by Carl Kitchen

Clean energy generation: On track or lagging behind?

An International Energy Agency (IEA) assessment of 18 energy-related technologies has found that only one - solar PV, which was deployed at record levels last year – is on track to meet long-term climate, energy access and air pollution goals.

The IEA tracks a range of energy technologies and sectors that it considers are critical to achieve a transition to lower emissions[i].

Its most recent Tracking Clean Energy Progress assessment found that most of the technologies were not on course to meet reduction targets, and that this contributed to a global increase in carbon emissions of 1.4 per cent in 2017.

The agency’s assessment considers where technologies are today, and where they need to be to reach the Paris Agreement’s “well below 2°C” climate target, based on the agency’s own Sustainable Development Scenario (SDS).

The SDS was developed to outline the scale of the transformation needed. Under the SDS, energy-related carbon dioxide (CO2) emissions are expected to peak around 2020 and then decline rapidly. By 2040, they are expected to be at around half of today’s level and on course toward net-zero emissions in the second-half of the century.

So what’s on track and what’s not?

Tracking Clean Energy Progress is intended to give a detailed assessment of recent progress, deployment rates, investment levels, and innovation needs.

Its power category includes generation technologies as well as carbon capture and storage while “energy integration technologies” include energy storage, smart grids, demand response, digitalisation, hydrogen and renewable heat sources.

Technologies significantly not on track included coal-fired generation, which is responsible for 72 per cent of energy sector emissions. The IEA notes that development of coal plants rebounded in 2017 after falling for the previous three years. It also notes that carbon capture and storage remains stalled. Also in the energy sector, onshore wind and energy storage were downgraded last year as their progress slowed.

Below we look at what the assessment reveals for gas, coal-fired, and nuclear power generation.

Gas-fired generation

The IEA found that gas generation developments slowed in 2017 to 1.6 per cent. This was mainly driven by a decline of 7.6 per cent in the United States, where gas prices increased.

There was growth in the amount of gas generation in other parts of the world, which grew by 4.6 per cent overall, with China leading the way. The amount of gas generation in China increased 17.2 per cent, while in India it rose 13.3 per cent. The European Union also increased strongly by 12.3 per cent.

The 2017 outcome followed significant growth in gas plant developments in 2016. The IEA described 2016 as a “remarkable year” with gas generation increasing by almost 6 per cent (this compares to a historical average growth rate of 4.7 per cent in the 15 years to 2015). Gas-fired power plants benefited as gas oversupply lowered prices in key regions.

Gas generation was also assisted by carbon price signals in several jurisdictions helping gas displace coal in the supply mix.

In terms of new investment, gas-fired power increased by nearly 40 per cent in 2017, led by the US and the Middle East/North Africa. Despite the positive trend, final investment decisions for new gas-fired power plant capacity fell to 50 GW in 2017, which was the lowest level in a decade (although final investment decisions for gas plants were more than 1.5 times those for coal). The slowdown was attributed to a drop in projects in the US and the Middle East and challenging market conditions in places like Europe with persistently low wholesale power prices.

