by Carl Kitchen

Some highs and lows: Investor sentiment

Some of the challenges being thrown up by the energy transition, in particular around approvals, capacity and supply chain constraints, skilled labour shortages and government interventions are being reflected in the latest assessment of investor sentiment towards the sector.

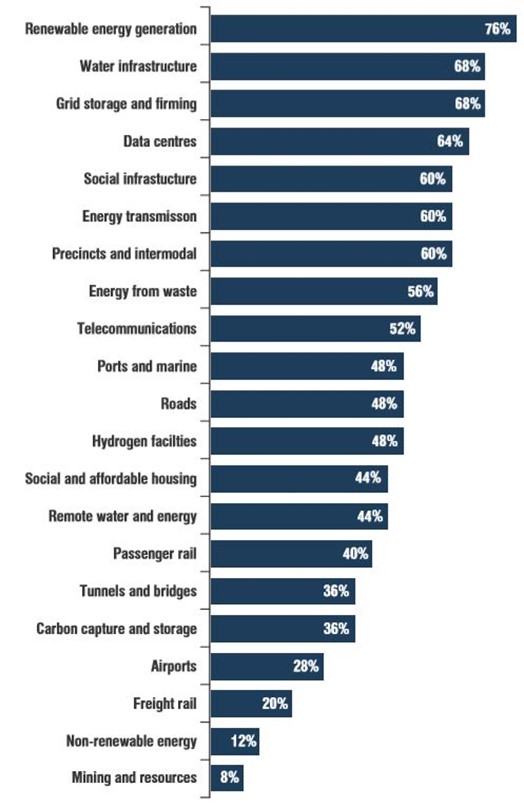

Infrastructure Partnerships Australia’s recently released Investment Monitor shows 76 per cent of investors surveyed identified renewable generation as an attractive asset class, the highest level since the first of the annual assessments was released in 2015. It is also the highest level of interest for any asset class. Sixty-eight per cent of investors involved in the survey also saw batteries/short duration storage as one of the most attractive renewable assets, as shown in figure 1. Figure 2 shows the level of interest for specific technologies.

Figure 1: Level of investor interest

Source: IPA Investment Monitor

Figure 2: Attractiveness by asset type

Source: IPA Investment Monitor

That’s the good news, but the assessment comes with a kicker: “While investor interest is reaching new heights, the pace of delivery of the energy pipeline has slowed over the past 12 months, with projects hitting an approval and delivery backlog. Hesitancy remains among investors, with a number of not insignificant hurdles facing the transition. Growing appetite for renewable projects is a welcome sign, however, industry and governments at all levels will have to work together to overcome these obstacles and shift from intent to action.”

The monitor involves a quantitative survey of 27 senior market participants and then 11 qualitative interviews. The investors involved account for more than $547 billion in infrastructure projects globally. Sixty per cent of those involved have more than half of their assets in Australia while more than half have interests in social infrastructure, renewable generation, roads, transmission and distribution, passenger rail and/or water infrastructure assets.

The outcome of the sentiment review shows investor interest in the energy sector is not always translating into action. Some of the factors at play are already well known but include ongoing capacity and supply chain constraints and skilled labour shortages that are contributing to the Australian infrastructure market “hitting a delivery ceiling”.

The investors involved in this latest report also indicated that inconsistent government interventions “risks shorting out the transition”. The assessment found that 40 per cent of participants were less likely to invest in energy transition infrastructure because of recent interventions, which are cited as “everything from establishing government-owned corporations to direct investments”. These, the monitor notes, are becoming normalised with the questions among investors of how, when and where government intervention is best placed to provide certainty and direction to the market but avoids crowding out private investment.

Where Priorities Lie

A majority of the investors involved in the assessment (56 per cent) already have investments in renewable energy generation, while the 20 per cent that aren’t currently investors have said they would consider it over the next three years.

