by Duncan MacKinnon

The rise of ancillary services

Ancillary Services are services that are essential to managing power system security and reliability, and ensuring electricity supplies are of an acceptable quality. Like the quality of the fuel you put in your car, these services are generally taken for granted, but they ensure that the electricity used in our lights, appliances and factories is safe and won’t cause expensive damage. They maintain the technical standards of the system including frequency standards, voltage and network loading, and with more and more renewables connecting to the grid with their natural output fluctuations, they will come into even sharper focus.

Like the electricity spot market, there is a market for ancillary services which runs in the background. Similar to the spot market for energy, generators (and loads) offer ancillary services and AEMO dispatches them, but the cost is then allocated to customers and generators based upon “causer pays” principles. Compared with the $10b p.a. of energy sold through the National Electricity Market, the ancillary services market is much smaller (about $30m p.a.), but this is about to change as greater demands are placed upon the generators (and loads) which provide these services, due to the increased penetration of renewable energy. Simultaneously, as dispatchable capacity is withdrawn the available supply of these services reduces.

South Australia is the nation’s test case for how renewable energy will be incorporated into the electricity market, so it’s worth looking at changes in the cost of their ancillary services as renewables have increased their share of generation. Table 1 shows how much has been paid to ancillary services providers for the state over the past few years:

Table 1: Payments to Ancillary Services Providers [i]

|

Calendar Year |

Ancillary Services Payments |

|

2012 |

$8.0m |

|

2013 |

$7.3m |

|

2014 |

$4.4m |

|

2015 |

$38.1m |

|

2016 (to date) |

$4.0m |

Source: Australian Energy Market Operator (2016).

The 2015 anomaly is explained by the loss of the Heywood Interconnector for 40 minutes on 1 November 2015.[ii] This sent the prices of the eight ancillary services up to the market price cap, ($13,800/MW, just like the spot market), and triggered the Cumulative Price Threshold[iii](again, just like the spot market).

Apart from the anomaly in 2015, the figures in themselves don’t look particularly interesting, but when they’re graphed, they show a different story.

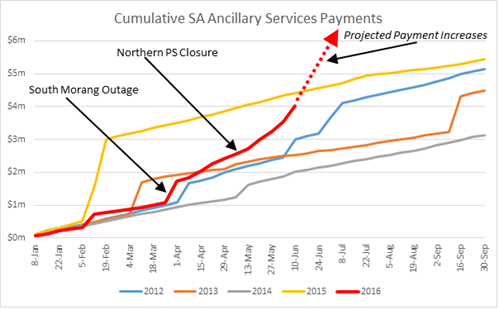

Figure 1: Cumulative SA Ancillary Services Payments

Source: Australian Energy Council analysis, based on AEMO data

As shown in Figure 1, on 26 March there was an unplanned outage of a circuit breaker at the South Morang Terminal Station 23km outside Melbourne. This had a cascading effect which constrained supply from Victoria to South Australia and required more ancillary services within SA. Again, limited supply caused increased prices and for 35 minutes ancillary prices were close to the price cap.

On 9 May 2016 the Northern Power Station closed, nominally removing 546MW from the power supply, but also up to 72MW in ancillary services. This means that SA has a reduced potential supply of ancillary services available. The services are now provided by only three generators, Pelican Point (owned by Engie), Torrens Island (owned by AGL) and Quarantine (owned by Origin). Intuitively we can expect that, with supply limited, the prices for providing these services will rise. The dotted line shows the trajectory, based on recent AEMO data.

Extrapolating the payments for this calendar year suggests costs could be in the order of $25m, excluding any unexpected outages which can cause material upward shifts in the market, e.g. the loss of the Heywood Interconnector in November last year.

What will this mean for wholesale market costs? South Australia’s annual energy consumption is about 13,500GWh[iv], which means that wholesale prices will increase by about $1.80/MWh. Based on the 2014-15 volume-weighted average SA price of $39.29/MWh[v], that equates to an increase of 4.7 per cent.

The increasing pressure on ancillary services is part of the reason why the SA Government is investigating the feasibility of another interconnector with NSW. According to ElectraNet, another electricity link “will improve wholesale market competition and power system security for SA, as well as facilitating renewable energy for Australia”[vi].

What might occur in the longer-term to change this supply-demand balance (particularly if a new interconnector is not economically viable)? Technically, wind farms can be configured to provide some ancillary services (although only when the turbines are spinning). As noted above, load sources can also in principle provide these services (or to look at it from a demand perspective, reduce the need for them). At historical price levels, there has been little incentive for these potential sources to compete with generators, and aggregation of many smaller providers may be required to match the scale of a coal or gas generator. While the cost allocation is required to be on a “causer pays” basis, there are many ways of allocating costs that meet this broad requirement. Some will drive sharper incentives on market participants to manage their costs, especially if the overall cost rises. AEMO periodically reviews the cost allocation methodology to ensure it is fit for purpose. The next such review may attract more attention than usual, especially in South Australia.

[i] http://www.aemo.com.au/Electricity/Data/Ancillary-Services/Ancillary-Services-Payments-and-Recovery

[ii] Australian Energy Regulator (2015). http://www.aer.gov.au/wholesale-markets/market-performance/fcas-prices-above-5000-mw-1-november-2015-sa

[iii] The Cumulative Price Threshold works in conjunction with the Administered Price Cap to provide short-term relief from sustained high spot prices.

[iv] Energy Supply Association of Australia (2015). Electricity Gas Australia

[v] Australian Energy Market Operator (2016). http://www.aemo.com.au/Electricity/Data/Price-and-Demand/Average-Price-Tables

[vi] http://www.premier.sa.gov.au/index.php/tom-koutsantonis-news-releases/697-state-budget-2016-17-study-into-new-interconnector

Related Analysis

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Green certification key to Government’s climate ambitions

The energy transition is creating surging corporate demand, both domestically and internationally, for renewable electricity. But with growing scrutiny towards greenwashing, it is critical all green electricity claims are verifiable and credible. The Federal Government has designed a policy to perform this function but in recent months the timing of its implementation has come under some doubt. We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.