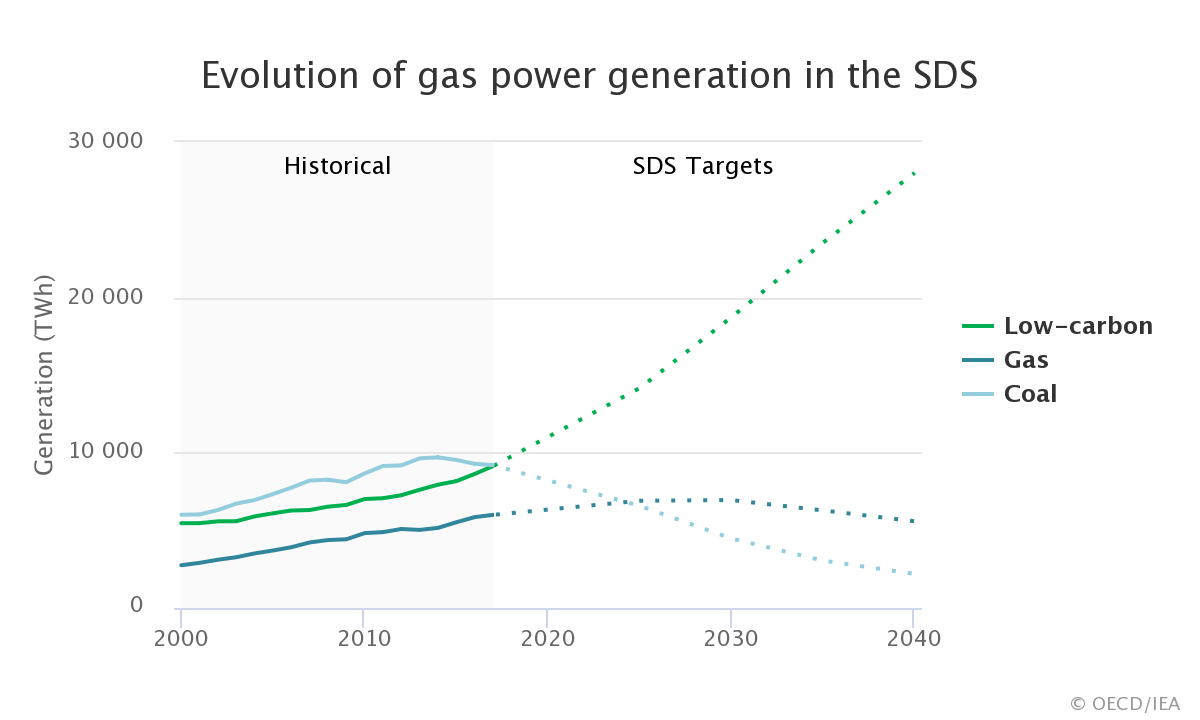

Figure 1

Source: IEA

The agency notes that gas is facing “fierce” competition from cost-competitive renewables. Growth prospects for gas will be affected not only by the competitiveness of gas prices, but also by the recognition of the benefits of gas compared to coal for pollution.

While gas as a transition fuel has fallen behind the SDS target, it tends to vary greatly from year to year. The report notes that a key factor for gas development will be improving flexibility, which will assist the integration of a growing amount of renewables.

Coal-fired power stations

Unabated coal-fired power generation (plants without Carbon Capture, Utilisation and Storage, or CCUS) increased by 3 per cent in 2017, offsetting the previous year’s decline – and rebounding after three years of consecutive falls.

The IEA notes that this growth is driven by increases in coal generation in China (+4 per cent) and India (+13 per cent) due to rising electricity demand. Southeast Asia also experienced strong generation growth.

The United States and the European Union experienced generation declines in 2017, of -33 TWh and -22 respectively. In the US competitive gas generation and renewables have pushed out coal, according to the report, while low gas prices and carbon policies prompted switching to gas in the EU.

