by Carl Kitchen

As reliable as clockwork: A debate on NEM supply

This week the question of what reliability standard should be applied to the National Electricity Market re-emerged when the Victorian Government declared it would raise the issue at the upcoming COAG Energy Council meeting next week.

Victoria’s Energy Minister, Lily D’Ambrosio, wrote[i] that the state would be asking the Energy Security Board (ESB) to come up with a new reliability standard which “accurately – and actually – reflects our current energy needs”. Assessment of the Reliability Standard for the National Electricity Market (NEM) is normally undertaken by the Reliability Panel for the Australian Energy Market Commission (AEMC).

The most recent review was completed last year and found that the standard and its settings were still achieving their purpose and were likely to continue to do so. Under the auspices of the AEMC, the panel included generators, energy users, retailers, networks and the Australian Energy Market Operator (AEMO).

The Victorian Energy Minister also argued that the current reliability standard “doesn’t consider longer, hotter summers. It doesn’t take into account ageing, failing coal stations”. Yet in its annual assessment of electricity supply reliability, AEMO includes forced outage rates for power plants, and this year it also factored in the probability of outages at units at Loy Yang A and Mortlake to extend into summer. Those units are currently expected to be in operation for the summer peak period.

AEMO’s Electricity Statement of Opportunities (ESOO) also takes into account likely peak demand based on weather modelling which incorporates the changing climate.

In the ESOO[ii], the market operator did flag the potential need for a change in the reliability standard and suggested that a reliability standard closer to a 1-in-10 year event was more appropriate than the current reliability standard of demand being met for 99.998 per cent[iii] of the time.

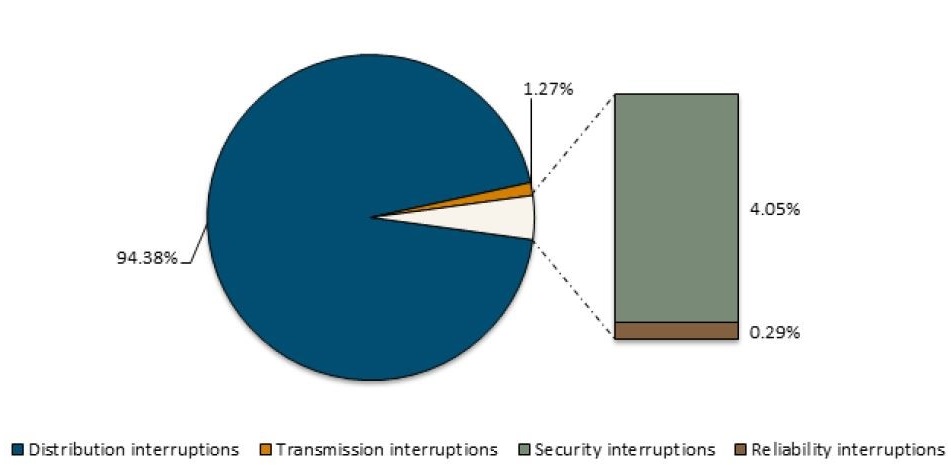

The reliability standard is designed to deal with the adequacy in the total capacity of generation which is responsible for 0.3 per cent of all supply interruptions that customers have actually experienced in the last 10 years as shown in Figure 1.

Figure 1: Sources of supply interruptions in the NEM: 2007-08 to 2017-18

Source: AEMC

Source: AEMC

Nervousness over the availability of generation at peak periods is not unique to Australia, it has also been the focus of commentators in the US in relation to the energy-only market in Texas, better known as ERCOT (Electric Reliability Council of Texas). Unlike the rest of the US, Texas is an energy-only market like the NEM and does not have a reliability standard mandated by a capacity obligation upon retailers. It instead relies on a high price cap of US$9,000 MWh (around A$13,000, which compares to the NEM price cap of $14,700).

In the federal sphere, the US North American Reliability Commission (NERC) sets target power reserve margins essentially based on 1 loss of load event (LOLE) in 10 years, or reserve margins of about 14 per cent and US capacity markets target their capacity obligations upon these targets. As Texas has no obligation, there are frequent debates as to whether their energy-only market will achieve this standard, and indeed whether it should even attempt to.

This year ERCOT experienced a hotter than usual summer with the state setting a new peak demand record (74,666 MW on 12 August 2019). There were no firm load shutdowns in the system despite it only having a reserve margin of 8.6 per cent. It did declare an Energy Emergency Alert Level 1 twice and there were many days with tight conditions[iv].

In 2018 ERCOT commissioned the Brattle Group[v], to assess and estimate the Market Equilibrium Reserve Margin (MERM) and the Economically Optimal Reserve Margin (EORM) for ERCOT’s wholesale electricity market.

The Brattle Group report[vi] estimated a market equilibrium reserve margin of 10.25 per cent under projected 2022 market conditions[vii] and an economically optimal reserve margin of 9 per cent, based on the risk-neutral, probability-weighted average cost of 57,000 simulations. Whilst these are different reliability metrics to what are used in Australia, they are clearly less conservative to that being imposed by NERC on other US markets.

