by Duncan MacKinnon

Standing on the outside, looking in

Recently the International Energy Agency published its Energy Policies of IEA Countries – Australia 2018 Review[i] (IEA Report). What interesting statistics did the IEA uncover, and what does the world think of our energy policies? We take a look.

Discussion

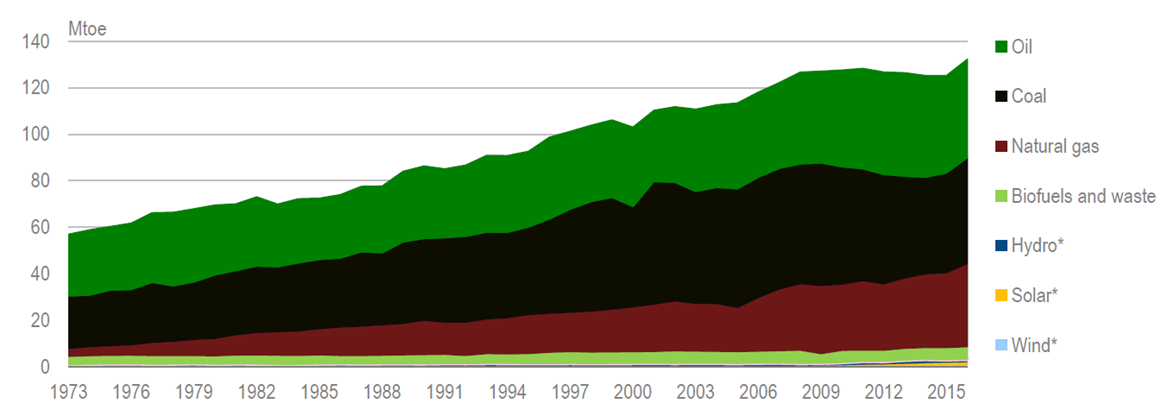

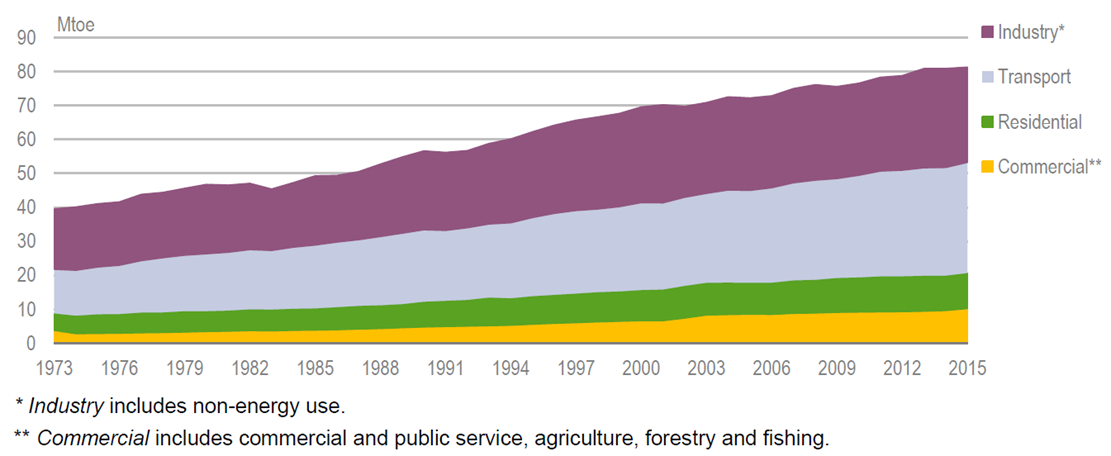

The report deals with Australia’s total energy position and presents data showing energy supplies over time (Figure 1), as well as the sector where consumption occurs (Figure 2).

