by Matthew Warren

Heat wave ahead: Life after coal

Today is the official start of South Australia’s first summer without coal fired power. The 544MW Northern Power station, the state’s last remaining coal generator, closed in May. In states like South Australia and Victoria, summertime heatwaves produce maximum electricity demand events. So how will the system cope with life after coal?

Heatwaves (three or more days of unusually high temperatures) typically place the South Australian and Victorian electricity grid under stress. Not only is demand at or near maximum demand, but high temperatures and heavy loads can impair the operation of key infrastructure like generators and transmission lines. While heatwaves are predictable and therefore can be planned for, dialing the system up to maximum output increases the risk that if something fails, there will be energy shortages. Unscheduled blackouts can occur during these times for these reasons.

Both South Australia and Victoria tend to have coincident heatwaves, which is important when looking forward to see how a grid with reduced supply from coal fired generators will cope with these events.

Heatwaves are frequently infrequent. The last two major heatwaves in South Australia and Victoria occurred in January 2014 and January 2009 and in South Australian in January 2011. The record peak demand was set in Victoria in January 2009, while the record South Australian demand was set in January 2011.

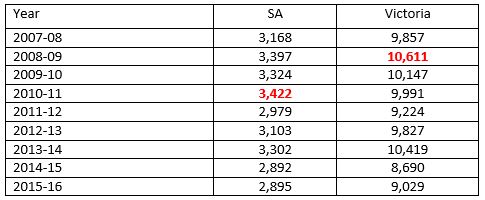

Table 1. Maximum demand in South Australia and Victoria (MW) by year[i]

Source: AEMO

What we know about heatwaves and electricity demand

Just as heat waves are predictable, so there are a range of factors which can vary the level of demand:

Duration of the heatwave: both temperatures and electricity demand tend to increase in the third and fourth days of consecutive hot days, as air conditioners increase output to manage the accumulating heat load in buildings;

School holidays and weekends: demand tends to be higher towards the end of January (or February) when schools and businesses have returned to work, and weekdays have higher demand than weekends;

Solar photovoltaic (PV): increased deploy of rooftop solar PV is helping to both reduce system demand during most summer heatwave peaks (providing there is no cloud cover) and is pushing the maximum peak event to later in the evening.

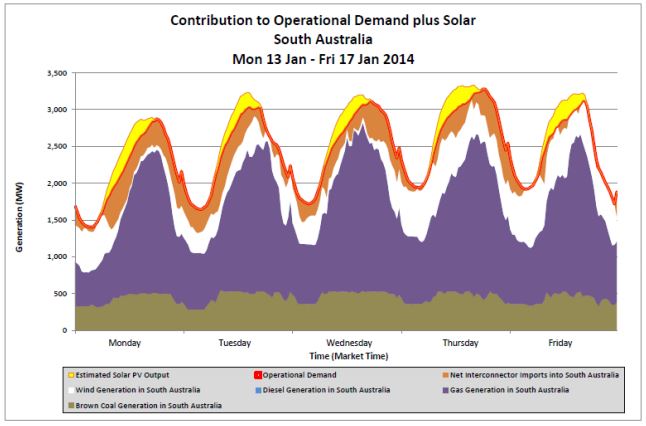

These effects can be seen in the demand profile of the last South Australian heatwave in January 2014.

Figure 2. Contribution to Operational Demand plus Solar – South Australia[ii]

Source: AEMO

What we know about heatwaves and electricity supply

The Australian Energy Market Operator (AEMO) forecasts demand and reports on the generation capacity to meet this demand. The June 2016 National Energy Forecasting Report (NEFR) is reporting flat demand growth across most of Australia, with the exception of increases in demand in Queensland associated with LNG compression.

