliers, then competition should lead to those savings being passed downstream. By taking this attitude, a policy maker’s job becomes easier: they can focus on conventional industry productivity, whilst leaving the distribution of its benefits to the magic of competition.

But competition has its doubters. Things can go wrong, for example in nineteenth century US railroads. But just like the US did in that case, the underlying problem inhibiting competition can be addressed without building duplicative infrastructure. One should instead be looking at, say, unnecessary barriers to entry. Such things can be fixed at effectively no cost.

Customer benefits were once tried in the NEM

The original National Electricity Code had a process for building interconnectors regulated by the National Electricity Market Management Company (NEMMCO). In the months before the NEM started in December 1998, NEMMCO assessed a South Australia to New South Wales interconnector (SNI). NEMMCO used something akin to the current day RIT, however, the Code required the test be assessed against the interests of customers.

NEMMCO obtained legal advice that because the word “customers” was italicised, the test had to be a customer benefit only (there was debate at the time as to whether the italicisation was a typo). NEMMCO knew this would be problematic.

NEMMCO’s assessment showed that under a net-benefits/resource cost assessment, the line stacked up. But something strange happened in the customer benefits test. South Australia prices were modelled to fall thanks to SNI. However, in New South Wales, the exporting region, prices would go up. Because there were many more customers in New South Wales, their customer disbenefits exceeded the customer benefits in South Australia. Therefore NEMMCO concluded, apologetically, that a line that they considered worthwhile had actually failed the test due to negative customer benefits.[i] In fact it is likely that had this price-based test been extended to existing interconnectors, it would have recommended that some should actually be cut.

The New South Wales Government, who had proposed the interconnector, was unsurprisingly disappointed by this outcome and insisted that the test be reviewed as one of their pre-conditions to allowing the NEM to start. That review, carried out by Ernst & Young, recommended the current RIT form which explicitly relies only upon Net Market Benefits[ii].

This conclusion, whilst being the sensible approach for economic reasons, is also a relief for the modellers. The customer benefits test required forecasting price outcomes which are notoriously subjective. For example, forecasting bidding behaviours requires guessing future industry ownership structures, which can change at any time.

Thankfully, resource cost modelling is much less subjective and disputable than price modelling. It is the approach used in AEMO’s Integrated System Plan.

A net market benefit approach is also used when rule change is quantitatively assessed. This expectation was made clear during the second reading speech of the introduction of the National Electricity Law’s (NEL) National Electricity Objective (NEO). The speech explained the intention of the NEO well:

“The national electricity market objective in the new National Electricity Law is to promote efficient investment in, and efficient use of, electricity services for the long-term interests of consumers of electricity with respect to price, quality, reliability and security of supply of electricity, and the safety, reliability and security of the national electricity system.

The market objective is an economic concept and should be interpreted as such. For example, investment in and use of electricity services will be efficient when services are supplied in the long run at least cost, resources including infrastructure are used to deliver the greatest possible benefit and there is innovation and investment in response to changes in consumer needs and productive opportunities. The long-term interest of consumers of electricity requires the economic welfare of consumers, over the long term, to be maximised. If the National Electricity Market is efficient in an economic sense the long-term economic interests of consumers in respect of price, quality, reliability, safety and security of electricity services will be maximised.” [iii]

Customer benefits tests emerging in government policy

Despite the approach taken by the NEL and its market bodies, and the weight of supporting academic literature, governments nevertheless frequently promote their own policies with customer benefits assessments. Whilst these can be useful to explore distributional issues, for the reasons above, should never be a justification for government policy.

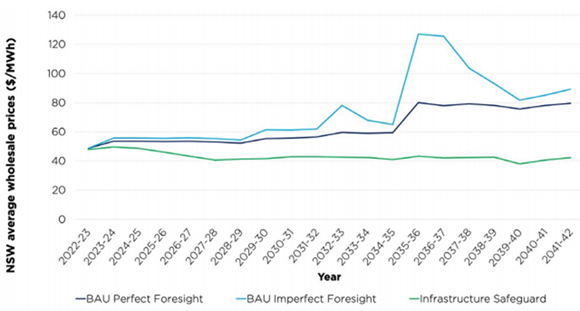

A recent example of this, but far from the only one, was the modelling results prepared by Aurora Energy Research and released with the 2020 NSW Roadmap legislation.

