by Peter Brook

CopperString 2.0: A look at the numbers

North Queensland (NQ) seems to attract its fair share of debate around electricity. Since around 2009 there has been a push to develop a major transmission line – now CopperString 2.0 (CopperString) – to connect Mt Isa to the National Electricity Market (NEM).

Due to its remoteness, Mt Isa and its surrounds were developed as an isolated small grid. Mount Isa is connected to both the Eastern Australian and Carpentaria gas pipelines, which fuels local generation with a growing solar component. The electricity grid has a typical demand of about 370MW.

Discussion around the CopperString proposal has come back into focus recently, with submissions in response to the Queensland Government on Electricity supply options for the North-West Minerals Province Consultation Regulatory Impact Statement (CRIS). Here we take a closer look at the CopperString proposal, the project’s background, options moving forward and the costs and benefits.

Background

Current demand in the North-West Power System (NWPS) is primarily supplied by a combination of Diamantina’s 242MW combined-cycle gas turbine power plant, Leichhardt Power Station’s 60MW open cycle gas turbine power station, and the X41 42MW gas turbine which are operated by private company APA.

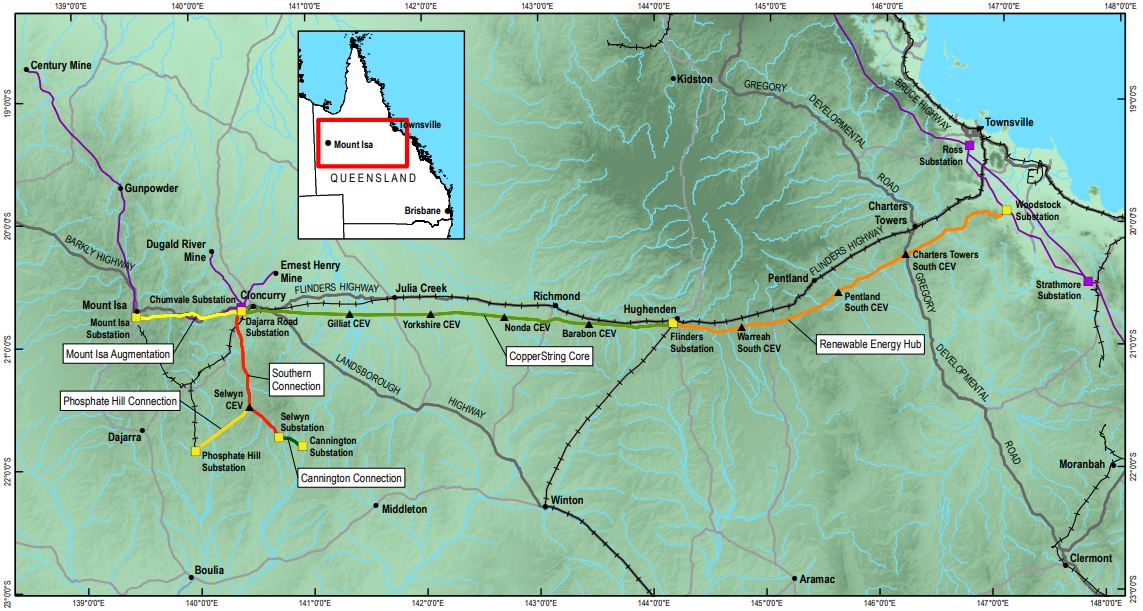

CopperString would be a 1,100km high-voltage dual circuit overhead electricity transmission line with 330kV from Townsville to Cloncurry and then 220kV to Mt Isa. There would also be a “Southern Spur” connecting facilities not currently connected to the NWPS (see Figure 1). Mt Isa and a large area surrounding it are known as the North-West Minerals Province (NWMP) which covers 375,000 square kilometres. The NWMP has been a world class mining region for decades and has substantial potential for exploration and development of both traditional base metals and “new economy minerals”.