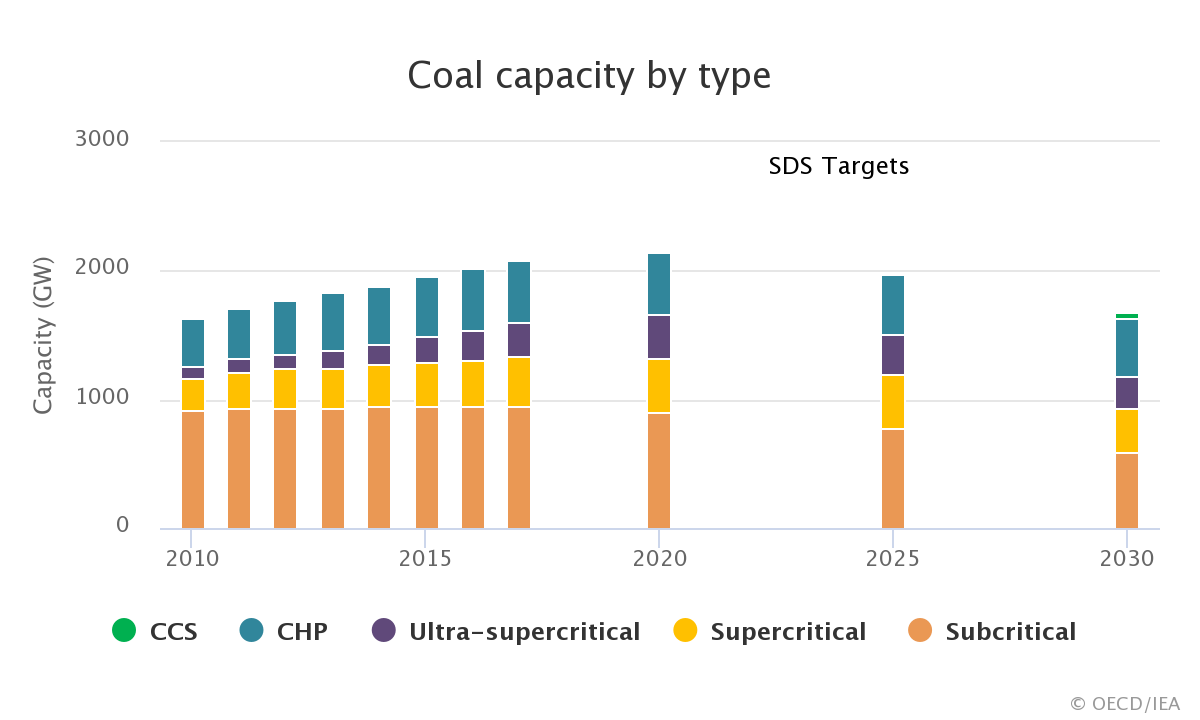

Coal-fired power generation remains the largest source of electricity generation (37 per cent) worldwide and is responsible for 72 per cent of energy sector emissions. The report notes that investments have moved to more efficient supercritical and ultra-supercritical coal power generation technologies. In 2017, the total capacity of current subcritical plants waned as retirements of over 20GW exceeded capacity additions.

Unabated coal-fired power generation is currently not on path to meet the SDS target. The agency estimates that it requires an annual decrease of 5.6 per cent until 2030, and current investment levels are nowhere near enough to increase coal-fired power generation with CCUS from less than 1 TWh today to the SDS goal of 305 TWh by 2030. The capacity of coal plants already exceeds the SDS generation target, so the report states that more retirements and/or decreased utilisation is required.

Figure 2

Source: IEA

Despite the increase in generation, investments worldwide in coal power dropped by one-third (led by China) due to a slowdown of new coal plant commissions. Capacity of final investment decisions also experienced a drop to 30 GW, the lowest level in over 15 years. This decrease has been led by China, India and Southeast Asia. In China, low power plant utilisation rates are an indication of an overcapacity of coal, as gas and renewable energy generation sources continue to grow.

The agency’s analysis shows that while unabated coal-fired power generation appears to be peaking, new investment is still happening in some regions and the rate of the world moving away from non-CCS coal is currently nowhere near enough to achieve the SDS target.