Figure 4: Estimated wholesale price effect of NSW roadmap

Source: NSW Electricity Infrastructure Roadmap Detailed Report November 2020

The above modelling of prices is effectively a customer benefit exercise. No estimate of resource costs was provided. Intuitively, as it is designed to subsidise plant to be constructed earlier than would otherwise occur, it would be expected to raise input costs through additional capital (see figure 1). And, as there was negligible load interruption forecast with or without the policy, it would not seem to materially improve outputs.

It therefore seems likely that the net market benefits would not be positive. Thus the customer benefits shown above derive entirely from wealth transfers from producers to consumers. Furthermore, the BAU prices forecast for the 2020’s were under $60/MWh: roughly the minimum required to recover the cost of recently built renewable plant. Hence there seems no concern about an expected failure of competition that might justify some kind of intervention.

It’s true that government policies of this nature can have environmental benefits. However if government ascribes an emissions price or budget, this is readily capturable in a resource cost modelling (although not in customer modelling).

Jobs

Another development is governments recently justifying energy policies through the virtue of creating additional jobs in the industry[iv]. But this runs counter to good economics: in figure 1 labour is an input to the industry that good policy should try to minimise, not maximise. This is perfectly obvious: we want to use as few resources as possible in making domestic energy, so those resources can be redeployed to where they add new value to the economy. And by keeping this input low, resulting lower prices will mean energy consumers will have money to fund productively employing activities elsewhere in the economy.

Wasteful over-manning was in fact one of the reasons for de-regulating energy markets from the early 1990’s, a time of higher unemployment than today.

Conclusion

The above discussion is nothing more than basic microeconomics and common sense. Policy decisions and monopoly infrastructure planning should be aimed at creating the most productive possible playing field so that markets can work within them as efficiently as possible. They should not be about moving deckchairs: that should be left to markets.

This has formed the sensible basis for the NEM, with market rules and network planning approaches following a “net market benefits” or “resource cost” approach. It may initially be surprising that the NEO, the long-term interests of customers, does not imply purely studying customer benefits. However after going through the thinking process, it is clear that a focus on net market benefits will in fact provide customers the best long-term outcomes.

It is concerning to see governments now frequently deviating from this common sense.

[i] Academia Edu, S. Littlechild, Australia: SNI and Murraylink Revisited

[ii] Ernst & Young Review of the Assessment Criterion for New Interconnectors and Network Augmentation Final Report

[iii] Hansard, SA House of Assembly 9 February 2005

[iv] Victorian Department of Environment, Land, Water and Planning, Victorian Renewable Energy Zones Development Plan Directions Paper, February 2021, p.3

Related Analysis

Addressing Energy Affordability Needs More Than Short-Term Relief

The conflict in the Middle East has continued to highlight the challenges we face in ensuring energy supply remains accessible and affordable for everyone. Ensuring Australia becomes more resilient to international energy price shocks will dominate the energy policy landscape for some time, and rightfully so. But while political debate often gravitates toward regulatory interventions and subsidies that deliver short term household bill relief, the real solution lies in something far more complex: reshaping how the energy system works for consumers. What’s increasingly clear is that energy affordability is not just about price - it’s about design. That is why the AEC is releasing its Affordability Action Agenda today – an 8-point plan of critical actions that industry and governments need to take to ensure that energy remains accessible and affordable for all Australians. Read more.

Getting it right: How to make the “Solar Sharer” work for everyone

On paper, the government’s proposed "Solar Sharer Offer" (SSO) sounds like the kind of policy win that everyone should cheer for. The pitch is delightful: Australia has too much solar power in the middle of the day; the grid is literally overflowing with sunshine: let’s give households free energy during 11am and 2pm. But as the economist Milton Friedman famously warned, "There is no such thing as a free lunch." Here is a no-nonsense guide to making the SSO work.

Energy Affordability: Will Solar Sharer reduce energy costs?

Energy affordability has been a hot topic for the last few months. Whilst the first term of the Albanese Government could be characterised as being focused on shifting the narrative on renewables development, it seems likely that its second term will need to consider how to deal with affordability, for both households and businesses. So what is the likely direction of travel for energy prices in the medium term, and is there anything industry and consumers can do to minimise the impacts? And can measures like the announced Solar Sharer help?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.