Figure 1: Total Primary Energy Supply by Source

Source: IEA Report, p.26

Source: IEA Report, p.26

Figure 2: Total Final Consumption by Sector

Source: IEA Report, p.27

Source: IEA Report, p.27

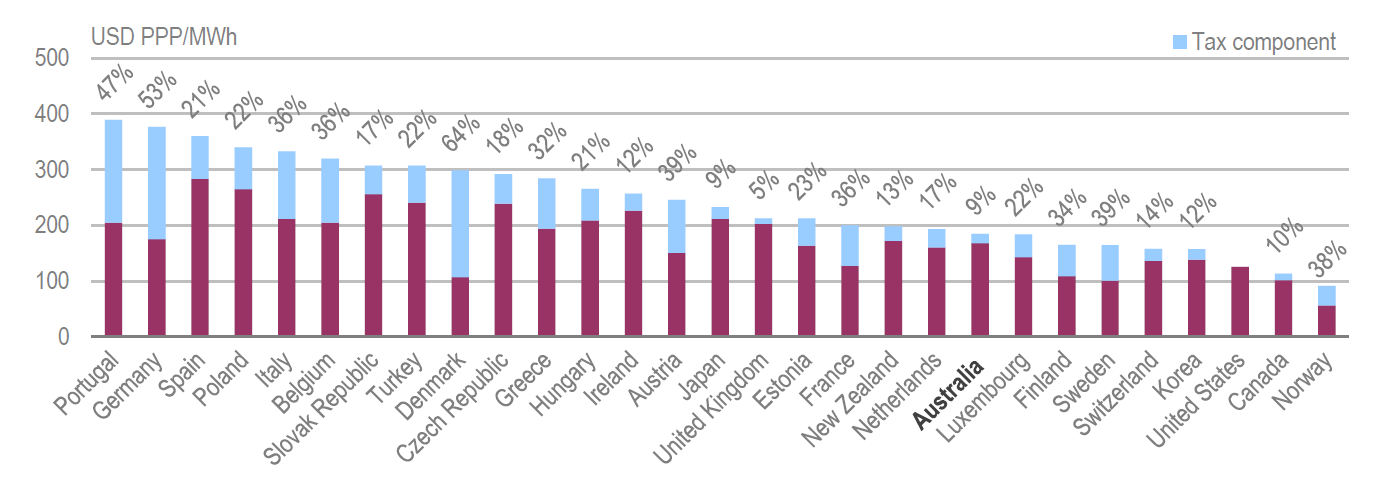

Other interesting data also appears in the report. For example, page 110 reports that “Electricity prices for households have increased significantly in Australia over the past decade, almost threefold, rising from USD 98 (AUD 134) per MWh in 2004 to USD 283 (AUD 314) per MWh in 2014.” However the report goes on to say that prices declined by 14 per cent in 2016 (except in Queensland) and when adjusted for purchasing power parity, Australian households’ electricity prices are among the ten lowest in the IEA member countries (Figure 3).

Figure 3: Household Electricity Prices in Purchasing Power Parity

Source: IEA Report, p.111

Source: IEA Report, p.111

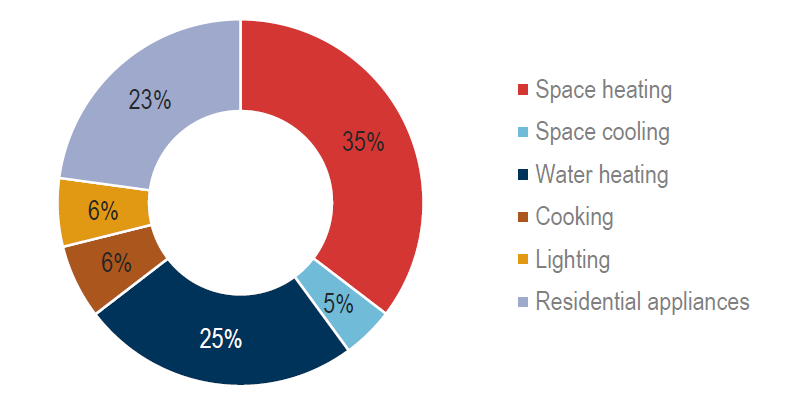

There is also other interesting household data. Despite the common knowledge that electricity consumption peaks in summer due to air conditioning load, the IEA Report shows that most domestic energy consumption is due to heating rather than cooling (Figure 4).

