by Rhys Thomas

The GHG Protocol: make or break for green data centres?

In the past few months, data centres have received significant attention as potential beehives for renewable investment and an antidote to the much-publicised tenor gap[i].

But some recent changes being discussed globally could complicate how businesses such as data centres purchase their electricity. If not navigated carefully, these changes could make the vision of 100 per cent renewable powered data centres a distant fantasy rather than a reality.

Let’s take a closer look.

Emissions profile of data centres

Something occasionally lost in the current speculation about data centre growth is that Australia already hosts many data centres – more than 250 according to some estimates, with over half located in Sydney and Melbourne.

While the emissions profiles of data centres vary in scale, the sources are mostly similar:

- Scope 1 emissions are usually on-site backup generation (e.g. diesel or gas) and refrigerant leakage from the cooling systems.

- Scope 2 emissions are the purchased electricity used to power the IT servers.

- Scope 3 emissions are from the value chain to build data centres (e.g. manufacturing of servers, construction materials).

It is Scope 2 emissions that are attracting the most attention.

The anticipated buildout of “hyperscale” data centres – very large data centres designed to meet the exponential use of AI – would significantly increase energy demand. At the moment, data centres account for about 1 per cent of total electricity consumption; by 2035, it could be as high as 11 per cent, which is around 35 TWh[ii]. For some comparison, the whole state of Victoria consumed 44TWh of electricity last year[iii].

Consequently, if energy supply does not also increase, then the result will be higher electricity costs and emissions. The Clean Energy Finance Corporation’s (CEFC) modelling warns that:

Without additional renewable energy and storage, data centre growth could significantly impact the electricity market, potentially increasing wholesale electricity prices by 26% in NSW and 23% in Victoria by 2035 … [it] could also lead to a 14% increase in grid emissions across the NEM[iv].

Can data centres attract renewable investment?

A major policy challenge with forecasting demand is the uncertainty and there is research suggesting future data centre demand is being overestimated[v]. Putting that to one side, there is an emerging expectation new large loads like data centres should meet its demand through renewable energy sources to support Australia’s energy transition.

The Commonwealth Government’s National AI Plan states it is developing national data centre principles that will “set clear expectations for sustainability and other factors, including bringing new renewable energy online”[vi]. Meanwhile, Minister Bowen said only yesterday “data centres do need to build new energy to go with it, and that energy will be renewable”[vii].

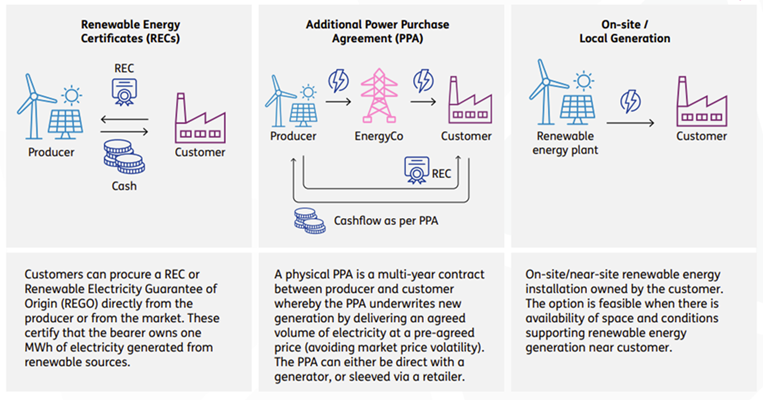

The illustration below, taken from the CEFC’s report on data centre growth, shows the different approaches to the procurement of green energy[viii].

Figure 1: Approaches to the procurement of green energy

Each approach involves trade-offs that data centre operators and policymakers will need to consider. For example:

- Building enough on-site renewable generation would require significant land that may not be available in city areas, not to mention these areas are generally not optimal sites for weather-dependent generation. It would also mean having back-up generation (presumably diesel, gas, or a large battery) to meet periods of high demand and/or weather intermittency.

- Power Purchase Agreements (PPAs) could help address the much talked about tenor gap but may also see renewable investment directed towards meeting additional demand rather than displacing fossil fuels from the grid.

