by Peter Brook

Spot market prices and revenues - ten years of historical spot prices

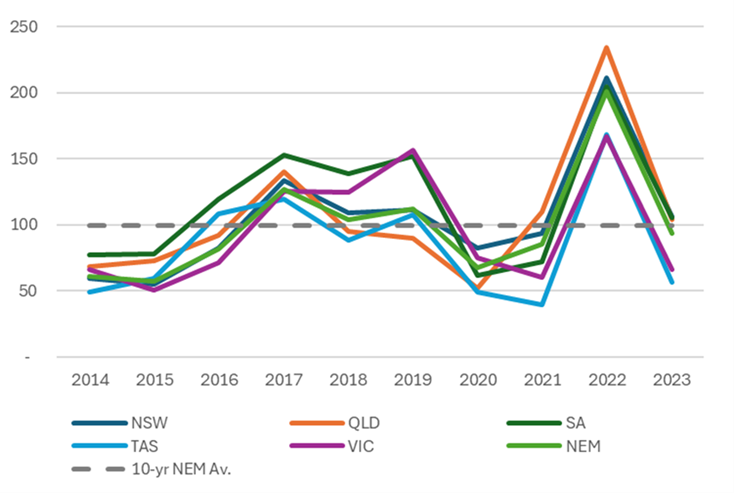

Elevated spot prices have received a lot of attention in recent times, and with justification, following the events of 2022[1]. Since Russia’s invasion of Ukraine in February 2022, and the suspension of the National Electricity Market (NEM) in June 2022, load weighted prices (LWPs) have declined in every jurisdiction across Australia, in some cases, by more than 50 per cent. Figure 1 displays how annual average LWPs in real 2023 dollars, have behaved over the past decade. LWPs are most relevant for consumers as they are derived from both the spot price and the level of demand at that time. In contrast, time weighted prices are a simple average of spot prices. Figure 1 also includes the LWPs for the entire NEM and the 10--year average NEM LWP, which is $99/MWh. The latter figure has been calculated by bringing together the total MWh of operational demand and real spot market revenues over the period.

Figure 1 sets out some major NEM events to provide context for Figure 1.

Figure 1: Real calendar 2023 dollar load weighted prices ($/MWh)

Source: NEOExpress, ABS and AEC analysis

Figure 2: Significant market events

Figure 1 illustrates prices increasing from 2015 which can be partially explained by Queensland LNG exports commencing. Not only did this add additional electricity load but it also exposed the east coast gas market (ECGM) to global LNG prices. Shortly afterwards, it was announced the 1,600 MW Hazelwood power station would be closing within three to four months. Most prices eventually began trending down although the impact of the 520 MW Northern closure in 2018 is clearly apparent in SA prices.

In 2020, COVID-19 and the associated lockdowns saw prices in all regions settling below or at the 10-year NEM average LWP. However, these low prices were short lived, with Russia’s invasion of Ukraine leading to unprecedented coal and gas rises in 2022 In addition, some coal mines had flooding issues, the 840 MW Callide C was offline and COVID restrictions had disrupted plant maintenance schedules. Table 2 sets out some basic descriptive statistics for prices over the past 10 years.

Figure 3: Load weighted price statistics (real calendar 2023 dollars)

Source: NEOExpress, ABS and AEC analysis

As would be expected, the high prices in 2022 greatly expanded the difference between minimum and maximum prices. If this year is removed from the analysis, the 10-year average NEM LWP reduces by $10/MWh to be $89/MWh. For the purposes of this analysis, the data is assumed to be broadly ‘normally’ distributed and has no unit roots (ie, cointegrated) hence, we have calculated the standard deviation (SD) which is a measure of volatility. The SD divided by the average price is an extremely crude volatility measure in percentage terms.

The SD (or sigma) infers that 68 per cent of observations will lie between the average plus, or minus the SD. A two-sigma event (ie, average plus or minus 2 SD) is a one in 20-year probability while a three-sigma event is a one in 333-year event (0.3 per cent probability). As can be seen from Table 2, the 2022 prices yielded sigmas ranging between 1.6 to 2.5, and for the NEM 2.4. Hence 2022 price outcomes were an extremely rare event. South Australia, Tasmania and Victoria were 2.0 sigma or lower ie, no more than a one in twenty year event. This can probably be attributed to:

- the fact that these states are not black coal (ie, exposed to global prices) dependant

- TAS is primarily hydro and renewables

- SA is very gas dependant but has high renewables capacity.