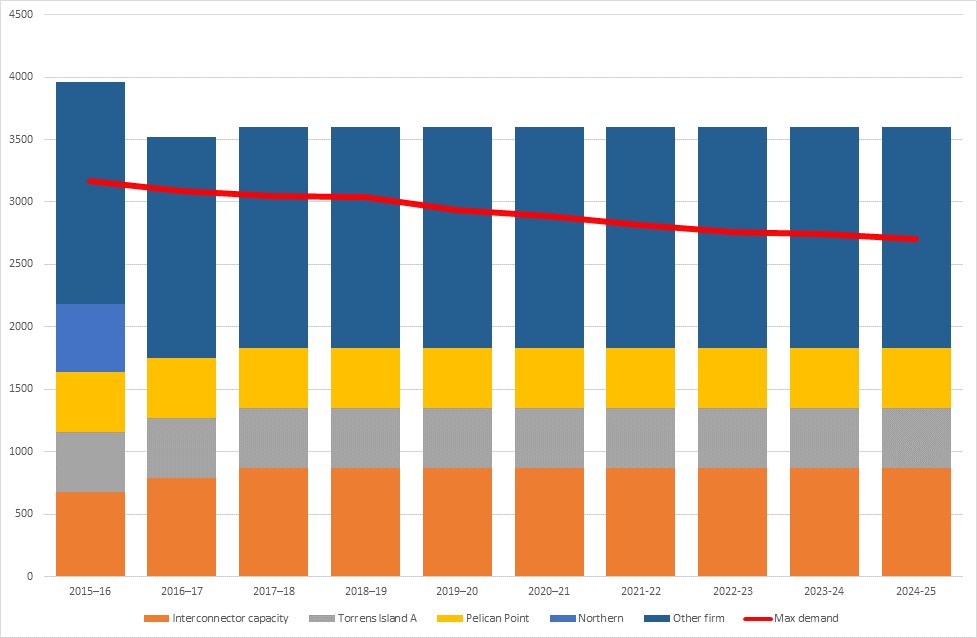

In South Australia, forecast flat electricity demand coupled with continued deploy of rooftop PV means AEMO is forecasting declining demand through to 2024-25. To meet this supply South Australia has firm and intermittent generators, as well as the expanded Heywood and Murraylink interconnectors.

South Australia has 1,595MW of wind generation capacity installed. AEMO has been exploring the extent to which some of this generation could be counted as firm generation, and has notionally estimated a summer firm contribution of 9.4 per cent of this generation. It was noted by AEMO that at times of winter peak demand in July there were periods with virtually no wind generation available.

We can stack the remaining firm generation and interconnection capacity in South Australia and plot it against the forecast demand to estimate minimum reserve margins under predicted maximum demand conditions (Figure 2).

Figure 2: South Australian firm supply and forecast demand (MW) 2015-2025[iii]

Source: AEC, AEMO

This chart shows that minimum reserve margin may be at its lowest in the summer of 2016-17, as a result of the closure of Northern and the remaining interconnector capacity coming progressively on line. Reserve margins appear to increase each year after that, assuming maximum demand continues to fall and all plants remain online. In the context of declining demand, the latter is in practice unlikely, but it is hard to estimate when and which plant will mothball or close first.

If all plant is operating at capacity, even in the event of a zero wind generation heat wave, there should be sufficient capacity to meet maximum demand. The effect of solar PV is reflected in the demand curve (behind the meter) rather than the supply stack. Solar PV is pushing the timing of maximum demand later in the day, meaning that incremental PV has a diminishing effect on maximum demand, as the timing gets closer to sundown.

Both transmission and generation can be impaired by high temperatures and high volumes, as well as faults and outages that can occur during these periods. Additionally, bush fires can impact supply, with electricity outages in this case a result of short-term damage to transmission lines. AEMO reported that during the 2014 heatwave period, fires threatened electrical and gas infrastructure assets.

Further from the Summer 2017-18 Victoria will be operating without the Hazelwood Power station. AEMO forecast this will put Victoria’s firm capacity reserves at -145MW. Assuming imports of up to 590MW from Tasmania into Victoria and 400MW from NSW, it is possible for Victoria to meet its maximum demand and supply South Australia. This in turn relies on a larger network of generators and transmission lines to be operating optimally, which in turn increases the risk and fragility, of the grid as a whole.

[i] AEMO, National Electricity Forecasting Report 2016 and AEMO, Forecast Accuracy Report 2016

[ii] AEMO, Heatwave 13 -17 January 2014 report

[iii] AEMO, 2016 Electricity Statement of Opportunities (ESOO) and AEMO, National Electricity Forecasting Report 2016

Related Analysis

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Green certification key to Government’s climate ambitions

The energy transition is creating surging corporate demand, both domestically and internationally, for renewable electricity. But with growing scrutiny towards greenwashing, it is critical all green electricity claims are verifiable and credible. The Federal Government has designed a policy to perform this function but in recent months the timing of its implementation has come under some doubt. We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.