Figure 1: CopperString 2.0 plan overview (view larger image)

{kind=link}

Source: CopperString 2.0 website

Proposed options to power the NWMP in the CRIS

The CRIS presents three options for NWMP electricity supply its supply and these options were assessed against three demand scenarios over a 40-year period:

Low demand: Current mining operations run to completion with NWMP demand declining over time.

Flat demand: Demand continues at 373MW.

High demand: Assumes an increase in mining activity because of lower power prices from NEM connection. Demand would peak at 556MW but average 395MW over the 40-year period ie, slightly more than current demand.

The three options are set out below.

Business as usual: Existing generation plant continues and a 200MW solar farm at Mt Isa is commissioned in 2022. As well as this there will be options for further renewables and firming (battery) development. This option has no costs for rest of Queensland (ROQ) electricity consumers and Queensland taxpayers. This option also allows “for generation to scale in alignment with customer demand.”

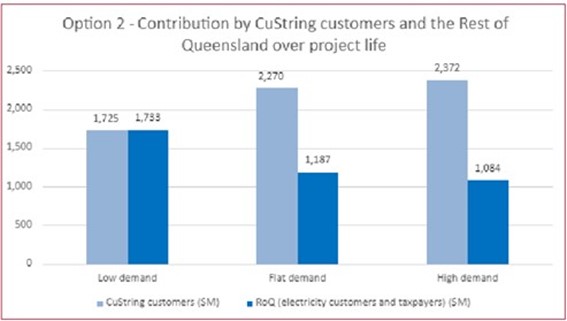

Build CopperString outside the regulatory framework: Where the proponents will require two and a half pages of derogations from the National Electricity Rules (NER) which will shift costs and risks to the ROQ electricity consumers and Queensland taxpayers (CRIS Appendix 1). The value of regulatory asset base (RAB) which will underpin CopperString’s revenues and returns will be determined by an “Independent Expert” rather than the AER. The implication being that the RAB will be higher than what the AER would have allowed.

The CRIS estimates the costs for ROPQ electricity consumers and taxpayers to range from $1.1 billion to $1.7 billion (see Figure 2). While not stated in the CRIS it is likely this is a net present value. The CRIS also notes that if renewable generation connected to the line flows from the west to the east the costs will be higher.

Figure 2

Source: CRIS.

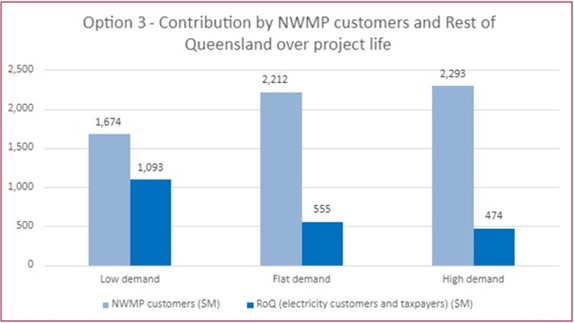

Build CopperString with a modified Regulatory Investment Test for Transmission (RIT-T): While similar to option 2, under this option the project would apply the Australian Energy Regulator’s (AER) regulatory framework through an amended RIT-T process. The Regulation would also be in accordance with the economic parameters applied under the AER’s economic regulatory regime. This option also involves significant costs for Rest of Queensland (ROQ) electricity users and taxpayers.

The CRIS estimates these costs to be between $0.5 billion and $1.1 billion. However, the results presented are the midpoints of high and low cases attributable to different assumptions relating to the size of the regulatory asset base (RAB). Figure 3 illustrates the estimates.

Figure 3

Source: CRIS.

As noted in the CRIS, the objective of National Electricity Law is:

“to promote efficient investment in, and efficient operation and use of, electricity services for the long-term interests of consumers of electricity with respect to:

- price, quality, safety, reliability and security of supply of electricity

- the reliability, safety and security of the national electricity system.”

Of the three options only the first – business as usual – would appear to satisfy this.

More on the costs

In the CRIS, CopperString’s total project costs for CopperString 2.0 are currently estimated at $2.5 billion with the 40-year asset expected to deliver an average of 395MW (or 22MW more than the current level in the flat demand scenario). In contrast, CuString’s website quotes a cost of $1.7 billion (as at 4 March 2022).

