by Australian Energy Council

Background on Factors Behind Retail Electricity Prices, DMO/VDO

25 May 2022

Background on Factors Behind Retail Electricity Prices, DMO/VDO

Each financial year Government regulators (the Australian Energy Regulator and the Essential Services Commission in Victoria) set default regulated prices – the Default Market Offer (New South Wales, South Australia and southeast Queensland). Victoria has its own, the Victorian Default Offer (VDO).

These are derived from retailers' overall costs in delivering energy to customers and provide a reference price or cap[i].

The number of people on default offers is not large. This is because default offers are not the cheapest deal out there but exist for customers who don’t want to shop around. More than 90 per cent of customers are on market contracts rather than default offers. The percentage of residential and small business customers on the DMO and VDO (7 per cent and 16 per cent respectively in Victoria) is small and has been falling, with the vast majority of customers on competitive market offers. This is a good thing and is supported by industry which encourages customers to shop around for the best deal.

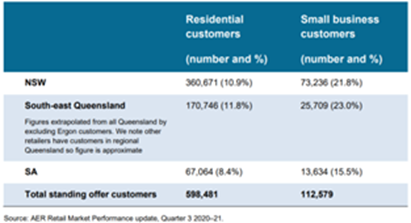

Customers on Default Market Offer

Retailers’ prices must be set based on their input costs. With the ACCC’s powers under the Treasury Laws Amendment (Prohibiting Energy Market Misconduct) Act 2019, the so-called “big stick” legislation, retailers have obligations to ensure price increases are in line with changes to their input costs.

The ACCC reports on prices, profits and margins in electricity supply in the National Energy Market at least every six months. It monitors customer prices, including the level and spread of price offers, and analyses the impact of factors like wholesale prices on retail prices.

Retailers purchase energy contracts in advance to cover their customers’ expected usage in advance.

These contracts (hedges) cover the retailer’s exposure to the highs and lows of the wholesale market, which can fluctuate dramatically (for more details see below).

The prices retailers charge customers vary based on a number of factors, which can include their hedge book. The DMO assumes a retailer will purchase hedges over a three-year period (ie, purchasing a third of their book each year). So, the contracts retailers have in place and when they end can be a factor in determining when and how the wholesale cost component of their electricity charges will change.

When market prices change depends on the retailer’s contracts and the terms of the customer’s contract. In Victoria, they can only increase once a year.

Based on the DMO, the reference price provides a consistent price point against which customers can compare plans. When marketing offers and advising customers about price changes, retailers display how their prices compare to the reference price to give the customer a way to assess the value of a competitive offer.

The best thing to do is shop around in the competitive market for the best deals or use independent websites like https://www.energymadeeasy.gov.au/or in Victoria www.compare.energy.vic.gov.au. The Australian Energy Council always advises people to look for market offers that offer competitive prices compared to the default offers.

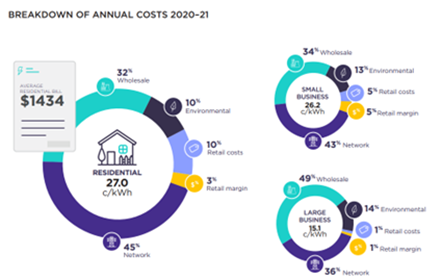

What are the cost components of the average household bill?

The components that make up the average household power bill are shown below.

This breakdown shows the costs for customers:

Source: ACCC

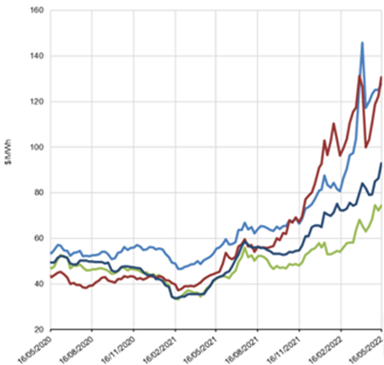

Since late last year, there has been a dramatic increase in the wholesale costs charged to retailers, which is illustrated below (based on future baseload prices).

Wholesale Price Changes

Source: NEMfutures

Wholesale costs are charged to the retailer and passed through to the customer. These costs make up around a third of the charges to consumers. In Q1 2022, the market operator reported a 141 per cent increase in wholesale prices compared to the corresponding period in 2021. This happened even with increased output from renewables. This paper (Residential Electricity Prices) provides a detailed look at the cost components of bills and what can influence them.