- Volumetric renewable energy certificate purchases can be misleading as data centres are still relying on fossil fuels at certain times of the day.

The other soon-to-be option is the Electricity Services Entry Mechanism (ESEM). Once the Expert Panel recommendations are implemented, a data centre may procure the necessary bulk renewable generation, shaping, and firming it requires by the ESEM administrator. One benefit of this approach is the ESEM will be fungible, meaning it does not require a one-to-one match between data centre demand and the energy supply.

Ultimately, perfect should not be the enemy of the good and getting data centres to 100 per cent renewables (or even in the high 90s) probably will not be a clean-cut process. Making sure there is flexibility in the way renewable generation can be supplied will be important, as is ensuring renewable energy claims are accurate.

Balancing these two considerations has been at the heart of recent policy discussions about how Scope 2 emissions are calculated.

Calculating Scope 2 emissions

To take a very tedious but necessary step back, there are established regulations in place for how companies calculate and report their Scope 2 emissions. These regulations are contained in Australia’s National Greenhouse and Reporting Scheme (NGERS) which are in turn derived from the international Greenhouse Gas Protocol (GHG Protocol).

Over summer, the GHG Protocol undertook consultation on its Scope 2 emissions accounting. The consultation received almost 1,400 responses highlighting its significance.

Part of the consultation focused on reforms to how purchased electricity can be claimed. Two areas of these proposed reforms stand out:

- Hourly time matching – aligning renewable energy claims with the time of use.

- Deliverability – mandating that renewable certificates are sourced within the regional grid market boundary.

These reforms are designed to increase the accuracy of renewable energy claims, as well as provide targeted signals for renewable and storage investment. At a principled level, they appear sensible. But the devil is in the detail especially when it comes to deliverability.

The GHG Protocol has proposed to enforce “zonal pricing boundaries” in Australia’s National Electricity Market (NEM). This means the deliverable market boundary for renewable certificates is confined to each state rather than the NEM.

The AEC submitted against this proposed definition and recommended that the NEM be recognised as one physical region for deliverability. This reflects the NEM’s intended design feature of enabling interconnection across the wholesale electricity market to encourage efficient investment in generation.

Moreover, state restricted, hourly stamped certificates could be so scarce and illiquid to be unable to meet large corporate demand, or at best, only do so at very high cost.

Bringing it back to data centres

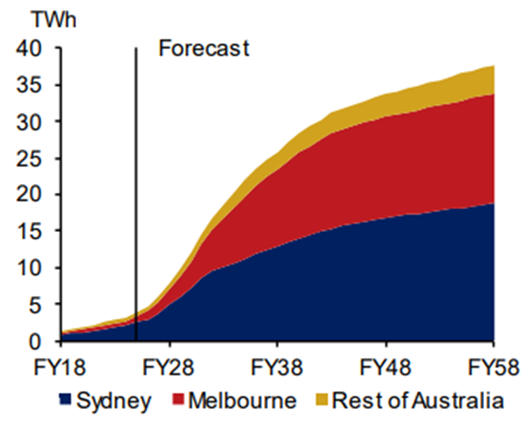

In line with the current trend, new data centres are expected to be highly concentrated within two specific locations – Sydney and Melbourne.

Figure 2: Data Energy Consumption Splits, AEMO Step Change

Source: Oxford Economics (based on AEMO Data), p5.

The regulatory and social licence expectations about data centre electricity consumption are still evolving. Key policy questions will at some point need answering such as:

- Must data centres be powered by only new renewable generation?

- Will data centres need to be 100 per cent renewable?

- Is 100 per cent volumetric or time matched?

These policy decisions alongside the GHG Protocol’s final guidance will significantly influence the economics of renewable powered data centres.

If the deliverability principle comes into effect as it currently reads, the pool of renewable generation (existing or new) available to meet this forecasted consumption will be substantially reduced. Only renewable generation in NSW could be used to support Sydney data centres, and likewise Victorian renewable generation for Melbourne data centres.

This could have distortionary impacts on the financing and efficiency of new renewable investment. For example, renewable developers may choose to build a new plant in Sydney to capitalise on data centre demand even though it would be cheaper for that plant to be built and operated in Queensland or South Australia and the energy supplied through interconnectors. This would have flow on implications for network build and congestion, costs that may be borne by customers rather than data centres.