Nuclear power

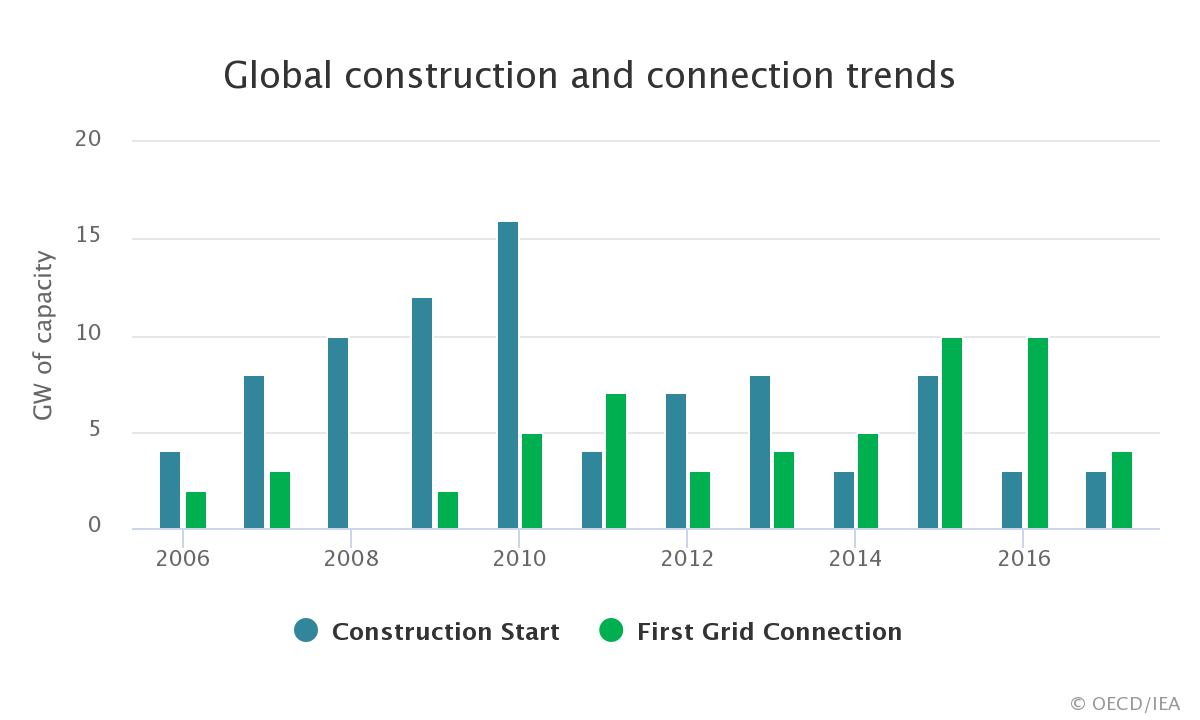

In 2017 nuclear generation new capacity fell to 3.6 GW, from 10 GW in 2016 (Figure 3). Construction starts, a proxy for final investment decisions, remained low. Declining investment, announced phase-out policies and planned retirements, combined with only 56 GW of nuclear capacity under construction in 2017, suggest that meeting the goal of 185 GW of net increase needed by 2030 will be challenging.

Figure 3

Source: IEA

Over the past five years, 33 GW of capacity was connected to the grid, with China forming two-thirds of this total. Over the same time, 18 GW has been shut down including 7.3 GW in Japan and 4.9 GW in the United States.

China, India, and Korea account for half (31 GW) of the reactors currently under construction. Over the past two years construction starts have been low in China with 2.3 GW in 2016 and a 600 MW fast reactor in 2017. However China is now “poised” to commence construction on several new reactors, with up to eight approvals anticipated in 2018 - this is mostly due to the government’s five-year plan for nuclear power development released in 2016, which projected 58 GW installed plus another 30 GW under construction by 2020.