Another interesting statistic is annual spot market revenue. Figure 2 illustrates how in 2022 spot market revenue was twice the 10-year real average. This created enormous balance sheet issues for businesses. For example, if a Victorian brown coal generator had sold a flat $80/MWh futures contract on the ASX, the high prices would have placed this contract well out of the money. As a result, the margining requirements for this contract effectively exploded (ie, need more cash for margin) even though the generator is more than able to make a return on this trade as it is not exposed to export coal prices. Thankfully, prices have receded, and this is demonstrated by 2023 spot revenues being below the real 10-year average of $18.5 billion.

Figure 4: NEM spot market revenue, nominal and real calendar 2023 dollars million

Source: NEOExpress, ABS and AEC analysis

As noted previously, LWPs are the best measure of prices whereas time weighted prices (TWPs) are somewhat of statistical artefact. However, in the course of preparing this paper I compared LWPs with TWPs. Figure 3 displays the difference between LWPs and TWPs. It also includes an ordinary least squares (OLS) trendline (noting that the data is probably cointegrated, but OLS is acceptable for this purpose). What is clearly apparent is that this spread is increasing over time at the rate of $2.80/MWh and the goodness of fit measure is not bad at 0.67. The inference that I draw from this is that LWP volatility is increasing and the driver of this is the solar PV profile (small and large) creating more negative spot prices. Negative prices will be explored in an upcoming Energy Insider.

Figure 5: Difference between LWPs and TWPs real 2023 dollars ($/MWh)

Source: NEOExpress, ABS and AEC analysis

The good news for consumers and business

Figure 6: Future Baseload Wholesale Prices CAL2025 (nominal dollars)

Source: ASX

Figure 6 illustrates how the market has recovered from the confluence of adverse supply events during 2022. The futures market has responded, as the primary driver of futures prices is current spot prices. After peaking in Q3 2022, Calendar 2025 declined sharply, especially in Victoria, but still remained somewhat elevated in NSW and SA. As of 10 March 2023, Victoria is around $60/MWh, SA $80/MWh, Queensland $90/MWh and NSW $100/MWh. This illustrates the bifurcation in the market between the southern and northern states, and this is particularly obvious for Victoria.

The reductions in futures prices will flow through to the wholesale energy component of prices for consumers and businesses. However, it needs to be noted that there are lags in this process as retailers hedge (ie, lock in future energy prices) generally over a two-to-three-year period build. This assumption forms part of the methodology for the AER’s Default Market Offer.

On 19 March 2024 the AER released its 2024–25 DMO 6 draft determination and the change whoesale energy costs are set out in Table 1. NSW and SA have accounted for the significant decreases in flat rates and contolled load with the exception of controlled load in SA. In contrast South East Queensland’s flat rate has only decreased by less than one per cent and controlled load around six to seven per cent. It is worth noting that the prices in this paper are calendar year wheras the AER uses financial year prices.

Table 1: Wholesale costs for the 2024–25 DMO 6 draft determination, $/MWh (excl. GST, nominal)

Note: CL refers to controlled load.

Source: ACIL Allen

Apart from decreasing contract costs the AER noted other factors influencing wholesale costs:

- “Upward cost pressure from the peaky shape of regional load profiles. The continued uptake of household solar PV systems reduces effective demand for grid-scale generation during daylight hours. As a result of this low demand, and exacerbated by grid-scale solar generating at the same time, over-hedging can occur, resulting in increased costs due to large contract for difference payments against base contracts.

- slightly lower costs for several smaller aspects of the WEC, including compensation costs, NEM fees, ancillary services and state-based schemes. In South Australia, these decreases were partially offset by an increase in directions for system security and the South Australian Retailer Energy Productivity Scheme ”

The Victorian Draft 2024-25 VDO was also released on 19 March 2024 and it is currently expecting a 22 per cent decrease in wholesale energy costs, driven by lower contracting costs.

[1] I would like to acknowledge Aaron Martinez from the in AEC for his help with the data collection.

Related Analysis

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Green certification key to Government’s climate ambitions

The energy transition is creating surging corporate demand, both domestically and internationally, for renewable electricity. But with growing scrutiny towards greenwashing, it is critical all green electricity claims are verifiable and credible. The Federal Government has designed a policy to perform this function but in recent months the timing of its implementation has come under some doubt. We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.