by Carl Kitchen

A fresh challenge: How to account for zero or negative demand?

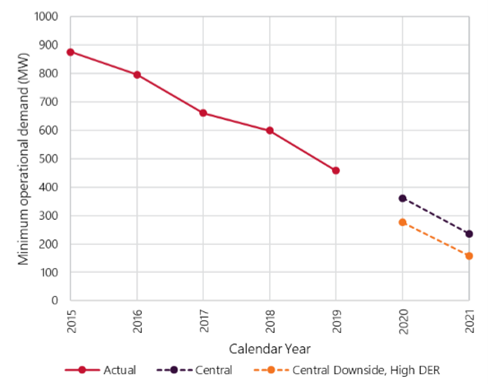

The continued fall in minimum demand levels to new record lows in South Australia is raising a new challenge for the market.

On 11 October, South Australia set another new low for operational demand of 300MW – 158MW lower than the minimum recorded less than a year earlier (10 November 2019). The state’s minimum demand levels are being driven by the take up of rooftop solar and occur on fine clear, mild days in spring and early summer, particularly on weekends and public holidays. This is when low demand coincides with high generation from solar.

This relentless growth in rooftop solar does not seem to have been affected by COVID-19, somewhat of a surprise considering the workforce restrictions that were in place and the related economic downturn.

The Australian Energy Market Operator’s (AEMO) 2020 Electricity Statement of Opportunities flagged that SA was likely to experience periods of negative demand in 2024, but the recent record is already lower than projected in AEMO’s central scenario. It is now being projected that zero or negative regional demand could occur as early as September 2021.

The dramatic shift in minimum demand is illustrated in figure 1.

Figure 1: Minimum operational demand in South Australia (90 per cent probability of exceedance)

Source: AEMO

The falling minimum demand has thrown up technical and system security challenges, and encouraged new operating strategies. This year also saw AEMO release a fact sheet on how it would manage the issues posed by this situation[i].

It has also thrown up a fresh and rather unexpected challenge for the market operator and retailers – how to recover AEMO’s non-energy costs in this situation. This is because the settlement system, which allocates costs to market participants, was not designed for a power system with two-way flows at significant scale and it did not foresee a situation where there may be no “customer energy” from which to recover the non-energy costs that are allocated to energy users (you can see the issues paper here).

Under the National Electricity Rules AEMO provides market participants with a financial settlement service for billing and clearing of all market trading.

The issue is this: AEMO is required to allocate all or some of the non-energy costs - such as ancillary services, the Reliability and Emergency Reserve Trader mechanism and administered price caps or floor price compensation - to market customers based on their share of energy in a given trading period.

A customer’s share is based on the total of the net metered energy amount for all classified loads in the region for the same time period. But if aggregate regional demand is zero or negative, the settlement system can’t calculate the relevant energy cost recoveries and, according to AEMO’s issues paper[ii], that would cause the entire automated settlement system run to fail because energy and reallocation transactions are part of an integrated process for settlement purposes.

On top of that there would also be no information available to determine prudential requirements. The prudential requirements oblige market participants to post a certain amount of credit support (such as bank guarantees) to the market operator. This is to deal with the risk of participant default.

For market settlement and calculating non-energy recovery amounts, AEMO uses net meter data for each trading interval and market participant. The net meter data provides an energy value for settlement, fees and recovery calculations for all registered participant categories. This arrangement has been in place since the NEM began operating in 1998.

Cost recovery is based on adjusted gross energy (AGE) – which is the energy value adjusted for distribution losses - for the trading periods and calculated using net metering data – the risk of zero or negative AGE is expected to increase with the introduction of five-minute settlements which come into effect in October next year.

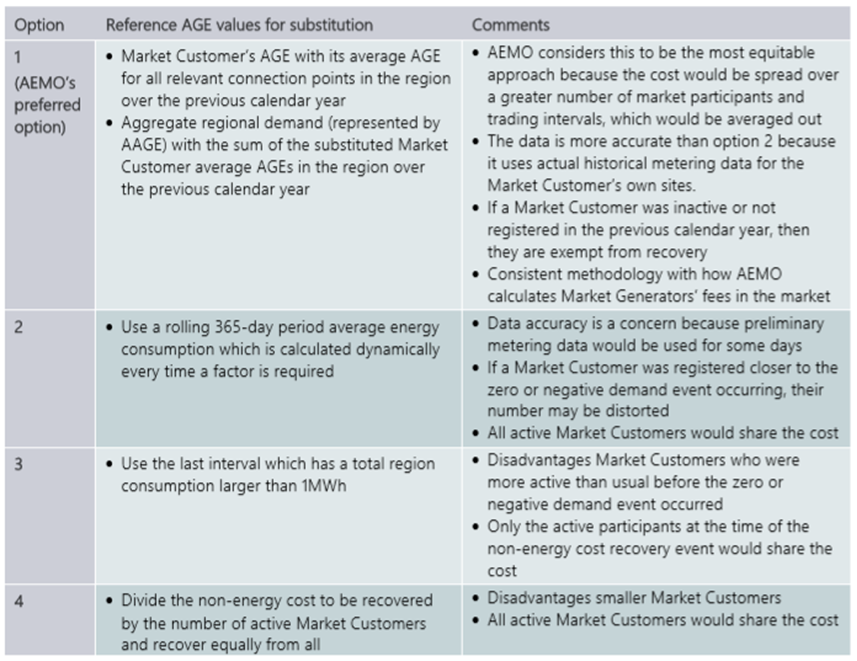

The options put forward, along with their advantage and disadvantages, are outlined in the table below. None of these are perfect solutions, with each creating a degree of winners and losers.

AEMO has already proposed a rule change for integrating energy storage systems (ESS) into the NEM which includes a non-energy costs recovery approach from bi-directional resource providers and market small generation aggregators. Based on that ESS proposal and its issues paper, the market operator intends to engage with the Australian Energy Market Commission. It is also urgently seeking market participants views with the intention of submitting a rule change in January next year for a more equitable and enduring solution.

In conclusion, this unexpected market settlement twist is just one of myriad issues that the transitioning electricity industry must resolve, necessitating an urgent and imperfect fix. However zero demands have been predicted for some years. This case study provides a learning of how all parts of the industry should keep abreast of planning documents, anticipate the likely impacts of industry change, and act before such problems become imminent.

[i] Operational management of low demand in South Australia, AEMO, 22 October 2020

[ii] NEM settlement under zero and negative regional demand conditions, AEMO Issues Paper, November 2020

Related Analysis

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Energy Dynamics Report - A Tale of Minimum Operational Demand and Wholesale Price declines

The third quarter saw significant price declines compared with the corresponding quarter in 2022 right across the NEM. At the same time with increased output from solar and wind generation inin Queensland’s case, minimum operational demand records were set or equaled in every region. The quarter also saw the highest-ever level of negative price intervals with all regions showing an increase. We dive in to the pricing and operational demand detail of AEMO’s Q3 Quarterly Energy Dynamics Report.

Data centres: A 24hr power source?

Data centres play a critical role in enabling the storage and processing of vast amounts of online data. However they are also known for their significant energy consumption, which has raised concerns about their environmental impact and operating costs. But can data centres be fully sustainable, or even a source of power?

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.