by Graham Pearson

Will the WEM have enough capacity?

The Australian Energy Market Operator (AEMO) has released its latest Wholesale Electricity Market (WEM) Electricity Statement of Opportunities (ESOO). The WEM ESOO is important in setting the Reserve Capacity Requirement (RCR) and also offers valuable insights into the future shape of the WEM as well as the challenges it will need to deal with.

The growth in distributed rooftop solar is again a key feature of the WEM ESOO. It has contributed to new records in minimum operational demand and remains a major challenge in the WEM. But the biggest takeaway from the 2022 WEM ESOO is the sharp reduction in excess capacity in the short term and the forecast capacity shortfall from 2025-26. This capacity imbalance doesn’t take into account the the WA Government’s announcement to retire Synergy’s remaining coal-fired plants.

Below we consider some of the key numbers in the WEM ESOO, as well as what the forecast capacity shortfall might mean for the future of the market.

Solar juggernaut continues

The WEM ESOO has shown again that Western Australia’s love of solar is continuing with 357MW of distributed photovoltaic (DPV) – residential and commercial rooftop solar systems and other smaller non-scheduled PV capacity up to 10MW – installed in 2020-21, a slight increase compared to the previous year.

The South West Interconnected System (SWIS) now has 2,042MW of DPV connected as at March 2022 and collectively it remains the largest generator in the SWIS. To put this into perspective, the SWIS has 1,371MW of coal generation[1], 1,647MW of gas generation and 1,011MW of wind generation.

And there are no signs of DPV slowing down. The WEM ESOO forecasts that DPV will grow at an average annual rate of 7 per cent or 238MW per year. This means that the installed capacity will be approximately 4,716MW by 2031-32, a big jump on last year’s WEM ESOO forecast installed DPV capacity of 4,069MW by 2030-31.

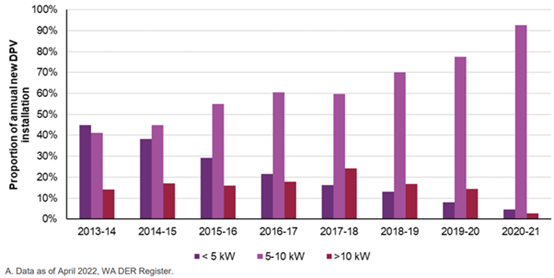

The WEM ESOO paints a clear picture of DPV continuing to grow over the coming decade. However, there is one number that is declining and that’s the amount of larger >10kW residential rooftop solar installations.

Figure 1: Proportion of annual new DPV installation by system size, 2013-14 to 2020-21A

Source: ESOO, page 35

Smaller <5 kW rooftop solar systems had the market share in 2013-14 and have since been displaced by larger systems as costs have reduced. The amount of rooftop solar installations >10kW were on an upward trajectory until 2017-18 when they reached a peak of 24 per cent of the market. Since then, the amount of smaller and larger installations have fallen and 5-10kW installations have accelerated to take 93 per cent of all installations in 2020-21. The trend toward 5-10kW systems and the reduction in larger systems is perhaps explained by the increase in equipment and shipping costs during Covid-19 and the lower buyback rates under the Distributed Energy Buyback Scheme.

Minimum demand reaches new record

The staggering amounts of DPV and its forecast growth over the next decade is important because it is central to one of the biggest challenges in the SWIS: minimum demand.

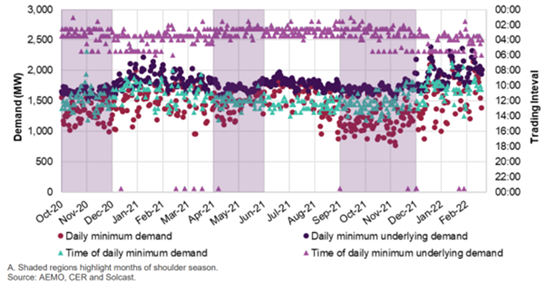

Five new minimum demand records have been set since the 2021 WEM ESOO. The current minimum demand record of 765MW occurred on 14 November 2021 when DPV reduced demand by 1,253MW. From October 2021 to February 2022, DPV was estimated to have reduced minimum demand during daytime hours on average by 773MW.

