by Carl Kitchen

South Australia: Famine one day, feast the next (but one)

South Australia could borrow a slogan from another state based on recent vagaries and challenges thrown up by its energy grid.

One day it experienced spot prices exceeding $5000/MWh six times between 6pm and midnight due to a reserve shortfall and two days later it was reporting near-record minimum demand, which required the unprecedented step of curtailing rooftop solar to ensure grid stability.

Day 1

On Friday 12 March South Australia’s spot prices experienced a reduction in available capacity due to a series of events which led to a reserve shortfall of 131MW for 60 minutes[i]. It’s estimated around 2000MW of firm supply capacity was unavailable on the day.

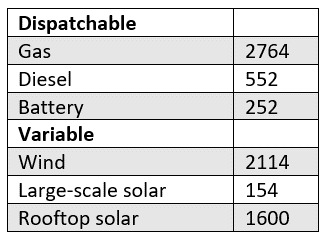

The state has around 3468MW of dispatchable capacity (figure 1). The limited availability of capacity to meet demand led to spot prices going over $5000/MWh six times in the six hours up to midnight.

Figure 1: SA Capacity by type (MW)

Source: NEOmobile

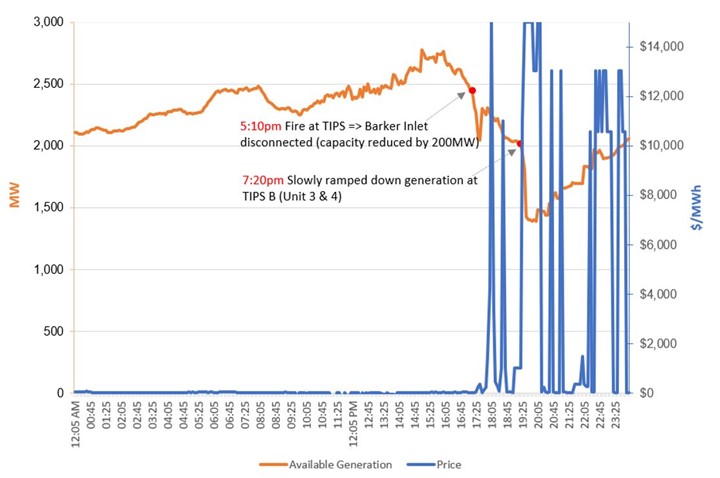

Figure 2: Available generation capacity and price on 12 March 2021 in South Australia

Source: Australian Energy Council analysis

The Australian Energy Regulator (AER) has completed a report into the high price events which outlines the key drivers. It states the reduction in, or access to, low priced capacity stemmed from:

- Planned outages of the Moorabool to Mortlake interconnector with Victoria, which started of 5:06am on 12 March and was expected to continue until 19 March. This work was to repair severe wind damage that occurred in February 2020 and limited South Australia’s ability to import cheaper generation from Victoria. Imports were limited by 350MW across the Heywood interconnector.

- Little wind generation was available because of still weather conditions. Output from the state’s wind capacity of 2114MW fell to as low as 12MW at times.

- A fire in the Torrens Island Power Stations (TIPS) switchyard at 5.10pm, which led to the Barker Inlet Power Station being disconnected and reducing capacity by around 200MW. This had been priced below $61/MWh before it was disconnected.

- Output from TIPS B was limited to close-to-minimum levels by the Australian Energy Market Operator (AEMO) due to the fire. This was maintaining system security; this meant 540MW of capacity that had been priced below $250/MWh became unavailable. While TIPS B had its limit lifted during the day, its total output was still capped at 270MW out of a possible 600MW.

The switchyard failure tripped both the Torrens A and Torrens B high voltage buses that distribute power, also connected TIPS B. Units 2, 3 and 4 at TIPS B were online at the time, and with a risk the station could trip, the market operator constrained the total output to 40MW and capped the output at 240MW.

On top of the unavailability of plant noted above, gas-fired capacity was also unavailable until Pelican Point’s second gas turbine came online later in the day and given and given the time of day there was limited solar generation available. The sunset in Adelaide on 14 March was at 7:35pm.

Demand reached 1752MW at 7.30pm, which is not particularly high for South Australia – in fact not much more than half the summer record. Yet the loss of Barker Inlet generation, TIPS B, as well as the Hornsdale battery and low wind output meant South Australia was running short of spare capacity from 7:30pm and AEMO issued a market notice that only 131MW of spare capacity was available. This lasted for an hour when there was enough spare capacity to cancel the notice.

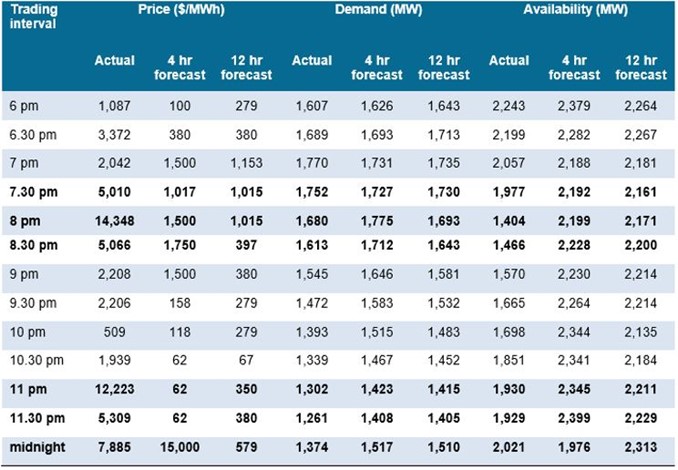

Given the plant availability and level of demand before the incident occurred, price sensitivity forecasts indicated that even a 100MW increase in demand or loss of supply would lead to the 7:30pm trading interval price increasing from $1,017/MWh to $13,100/MWh, according to the AER.