By way of comparison, the NEM’s Queensland transmission company, Powerlink, carries 48,204GWh annually with an average load of 5500MW from a RAB of $7.2 billion. On a ratio of transmission RAB against delivered electricity Powerlink costs about $1.3 million per MW and CopperString’s would be $6.3 million per MW (assuming its RAB is $2.5 billion). Recovering the cost of the additional transmission via Powerlink would increase its RAB by 34 per cent to deliver an increase of around 7 per cent in transmitted electricity.

The cost of large transmission projects has been challenging to forecast, for example the EnergyConnect interconnector between South Australia and New South Wales was originally expected to cost $1.5 billion and subsequently increased to $2.28 billion (AER Final Determination May 2021).

Under option 2 , the majority of any cost overruns would be added to the RAB and recovered through project revenues with Queensland Government guarantees, while ROQ electricity consumers also appear to be exposed to this risk.

With respect to the two CopperString options, the CRIS states that “wholesale electricity prices will be $50/MWh for the forecast period.” It is not clear how this figure has been reached or whether it is real or nominal dollars. $50/MWh is a key assumption for the ‘economics’ of both CopperString options as it underpins the comparison with the expected $/MWh under Option 1 business as usual.

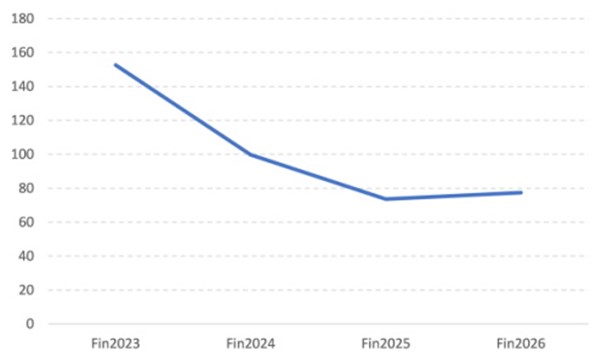

The $50/MWh assumption is difficult to reconcile with current Queensland flat forward prices which are displayed in Figure 4: FY2023 is $153/MWh; FY2024 is $100/MWh; and FY2026 is $77/MWh. Even prior to the recent surge in forward prices, as at 4 March 2022 the outer years were over $70/MWh. The forward prices are in nominal dollars.

Figure 4: Financial Year QLD Flat forward prices on 9 May 2022 ($/MWh)

Source: NEMfutures by Global-Roam

Option 1 - the business-as-usual approach - would see the region continue to draw on existing supply from APA’s gas-fired generation with options to increase local supply via renewables coupled with short duration storage to help meet additional demand. An 8-hour battery energy storage system has been estimated to cost $2959/kW with costs expected to come down as the technology continues to mature.

The cost of renewables and storage continue to fall and are increasingly suited to these types of remote networks and demand. Hybrid systems, combining renewables like solar and batteries, are being developed for mining operations elsewhere in Australia and have the potential for the NWMP region.

Benefits of CopperString?

The CRIS notes that CopperString could support the development of renewable energy in NQ particularly in the Hughenden region. As can be seen from Figure 1, Hughenden is approximately 40 per cent of the way to Mt Isa along the proposed CopperString line. However, the CopperString proposal appears to be a costly way to access these potential renewable resources. An alternative is for the Queensland Government to consider the area around Hughenden for assessment as a renewable energy zone (REZ), which would negate the requirement for CopperString to be built.

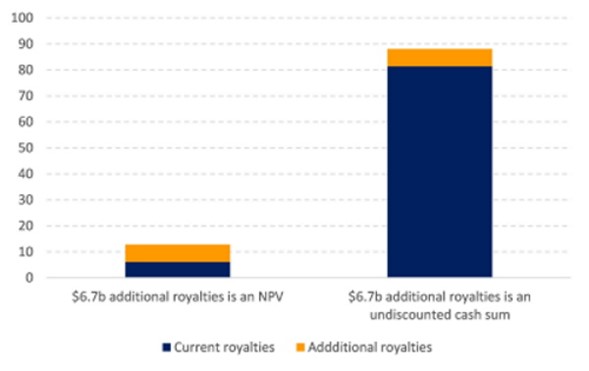

CopperString’s proponents claim that the project will deliver an additional $6.7 billion in royalties and taxes by expanding mining development in the NWMP. The press release does not specify whether it is a simple undiscounted cash sum over 40-years or a net present value (NPV). However, in the same document $40.8 billion in additional GSP at a discount rate of 7 per cent is referred to, so in the first instance it will be assumed to be an NPV with a discount rate of 7 per cent.