The divergence between minimum demand (i.e. demand from the network) and minimum underlying demand (i.e. demand from the network plus an estimation of rooftop solar PV and battery storage) is shown in the below figure alongside the time of day that the minimum demand occurs. The gap between minimum demand and minimum underlying demand is greatest in the spring months where there are sunny days, rooftop solar PV is producing full output and there is less need for cooling. Minimum demand in summer shifts earlier in the day to between 9:30am and 11:00am.

Figure 2: Daily operational and underlying minimum demand, 2020-21 to 2021-22A

Source: ESOO, p45

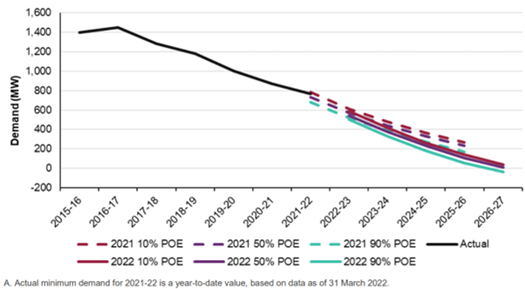

According to AEMO, minimum demand is forecast to decline rapidly from 546MW in 2022-23 to 11MW in 2026-27, at an average annual reduction of 62.1 per cent. Highlighting the pace of change, AEMO warned only as recently as 2019 that the minimum level of operational demand required for system security is about 700MW.[2]

Figure 3: Minimum demand and 10%, 50% and 90% POE minimum demand forecasts under the expected demand growth scenario compared to actuals, 2015-16 to 2026-27A

Source: ESOO, p50

Peak demand increases

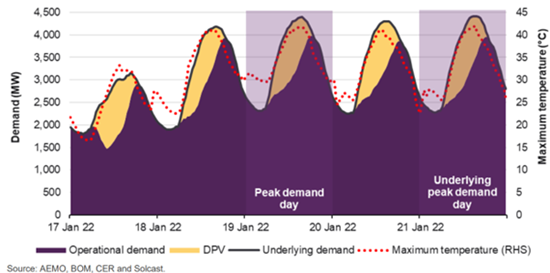

While minimum demand will continue to decline, the WEM ESOO simultaneously forecasts peak demand to increase over the next decade at an average annual rate of 0.9 per cent. This is driven by stronger growth from large industrial loads, residential customers, and the uptake of electric vehicles.

The 2021-22 operational peak demand of 3,984MW was the second-highest annual peak since the WEM commenced in 2006. It came after two consecutive days with maximum ambient temperatures above 41°C and high overnight temperatures. The record for underlying peak demand occurred two days later on 21 January 2022.

Figure 4: Demand and temperature profiles for a five day period covering the peak demand day (19 January 2022) and underlying demand day (21 January 2022)

Source: ESOO, p42

The future of the SWIS

The WEM ESOO puts a spotlight on the limits of the existing generation fleet as more DPV has entered the SWIS, minimum demand nosedived and peak demand climbed.

The WA Government pointed to these issues in their recent announcement to close Collie Power Station in late-2027 and Muja D in late-2029, in addition to Muja C's Unit 5 closing later this year and Unit 6 in 2024.

“WA's electricity system is being increasingly challenged by the overwhelming uptake of rooftop solar…

To address this, the State's energy generation system will embark on a sensible, managed transition to a greater use of renewables, while ensuring electricity reliability and affordability continues to be paramount.

An estimated $3.8 billion will be invested in new green power infrastructure in the South West Interconnected System (SWIS) - including wind generation and storage - to ensure continued supply stability and affordability.”