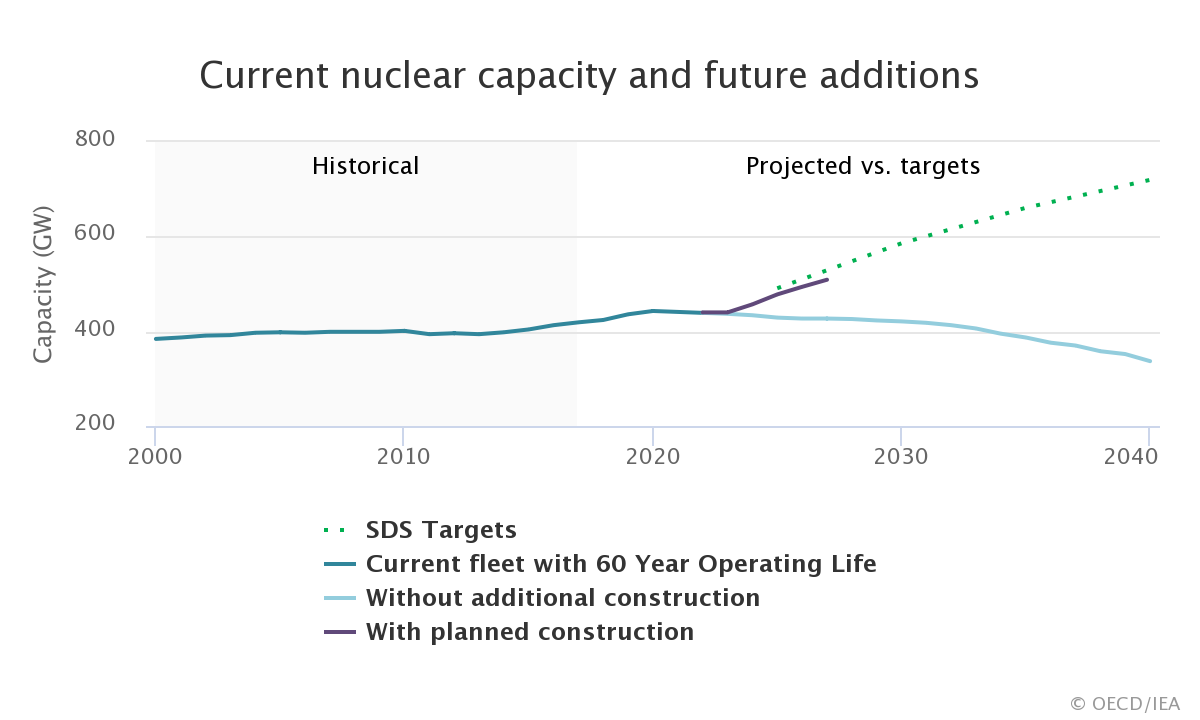

Nuclear power is expected to be on track to meet the 2020 SDS target of 438 GW installed capacity, as construction of 40 GW is completed. However, since it takes more than five years to build a nuclear plant, it will be increasingly unlikely that nuclear power will meet the 2025 target of 490 GW installed capacity, as global phase-outs offset progress. Nuclear policies also remain uncertain. Construction decisions by China, India and Russia in 2018-2020 will play a major role in whether nuclear power will meet the SDS targets in 2030 and beyond.

Figure 4

Source: IEA

While nuclear is currently behind the SDS target, China’s ambitions may help it to catch up. If China executes its five-year plan and India fulfils its plan for 63 GW by 2032, the IEA estimate that the SDS targets could be reached. In addition, the Russian state-owned corporation Rosatom signed more than ten agreements in 2017. While many of these are exploratory, some show progress towards actual construction.

A following article looks at the IEA’s assessment of wind, solar and CCS generation.

[i] Tracking Clean Energy Progress, International Energy Agency (https://www.iea.org/tcep/)

Related Analysis

Climate and energy: What do the next three years hold?

With Labor being returned to Government for a second term, this time with an increased majority, the next three years will represent a litmus test for how Australia is tracking to meet its signature 2030 targets of 43 per cent emissions reduction and 82 per cent renewable generation, and not to mention, the looming 2035 target. With significant obstacles laying ahead, the Government will need to hit the ground running. We take a look at some of the key projections and checkpoints throughout the next term.

Certificate schemes – good for governments, but what about customers?

Retailer certificate schemes have been growing in popularity in recent years as a policy mechanism to help deliver the energy transition. The report puts forward some recommendations on how to improve the efficiency of these schemes. It also includes a deeper dive into the Victorian Energy Upgrades program and South Australian Retailer Energy Productivity Scheme.

2025 Election: A tale of two campaigns

The election has been called and the campaigning has started in earnest. With both major parties proposing a markedly different path to deliver the energy transition and to reach net zero, we take a look at what sits beneath the big headlines and analyse how the current Labor Government is tracking towards its targets, and how a potential future Coalition Government might deliver on their commitments.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.