The impact on prices – which ranged from $509/MWh to a high of $14,348/MWh from 6pm to midnight – along with the available capacity and demand is shown in the table below.

Figure 3: Actual and forecast spot price, demand and available capacity

Source: AER

Just another day

In the most dramatic of contrasts, two days later, the state saw demand fall to 358MW a near-record minimum level (the record of 300MW was set on 11 October 2020). The low demand was the result of, mild weather, low demand from industry (it was a Sunday) and a high output of rooftop solar. At the same time the interconnector works as noted above limited exports from South Australia to Victoria.

As would be expected, prices were negative through the surplus period and all large-scale renewable energy self-curtailed to zero output.

Figure 4: Price and demand on 14 March 2021 in South Australia

Source: Australian Energy Council analysis

AEMO had issued a market notice forecasting demand levels below the 400MW considered to be the state’s secure scheduled demand threshold. To maintain system security the market operator directed that steps be taken to maintain grid-demand above the threshold for about an hour from 3pm. The reasons for this minimum secure level of demand are complex and include the need to retain some gas generators on-line at minimum output for “system strength” purposes. There needs to be somewhere to put this minimum output.

As a result, it led to what may well be the first curtailment of rooftop solar in a major grid. The market operator reported that 67MW of solar was curtailed via:

- the SCADA control system involving 17MW of commercial solar PV;

- more than 10MW of distributed solar PV curtailed through registered agents – this is under the Smarter Homes regulations introduced to South Australia on 28 September last year. These require anyone installing or upgrading a solar system to appoint an agent who is responsible for disconnecting and reconnecting the system during state electricity security emergencies; and,

- 40MW of rooftop solar PV curtailed through voltage management at seven substations.

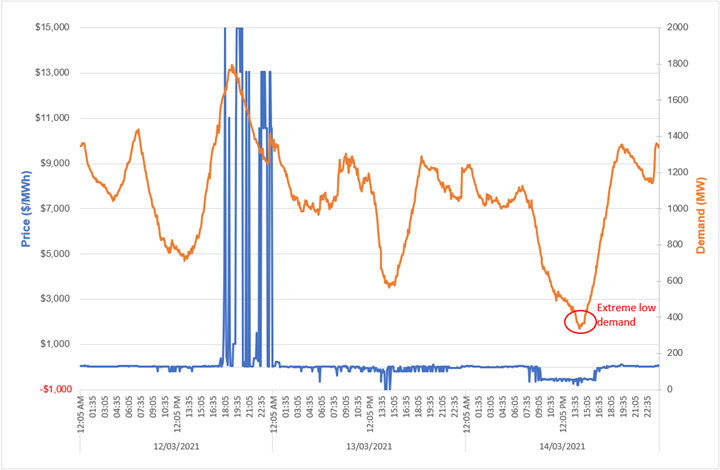

Figure 5: Demand and Price in South Australia from 12 to 14 March 2021

Source: Australian Energy Council analysis

Figure 5 shows the market condition in South Australia across the three days (12 to 14 March) with high volatility in price.

Full details of the high priced events can be found in the AER report.

[i] AEMO issued a reserve notice (83263) with an actual LOR2 condition declared for the SA region from 1930hours. This was cancelled at 2030 (via reserve notice 83268).

Related Analysis

From Energy to Flexibility: Rewiring Australia’s Wholesale Markets for Net Zero

Australia’s path to net zero will depend not only on new technologies, but on fundamentally reshaping the markets that underpin the energy system. As coal exits, renewables, storage and consumer energy resources will drive a far more dynamic and decentralised National Electricity Market, where flexibility becomes the critical commodity. We explore the market reforms, investment signals and system changes required to deliver a secure, affordable and reliable Energy2050 future, themes that will also sit at the centre of the Australian Energy Council Conference 2026 in Sydney on 4 June.

Is increased volatility the new norm?

This year has showcased an increased level of volatility in the National Electricity Market (NEM). To date we have seen significant fluctuations in spot prices with prices hitting both maximum price caps on several occasions and ongoing growth in periods of negative prices with generation being curtailed at times. We took a closer look at why this is happening and the impact this could have on the grid in the future.

Is there a better way to manage AEMO’s costs?

The market operator performs a vital role in managing the electricity and gas systems and markets across Australia. In WA, AEMO recovers the costs of performing its functions via fees paid by market participants, based on expenditure approved by the State’s Economic Regulation Authority. In the last few years, AEMO’s costs have sky-rocketed in WA driven in part by the amount of market reform and the challenges of budgeting projects that are not adequately defined. Here we take a look at how AEMO’s costs have escalated, proposed changes to the allowable revenue framework, and what can be done to keep a lid on costs.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.