by Carl Kitchen

Cost storm hits UK offshore wind

As Australia prepares for its first offshore wind projects, the leading international market for offshore wind, the UK, has hit some rough seas due to a combination of low strike contract prices being offered under its Contracts for Difference scheme and major increases in overall project costs.

Like all current energy developments offshore wind is being impacted by factors like increased interest rates and financing costs, inflationary pressures and supply chain issues, all of which are pushing up the costs of new projects. Its latest Contracts for Difference auction price cap was set at GBP44/MWh but resulted in no offshore project proposals. We take a look and consider what is proposed in response to support the UK’s ambitious offshore wind target of 50GW by 2030.

Well suited

The UK is considered to be well suited to offshore wind farms given its relatively shallow coastline and relative lack of land mass for onshore wind. The UK currently has 14 GW of offshore wind installed, and around a further 9GW committed for installation. As a result, the UK currently has the largest offshore wind fleet outside of China. But it also has significant targets for offshore wind to meet - its Offshore Wind Sector Deal signed in 2019 targeted 30GW by 2030, and this was subsequently increased to 50GW, which is the current target. To reach the higher target it was forecast that around 8GW in new projects would need to be committed in each of the next two auction rounds as well as the round that just concluded.

Offshore wind is seen as one of the UK’s biggest infrastructural successes with prices falling substantially over the past eight years. In 2015 new offshore wind cost nearly £120 (~$230) per megawatt hour and by 2022 that was down to around £40.

A competitive Contracts for Difference (CfD) auction process was launched in 2014. The UK’s CfD are for 15 years and are entered into by the project developer and a government-owned company known as the Low Carbon Contracts Company (LCCC). Like any CfD scheme, if the UK’s market reference price is below the strike price of the contract, generators receive a top-up payment to cover the difference. Conversely, if the reference price is above the strike price, the generator pays back the difference.

The UK plans to hold its auction rounds (AR) annually beginning from March this year. Previous rounds were held in 2015, 2017, 2019 and last year and prices offered have continuously declined until the most recent round. AR1 had an average price of GBP117.24/MWH, while AR2 prices ranged from GBP57.50 to GBP75.75 depending on commissioning dates. AR3 prices ranged from GBP41.611 to GBP39.65. By AR4 strike prices were below wholesale power prices at GBP37.35 for delivery of projects in 2026-27.

Disappointment, but no surprise

AR5 failed to attract any offshore wind projects, an outcome described as a “disappointment, but not a surprise”. The administrative price cap set for offshore wind in AR5 was GBP44/MWh and below electricity prices. Given the increased costs emerging for energy projects the UK Government had already increased its CfD budget in August by GBP22 billion to try to address concerns, but it did not change the cap on strike prices, which was seen by some as the only way to address the increased costs[i]. The peak body for the UK energy industry, EnergyUK, had previously warned that the AR5 had not recognised the scale of cost increases.

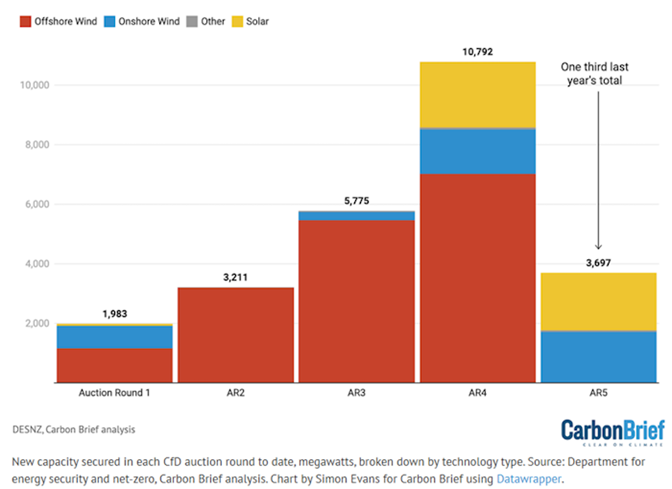

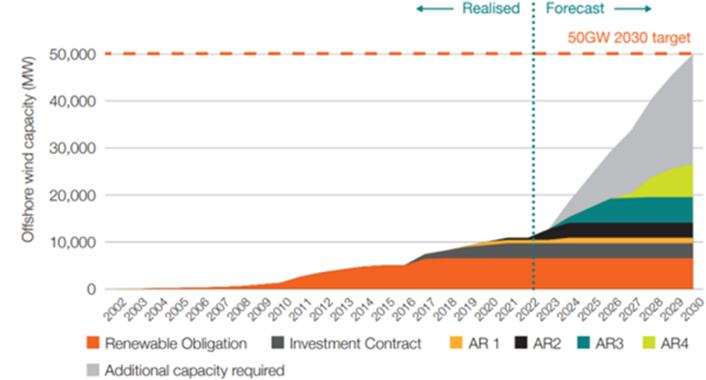

The cost of offshore wind is estimated to have increased by 40 per cent[ii] over the past year. EnergyUK found that factors like inflation, interest rate rises pushing up financing costs, supply chain difficulties, and regulatory uncertainty because of systemic problems with grid connections and planning, have led to higher overall project costs. It had forecast that around 8GW of offshore wind would need to be committed over the AR5, AR6 and AR7 rounds to hit the UK’s target. Figure 1 shows the commitments from previous auction rounds and the most recent AR5 and the drop in offshore wind capacity project bid into the auction, while figure 2 shows EnergyUK’s projections of what is needed to hit the 50GW target in 2030.