Illiquidity of supply would be further exacerbated if hourly time matching were introduced alongside zonal pricing boundaries. The availability of certificates produced at certain times of the day, by new renewable generation, located in a single state would likely be too scarce and not enough to encourage competitive efficiencies.

At best, there would be a limited pool of very expensive certificates data centres could use to time match their consumption. At worst, there may not be enough certificates at certain times of the day, and some data centres will need to draw electricity from the grid, increasing costs and emissions.

As an example, Amazon is one data centre company that currently purchases renewable certificates to match their electricity consumption in Australia. This involves surrendering almost 350,000 certificates, each representing 1MWh of electricity[ix]. Amazon’s commitment is part of a global company pledge and the company says it is “the world’s largest corporate purchaser of renewable energy”[x].

This is no mean feat but even this level of ambition would not suffice under potential future rules because Amazon has sourced its generation from different parts of the NEM and the certificates are volumetric (i.e. not time matched)[xi]. Not to mention Amazon’s electricity consumption will only increase as it builds out new, hyperscale data centres.

None of this is to argue against time matching. Rather, because market demand and IT infrastructure for time matching is still maturing, it would seem preferable to keep the renewable generation pool as large as possible, so long as it is located within the NEM.

Conclusion

It goes without saying there are many variables in this article. Demand forecasting is highly uncertain and the GHG Protocol has not made any final determination on its proposed reforms.

Nonetheless, it is important to keep these possibilities in mind to minimise unintended consequences to Australia’s energy transition. In this case, defining deliverability in Australia to state boundaries does not seem to be the right call – it goes against the NEM’s intended design and may inadvertently form a barrier to investment in new and time-matched renewable generation.

[i] The tenor gap refers to a mismatch between the long-term contracts needed by sellers to finance capital-intensive assets (often 10 to 30 years) and the short-term contracting of buyers (typically three to seven years).

[ii] Clean Energy Finance Corporation, December 2025, Getting the balance right: data centre growth and the energy transition, p5.

[iii] Australian Energy Regulator, February 2026, Annual electricity consumption.

[iv] Clean Energy Finance Corporation, December 2025, Getting the balance right: data centre growth and the energy transition, p5.

[v] Oxford Economics, November 2025, Estimating data centre ‘phantom demand’.

[vi] Department of Industry, Science and Resources, 2025, National AI Plan, p11.

[vii] Australian Financial Review, February 2026, Data centres should bring their own green power: Bowen.

[viii] Clean Energy Finance Corporation, December 2025, Getting the balance right: data centre growth and the energy transition, p23.

[ix] Green Energy Markets, March 2025, What is the real size of Australian corporate demand for Renewable Energy?, p5.

[x] Amazon News, January 2024, Amazon is the world's largest corporate purchaser of renewable energy for the fourth year in a row.

[xi] PV Tech, June 2025, Amazon to invest in AU$20 billion in Australian data centres powered by solar PV.

Related Analysis

Energy2050: Building the ‘Light on the Hill’ for Australia’s Net-Zero Future

Today, we are pleased to publish an important report for the Australian Energy Council and the energy industry. Energy2050 is intended to be a vision statement, providing a practical illustration of what it will take to deliver a net zero energy system while balancing affordability, reliability and sustainability. Read more.

Clarity and understanding key ingredients for successful transition

The energy system is complex and decarbonising the grid adds further complexity. It requires significant new investment to ensure coal plants can exit without having an impact on the reliability of the grid. It comes with unavoidable costs and will take time to get right. It is increasingly important given this context that the energy transition is well understood. Selective framing of data to apportion blame works against a broad understanding and has the potential to undermine customer confidence and support for the transition. Read more.

Joint AEC-CEC rule change to enhance system security frameworks

As the National Electricity Market accelerates its transition to higher levels of renewable energy, maintaining system security has become a critical challenge. In response, the Australian Energy Council and Clean Energy Council have lodged a joint rule change request to strengthen planning, governance and procurement frameworks for essential system services. The proposal aims to support an orderly transition while ensuring the grid remains secure and investable. Read more.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.