It also noted that the estimated societal costs were relatively flat with respect to a reserve margin near the minimum level and that there was only a modest variation between reserve margins of 7-11 per cent.

Based on its findings the report concluded that ERCOT’s current market design would support more than sufficient reserve margins from an economic perspective.

In another assessment of the performance of ERCOT, the Regulatory Assistance Project[viii] (RAP) noted that: “NERC and most system operators employ an extremely conservative interpretation of a conservative standard. System operators, regulators, and government appear to tacitly endorse a goal of never curtailing any firm load — an uneconomic and unachievable objective — by treating every instance of firm load curtailment, no matter how rare, as a failure not to be repeated in future.”[ix]

RAP writes that the result of the more conservative approach adopted in NERC’s 1-in-10 LOLE has led to mandatory capacity margins leading to levels of capacity investment that, at the margin, costs consumers (US)$100,000/MWh or more.

In its comments RAP said: “If that strikes you as vastly more than consumers would knowingly pay to avoid briefly postponing or foregoing some of their more flexible electricity needs, that’s because it is. Many consumers, especially large industrial and commercial consumers, are happy to shift some of their more discretionary loads by a few hours for a tiny fraction of that cost,” the RAP assessment says.

RAP goes on to state, “Why the disconnect? It turns out that the ‘one event in ten years’ standard has its origins in technical papers from the 1940s, if not earlier, and has never been backed by an objective benefit-cost assessment.”

The Brattle Group noted in a report to the AEMC earlier this year[x] that studies had found that achieving a 0.1 LOLE standard implies a VOLL (Value of Lost Load[xi]) of US$200,000/MWh or higher, significantly above most empirical estimates of VOLL.

Reliability will continue to be hotly debated given the changing shape of the electricity grid and heightened political concern about keeping the lights on. The important thing from an industry perspective, as noted in the Reliability Panel’s most recent assessment, is that in the current environment of a transforming sector, stability in market frameworks is extremely important.

[i] “It’s past time for sorting out energy reliability”, The Age, 13 November 2019

[ii] https://www.energycouncil.com.au/analysis/esoo-and-reliability-what-does-it-tell-us/

[iii] This equates to on average the risk of not being able to meet customer energy demand being limited to 0.002% of the desirable energy consumption.

[iv]http://www.ercot.com/content/wcm/key_documents_lists/161478/5.1_Summer_2019_Operational_and_Market_Review.pdf

[v] The Brattle Group is an international consultancy. It was also commissioned by the AEMC to look at reliability frameworks in the NEM and produced the report, “High-Impact, Low-Probability Events and the Framework for Reliability in the National Electricity Market”, February 2019

[vi] Estimation of the Market Equilibrium and Economically Optimal Reserve Margins for the ERCOT Region 2018 Update, Final Draft

[vii]http://www.ercot.com/content/wcm/lists/143980/10.12.2018_ERCOT_MERM_Report_Final_Draft.pdf

[viii] The Regulatory Assistance Project (RAP)® is an independent, non-partisan, non-governmental organisation involving former utility and environmental regulators, industry executives, system operators and other policymakers and officials with extensive experience in the power sector. www.raponline.org

[ix] https://www.raponline.org/blog/a-hearty-bowl-of-texas-soup-how-ercot-keeps-the-lights-on/

[x] High-Impact, Low-Probability Events and the Framework for Reliability in the National Electricity Market”, February 2019

[xi] Now referred to as the Market Cap Price in the NEM

Related Analysis

Ireland’s Green Energy Rule: What Can Australia Learn From Its Approach to Data Centres?

A recurring theme at the Australian Energy Council’s inaugural Energy2050 Conference was the challenge of managing the rapid growth of data centres and their increasing electricity demand. While data centres present a significant economic opportunity for Australia, policymakers are grappling with how to support investment while minimising impacts on customers, the electricity system, and emissions. We take a look at Ireland’s recently introduced data centre policy and explore the lessons it may offer for Australia.

The ‘f’ word that’s critical to ensuring a successful global energy transition

You might not be aware but there’s a new ‘f’ word being floated in the energy industry. Ok, maybe it’s not that new, but it is becoming increasingly important as the world transitions to a low emissions energy system. That word is flexibility. The concept of flexibility came up time and time again at the recent International Electricity Summit held in in Sendai, Japan, which considered how the energy transition is being navigated globally. Read more

International Energy Summit: The State of the Global Energy Transition

Australian Energy Council CEO Louisa Kinnear and the Energy Networks Australia CEO and Chair, Dom van den Berg and John Cleland recently attended the International Electricity Summit. Held every 18 months, the Summit brings together leaders from across the globe to share updates on energy markets around the world and the opportunities and challenges being faced as the world collectively transitions to net zero. We take a look at what was discussed.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.