Figure 1: Outcome of auction rounds in UK by capacity type

Source: Carbon Brief

Figure 2: Projections of capacity required to meet 2030 offshore wind target

Source: EnergyUK

Analyst Stephen Bull, Executive VP at Aker Solutions and chair of RenewableUK, claims the current situation has created a “broken model”. After a period of auction success and offshore wind costs being driven down, they have now increased substantially while the CfD had not kept pace with the market. “Contract terms, strike prices – this is the broken model essentially… it’s not a sustainable business today financially”.

He argues a new deal is required with “smarter policy mechanisms, stronger local investments in infrastructure and jobs and a more collaborative, risk sharing industry environment”.

International law firm, Norton Rose Fullbright, also points to an announcement by Vattenfall earlier this year to stop the development of the 1.8GW Norfolk Boreas offshore wind project as a “concerning example of the practical realities of the cost crisis facing the UK offshore wind sector”. That project was successful in AR4. In announcing its halt to Norfolk Boreas development, Vattenfall said it remained committed to the Norfolk Offshore Wind Zone and work on Norfolk Vanguard West and Vanguard East would continue.

Aside from the strike price for the auctions the UK Government also tightened flexibility for generators to nominate a start date, which reduces their ability to take advantage of higher wholesale prices before starting the CfD. Under the changes the LCCC can issue a Unilateral Commercial Operations Notice (UCON) around when a CfD would be deemed to have begun. When it considers that commercial operations have started this would also trigger the generator’s liability to pay the difference between higher wholesale prices and the CfD strike price.

But in a fine balancing act and to continue to encourage early commissioning of projects, the UCON can only be issued after the Target Commissioning Window[iii] has started, which means generators can still operate their project on a merchant basis prior to commencement of this window.

There are now calls for the CfD to be reviewed, for a re-run of the CfD with a new strike price, or for next year’s auction to be brought forward. Project proponents will likely need to consider alternative offtake arrangements to replace or supplement the support from the CfD scheme.

The UK Government is considering possible changes to the CfD scheme to introduce non-price factors as part of the assessment criteria. In doing that it has acknowledged that low margins and a tough economic environment are making it harder for proponents.

It sought feedback on introducing non-price factors and tested whether and how to introduce mechanisms to value criteria other than just cost through CfD auctions. This in itself is unlikely to be a simple fix as noted in the response to the consultation:

“Government will need to consider if non-price factors are the appropriate policy tool to respond to specific issues and market failures for other technologies in ways that are similar to offshore and floating wind – the nature of the market volatility and supply chain bottlenecks are different for each technology, and therefore different policy interventions for different technologies might be more suitable. Government recognises the challenge of having numerous technologies competing in a single auction pot with different non-price factors applying. Pot structure is reviewed ahead of each allocation round and is based on a range of factors including the need to maintain competitive tension in auctions.”

To reach its targets the UK Government will need to respond in some way to maintain a pipeline of offshore wind projects. Another hurdle to the UK meeting its 50GW goal is competition for parts and skills elsewhere in Europe. Having the onshore infrastructure in place in time to connect new projects is also cited as another.

As we are discovering in Australia, there are serious challenges emerging which could stymie the intention to get more low carbon capacity into the system. Developers here too will be facing similar cost pressures due to a range of issues and will be following developments in the UK closely for any lessons that can be drawn.

[i] https://www.newcivilengineer.com/latest/lack-of-offshore-wind-in-new-cfd-shows-governments-fundamental-misunderstanding-of-renewables-11-09-2023/#:~:text=But%20this%20year's%20fifth%20round,been%20squandered%2C%20according%20to%20analysts.

[ii] See Energy and Climate Intelligence Unit, https://eciu.net/analysis/reports/2023/offshore-wind-all-at-sea

[iii] Target commissioning window can be a year before the target commissioning date and a year after.

Related Analysis

Wild Cards: Could these technologies advance the energy transition?

In December 2022, scientists at the National Ignition Facility achieved a landmark nuclear fusion result: a reaction that produced more energy than the laser pulse used to start it. It made headlines globally, but the caveats came quickly. Overall system energy use was still far higher, and commercial viability remains decades away. It was a real breakthrough, but also a reminder of how far the engineering still has to go. That gap between scientific progress and commercial reality is a defining feature of the energy transition today. While solar, wind, and batteries are scaling rapidly and doing most of the heavy lifting, the International Energy Agency estimates that nearly half of the emissions reductions needed for net zero will depend on technologies still at demonstration stage or earlier. This raises the key question: which “wild card” technologies could help close that gap?We take a look.

Integrated System Plan – What Should We Expect?

The release of an expert study of last year’s autumn wind drought in Australia by consultancy Global Power Energy[i] this week raised some questions about the approach used by the Australian Energy Market Operator’s in its 2024 Integrated System Plan (ISP). The ISP has been subject to debate before. For example, there has previously been criticism that some of the ISP’s modelling assumes what amounts to “perfect foresight” of wind and solar output and demand[ii], rather than a series of inputs and assumptions. The ISP is produced every two years and with the draft of the next ISP (2026) due for release soon, it is useful to consider what it is and what it is not, along with what the ISP seeks to do.

Nuclear Fusion Deals – Based on reality or a dream?

Last week, Italian energy company ENI announced a $1 billion (USD) purchase of electricity from U.S.-based Commonwealth Fusion Systems (CFS), described as the world’s leading commercial fusion energy company and backed by Bill Gates’ Breakthrough Energy Ventures. CFS plans to start building its Arc facility in 2027–28, targeting electricity supply to the grid in the early 2030s. Earlier this year, Google also signed a commercial agreement with CFS. These are considered the world’s first commercial fusion-power deals. While they offer optimism for fusion as a clean, abundant energy source, they also recall decades of “breakthrough” announcements that have yet to deliver practical, grid-ready power. The key question remains: how close is fusion to being not only proven, but scalable and commercially viable, and which projects worldwide are shaping its future?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.