This announcement came only a few days before the release of the WEM ESOO and AEMO couldn’t factor this into their forecasts. Still, the WEM ESOO expects capacity to tighten over the coming years. The Reserve Capacity Requirement (RCR) is set at 4,526MW for the 2024-25 capacity year, with excess capacity projected to decline from 331MW (7.5 per cent) in 2023-24 to 8MW (0.2 per cent) in 2024-25. From 2025-26, the capacity shortfall is forecast to increase from 21 MW (0.5 per cent) to 303 MW (6.3 per cent) by 2031-32. This assumes no further capacity changes beyond the retirement of Muja C unit 6.

This tightening capacity and the retirement of Collie Power Station and Muja D raises an important question: what types of generation does the SWIS need and how can we get it?

Marsden Jacobs Associates (MJA) considered this in a report commissioned by the AEC on revenue adequacy for generators in the WEM. According to MJA, large amounts of new storage capacity must be introduced to satisfy demand and maintain supply reliability, while significant investment in intermittent wind and solar generation is needed to meet emission reduction targets.

The trouble is that solar generation is not economic without Large-scale Generation Certificates (LGC) at strong prices because DPV is depressing the dispatch weighted price for energy delivered in the balancing market. On top of this, much of the SWIS is already constrained and Western Power has not identified any significant transmission upgrades to support more solar and wind generation entering the grid. Those developers that are proposing new projects are often facing lengthy connection agreement timeframes with the network operator and are unlikely to be able to get their projects operational before excess capacity tightens in the next few years.

Storage is one type of generation that could be located in the south-west to take advantage of existing transmission and the Premier has already suggested that pumped hydro options are being considered for the area. However, for the private sector, it’s still difficult to put together a business case for investment in battery storage. MJA’s modelling shows that 4-hour battery storage has marginal economic returns until around 2024/25. After that, annual revenue starts to increase and 4-hour storage becomes economic but it relies on an investor taking a long-term view and banking on settings becoming favourable in the future.

To compound things further, MJA points out in their report that longer duration battery storage will be required in the future as peak demand extends beyond 5 hours. The problem is that the ESR Obligation Duration, the Capacity Price formula and linear derating method does not provide an economic return for storage facilities exceeding 4 hours.

A coordinated approach to the future grid

The 2022 WEM ESOO is another insightful piece of work from AEMO that highlights the challenges and opportunities in the energy sector. In recent times, the triple threat of increased DPV, dropping minimum demand and increasing peak demand has rightly demanded a response and will require more focus in the coming years.

The release of the WEM ESOO and the WA Government’s de-carbonisation agenda does create an interesting pivot point and an opportunity to re-shape the market with right type of generation. The WA Government has foreshadowed additional wind and storage to replace Collie Power Station and Muja D, but it won’t be an easy void to fill with limited transmission capacity, long connection agreement timeframes and a reserve capacity market that does not adequately value battery storage. A coordinated and joint effort between the WA Government, Energy Policy WA, Western Power and developers will be critical to meeting this challenge.

[1] This includes the retirement of Muja C unit 5 in 2022

[2] See page 23 - https://www.aemo.com.au/-/media/Files/Electricity/WEM/Security_and_Reliability/2019/Integrating-Utility-scale-Renewables-and-DER-in-the-SWIS.pdf

Related Analysis

Is increased volatility the new norm?

This year has showcased an increased level of volatility in the National Electricity Market (NEM). To date we have seen significant fluctuations in spot prices with prices hitting both maximum price caps on several occasions and ongoing growth in periods of negative prices with generation being curtailed at times. We took a closer look at why this is happening and the impact this could have on the grid in the future.

Is there a better way to manage AEMO’s costs?

The market operator performs a vital role in managing the electricity and gas systems and markets across Australia. In WA, AEMO recovers the costs of performing its functions via fees paid by market participants, based on expenditure approved by the State’s Economic Regulation Authority. In the last few years, AEMO’s costs have sky-rocketed in WA driven in part by the amount of market reform and the challenges of budgeting projects that are not adequately defined. Here we take a look at how AEMO’s costs have escalated, proposed changes to the allowable revenue framework, and what can be done to keep a lid on costs.

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.