Figure 4: Energy Consumption in the Residential Sector

Source: IEA Report, p.211

Source: IEA Report, p.211

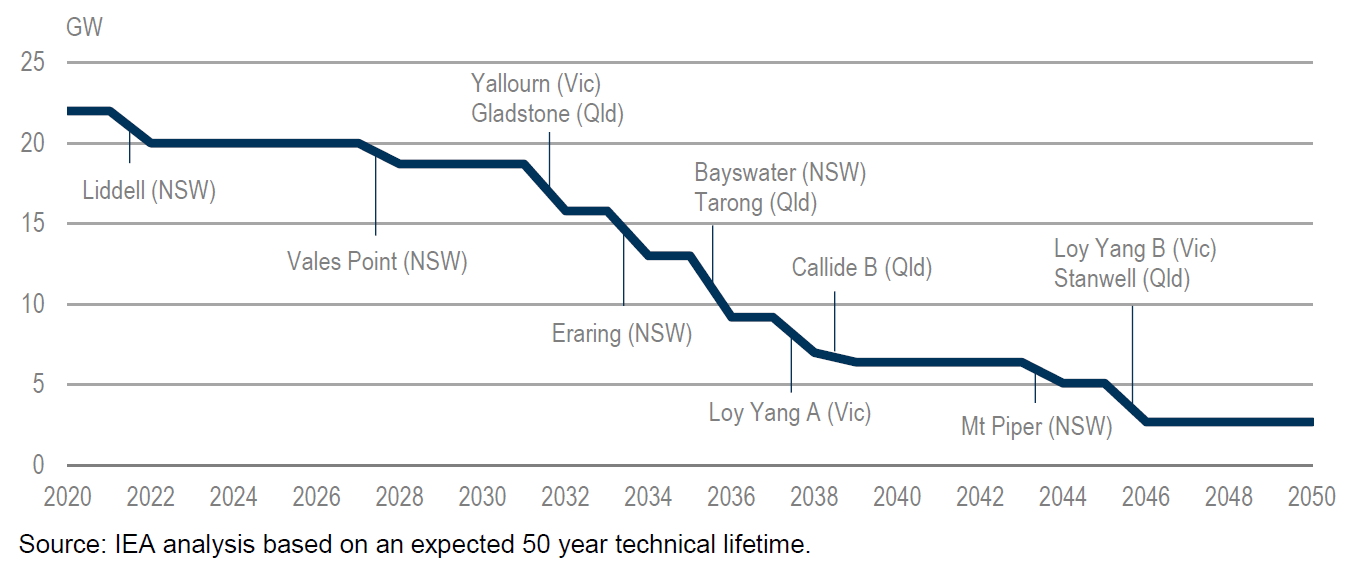

And while many are aware of the expected retirement schedule of NEM coal capacity, the IEA report presents it graphically, showing the 20GW reduction over the next thirty years (Figure 5).

Figure 5: NEM Coal-fired Plant Capacity & Closures

Source: IEA Report, p.182

Source: IEA Report, p.182

Analysis of Policies

The report focuses on two main areas, energy security and energy system transformation, both of which are related to the transition to renewable forms of energy. The report observes that, “the country is in a paradoxical situation: while Australia is well endowed with natural resources, energy security risks across several sectors have increased”[ii].

Energy security is an increasing challenge for Australia, and the report suggests the National Energy Security Assessment, last updated in 2011[iii], should be revised to consider the current situation in which:

- domestic oil production has declined by 30 per cent (along with domestic refining capacity);

- gas reserves needs to be developed sustainably to meet increasing demand (primarily from the LNG export industry);

- energy infrastructure has reduced resilience; and,

- electricity & gas security are more tightly linked.