In trying to ascertain the spilt between royalties and state taxes (ie, stamp duty, payroll and land tax) the Queensland Resources Council website was examined. 2019/20 royalties and taxes were $4.4 billion according to a QRC commissioned report and on another part of the QRC website royalties alone are reported as $4.5 billion. Based on this it will be assumed the taxes are a small component and will be assumed to be zero.

According to a 2019 Queensland Government report, royalties for the NWMP were $215 million. Escalating this by assumed inflation of 2.5 per cent over 40 years and discounting using 7 per cent produces an NPV for the royalties of $6.1 billion. To achieve the additional $6.7 billion of royalties and taxes (claimed by the proponents), royalties would have to be 110 per cent higher in its first year of operation (ie, $237 million on top of the current $215 million of actual royalties). See the first column in Figure 5.

For completeness, a simple analysis has been conducted on the basis that the $6.7 billion claim is the undiscounted sum of cash flows. Indexing the 2019/20 NWMP $215 million royalties by assumed inflation at 2.5 per cent over 40 years, produces $81.3 billion. To attain the additional royalties claimed by the proponents, in year one the additional royalties would be $17.7 million and indexed by over 40 years sums to $6.7 billion. This represents an 8 per cent increase in royalties from the NWMP over the 40-year period. See the second column in Figure 5.

The results of these two assessments are displayed in Figure 4. As can be seen, they represent two sides of the claimed additional royalties attributable to CopperString.

Figure 5: CopperString additional royalties claim versus current royalties over 40-years ($ billion)

Source: Australian Energy Council analysis, based on CopperString press release, Queensland Government Report data and Queensland Resources Council data.

Conclusion

Committing major investment to a transmission line in a remote area, with limited expected demand growth (even under the high demand scenario), involves significant risk and cost. The project relies on advantageous ore bodies, commodity prices, and investor appetite for the region.

The need for additional transmission within the NEM is undoubted. The Australian Energy Market Operator’s Draft Integrated System Plan (ISP) highlights the importance of managing the energy transition and the role of transmission projects with some $12 billion of “actionable” developments. The ISP however does not mention CopperString.

The business-as-usual option - albeit slightly enhanced - appears the rational option. Transmission projects will also remain high on the agenda given state-based plans for renewable energy zones and perhaps the Queensland Government should consider the area around Hughenden be considered as a renewable energy zone (REZ). But we need to ensure that business cases are carefully considered along with alternative options.

Related Analysis

2025 Election: A tale of two campaigns

The election has been called and the campaigning has started in earnest. With both major parties proposing a markedly different path to deliver the energy transition and to reach net zero, we take a look at what sits beneath the big headlines and analyse how the current Labor Government is tracking towards its targets, and how a potential future Coalition Government might deliver on their commitments.

Retail protection reviews – A view from the frontline

The Australian Energy Regulator (AER) and the Essential Services Commission (ESC) have released separate papers to review and consult on changes to their respective regulation around payment difficulty. Many elements of the proposed changes focus on the interactions between an energy retailer’s call-centre and their hardship customers, we visited one of these call centres to understand how these frameworks are implemented in practice. Drawing on this experience, we take a look at the reviews that are underway.

Data Centres and Energy Demand – What’s Needed?

The growth in data centres brings with it increased energy demands and as a result the use of power has become the number one issue for their operators globally. Australia is seen as a country that will continue to see growth in data centres and Morgan Stanley Research has taken a detailed look at both the anticipated growth in data centres in Australia and what it might mean for our grid. We take a closer look.

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.