As mentioned there is a strong appetite for grid storage and firming assets. While only 16 per cent of participants currently hold an investment in grid storage and firming, 52 per cent of participants who identified as not owning a storage and firming asset are interested in investing over the next three years. As one institutional investor commented: “Storage projects are pretty compelling. They carry less development risk than some other assets and they’ve got great ESG[i] profile”.

Another 52 per cent of respondents nominated pumped hydro/long duration storage projects as a preferred focus for investment, although there was a degree of concern expressed by some respondents because of perceived risks, such as construction risks for these developments.

Other Key Findings

Some other interesting take outs from Infrastructure Partnerships survey:

There is a strong preference for the Federal Government to introduce carbon pricing or establish an emissions trading scheme – 72 per cent overall support this to a large or very large extent. Respondents felt that carbon pricing would provide strong incentives for further investment in energy transition infrastructure.

Figure 3: Support for Federal introduction of price on carbon or ETS

Source: IPA Investment Monitor

Impediments to the transition. Like others in the energy sector investors point to limitations to the existing transmission system as a major impediment with 84 per cent of respondents pointing to this as a primary concern, followed by the need for adequate policy and regulatory frameworks to ensure an orderly transition to a lower emissions grid (see figure 4).

Figure 4: Impediments to the energy transition

![]()

Source: IPA Investment Monitor

Participants also flagged concerns about Australia’s slowing progress in delivering the renewable generation, storage and transmission required. And in the case of transmission developments noted the key challenges as being land acquisition, social licence, environmental approvals and high costs.

Hydrogen (20 per cent) and nuclear (4 per cent) were two of the least preferred asset classes. The lack of investor interest in nuclear is easily understood given the hurdles the technology would need to overcome including the long standing Federal Government nuclear prohibition. On hydrogen, Infrastructure Partnerships Australia comments that the lack of interest in at a technology that is being seen as a technology with the potential to transition hard-to-abate sectors stems from “investors… (remaining) uncertain about its realistic application and delivery in the near-term”.

Overall this latest assessment of investor interest shows that while Australia remains an attractive venue for investors and there is a strong interest in the energy transition that has accelerated in recent years “experience shows this is not always resulting in activity” for a variety of reasons. A key requirement will be coordination and collaboration between government and industry in order to deliver “the eye-watering energy transition and social infrastructure build” at a time when the “transport ‘megaproject’ tail is still wagging”.

[i] Environmental, Social and Governance

Related Analysis

Australia’s Home Battery Surge: A Question of Equity

Australia is a global leader in rooftop solar, with more than 4.3 million households and small businesses installing photovoltaic (PV) systems as of February 2026. Battery uptake has also accelerated, particularly since the introduction of the Cheaper Home Batteries Program in July 2025, which offers around a 30 per cent upfront discount for systems between 5 kWh and 100 kWh. More than 236,000 batteries had been installed by February 2026, although this likely understates the true figure due to reporting lags; the Federal Government has since indicated installations have surpassed 250,000 as of March 2026. Despite this rapid growth, an important question remains: who is actually benefiting from these subsidies?

Integrated System Plan – What Should We Expect?

The release of an expert study of last year’s autumn wind drought in Australia by consultancy Global Power Energy[i] this week raised some questions about the approach used by the Australian Energy Market Operator’s in its 2024 Integrated System Plan (ISP). The ISP has been subject to debate before. For example, there has previously been criticism that some of the ISP’s modelling assumes what amounts to “perfect foresight” of wind and solar output and demand[ii], rather than a series of inputs and assumptions. The ISP is produced every two years and with the draft of the next ISP (2026) due for release soon, it is useful to consider what it is and what it is not, along with what the ISP seeks to do.

Getting it right: How to make the “Solar Sharer” work for everyone

On paper, the government’s proposed "Solar Sharer Offer" (SSO) sounds like the kind of policy win that everyone should cheer for. The pitch is delightful: Australia has too much solar power in the middle of the day; the grid is literally overflowing with sunshine: let’s give households free energy during 11am and 2pm. But as the economist Milton Friedman famously warned, "There is no such thing as a free lunch." Here is a no-nonsense guide to making the SSO work.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.