Similarly the transformation of the energy system to fulfil Australia’s international climate change ambitions is happening at a faster pace and scope than expected, but the report concludes that, “[c]urrent energy efficiency measures and climate mitigation policies are not sufficient” and “domestic efforts need to increase”.[iv] It does believe the National Energy Guarantee offers hope and concludes that, “The NEG could be an effective market-based mechanism if the government can ensure more competition, better interconnection among the NEM regions and stringent rules for the integration of renewable energy capacity into the system. The NEG cannot become a ‘silver-bullet’ and its design should remain compatible with the NEM energy-only market, otherwise, it could create new barriers and windfall profits, if those elements are not considered.”[v]

Report’s Recommendations

The report made 40 recommendations for improving Australia’s energy policies, the key recommendations from which are:

“The Government of Australia should:

- Design an energy and climate policy framework for 2030 and develop a mid-century low emission development strategy, based on the outcomes of the 2017 review of the climate policies and the Finkel review.

- Improve governance through enhanced collaboration and clarified roles with states and territories through the COAG Energy Council and with market bodies of the NEM.

- Guide the energy transition through an emissions reduction goal for the power sector and provide a market signal to retire older and less efficient generation, while ensuring that plants provide sufficient advance notice of their intention to close.

- Continue to foster well-functioning wholesale and retail electricity markets through the COAG Energy Council in order to ensure efficient and innovative outcomes, to deliver security of supply and to more effectively integrate growing shares of variable renewable energy by:

- Reviewing and adapting technical standards and the procurement of ancillary services, including a strategic reserve to increase power system flexibility, resilience and reliability;

- Ensuring that low-emission technology support is market-based and guided by locational signals, supported by energy system-wide network planning.

- Adapting the distribution network regulation through harmonised technical standards, interoperability of resources in different states and consistent economic regulation.

- Develop competitive, liquid and adequate domestic gas supplies and transportation capacity by swiftly completing the gas market reforms. Support the sustainable development of domestic oil/gas reserves by addressing community concerns.

- Regularly update the National Energy Security Assessment, in order to identify energy security risks across the energy system, and design measures to reduce or eliminate these risks in a timely and comprehensive manner.

- Foster data reporting and monitoring across all energy sectors and continue to develop data-sharing arrangements across government and agencies to improve energy data quality for analysis, policy development and the deployment of emergency measures.”[vi]

[i] https://www.iea.org/publications/freepublications/publication/energy-policies-of-iea-countries---australia-2018-review.html

[ii] IEA Report, p.38

[iii] https://www.energy.gov.au/publications/national-energy-security-assessment-2011

[iv] IEA Report, p.17

[v] ibid., p.18

[vi] ibid., pp.21-22

Related Analysis

2025 Election: A tale of two campaigns

The election has been called and the campaigning has started in earnest. With both major parties proposing a markedly different path to deliver the energy transition and to reach net zero, we take a look at what sits beneath the big headlines and analyse how the current Labor Government is tracking towards its targets, and how a potential future Coalition Government might deliver on their commitments.

International Energy Summit: The State of the Global Energy Transition

Australian Energy Council CEO Louisa Kinnear and the Energy Networks Australia CEO and Chair, Dom van den Berg and John Cleland recently attended the International Electricity Summit. Held every 18 months, the Summit brings together leaders from across the globe to share updates on energy markets around the world and the opportunities and challenges being faced as the world collectively transitions to net zero. We take a look at what was discussed.

Great British Energy – The UK’s new state-owned energy company

Last week’s UK election saw the Labour Party return to government after 14 years in opposition. Their emphatic win – the largest majority in a quarter of a century - delivered a mandate to implement their party manifesto, including a promise to set up Great British Energy (GB Energy), a publicly-owned and independently-run energy company which aims to deliver cheaper energy bills and cleaner power. So what is GB Energy and how will it work? We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.