Key factors behind higher wholesale costs are:

- Higher fuel costs

- Black coal prices are very high due to international demand.

Coal Price Change (USD/Tonne) 12 Nov 2021-16 May 2022

Note: Newcastle coal futures, the benchmark for top consuming region Asia, consolidated above the US$390-per-tonne mark and has more than doubled in value since the beginning of 2022, supported by continued robust demand against a tightening market backdrop. Source: Trading Economics.

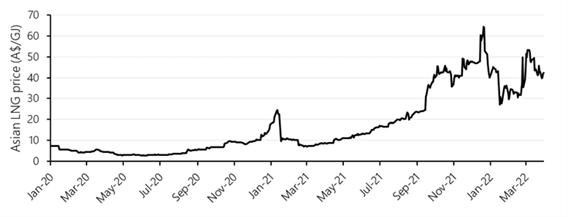

- East coast gas prices at near record levels across the NEM.

- International gas prices at record levels due to geopolitical factors.

Wholesale prices in Queensland and NSW have been significantly higher than in southern NEM states. This is due to the larger price-setting role of black coal generation, as well as transmission constraints limiting daytime electricity transfers from Victoria into NSW.

Wholesale prices can also be impacted by the availability of different types of generation at various times. This can result from plant outages or a lack of resources, such as low wind periods or times of lower availability of sunlight (such as winter and cloudy days), or a combination of these factors (known as Dunkelflaute in Germany).

Plant outages also occur from time to time, both unplanned and planned (when units are taken offline for maintenance and/or upgrades). Generators continue to invest significantly to maintain and upgrade plants. This is usually s for lower demand periods such as autumn and the lead up to summer. The market operator oversees all plant availability.

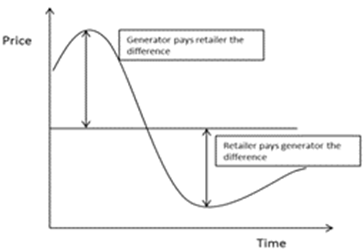

Smoothing Costs to Customers via Hedging

The spot market price can sometimes rise to the market cap (currently $15,100/MWh, increasing to $15,500/MWh from 1 July 2022) or fall to minus $1000/MWh depending on market conditions. In an “energy only” market like the NEM retailers and generators face significant risk if they only sell or purchase energy at spot prices and so they are motivated to provide cost or revenue certainty by contracting (hedging).

An unhedged retailer can face huge losses if prices spike at times of high demand or low supply. Retailers supply homes and businesses with electricity at an agreed price and have to meet that price regardless of spot market price rises and falls.

A generator faces the risk of receiving little or no revenue when spot prices are down. Typically, generators will hedge most of their capacity which will allow them to generate enough power to cover the contract. It is not in a generator’s business interests to have units offline for an extended period.

According to the Productivity Commission[ii], retailers have followed several different strategies, ranging from attempting to fully hedge their position to holding a minimal hedging position and this will often reflect their risk management strategies.

There are a number of derivatives or financial contracts that can be used to hedge but the main contracts are swaps and caps (although there are other contracting choices).

A swap involves both parties entering into a hedging contract which sets the price they will pay for electricity in advance.

These contracts are relatively simple to arrange and involve only the retailer and generator. Under this arrangement, the generator makes a payment to the retailer if the price is high, and the retailer makes a payment to the generator if the price is low. All electricity must be sold through the NEM control pool, however, the two parties settle in cash once the electricity purchase has taken place.

A cap is a hedging contract that gives the holder the option to buy a given amount of electricity at an agreed price. A peaking cap is similar to a flat cap but can only be called on during peak hours.

Smoothing of prices is the basis of the hedging contracts, so if the spot price is high, the generator agrees to pay the retailer, and if the spot price is low, the retailer will pay the generator (below is a simplified illustration of this[iii].

Retail Gas

As with electricity, some energy retailers also enter contracts to manage gas supply and costs to consumers.

The Australian Energy Market Commission (AEMC) breaks down the components of residential gas bills so customers can better understand the structure and the effect of retail competition. The Commission notes[iv] upstream factors determine a significant proportion of a typical retail gas bill.

Wholesale market, transmission and distribution network costs make up the majority of the final price that customers pay. On average network (transmission and distribution pipelines) and wholesale costs make up the bulk of a gas residential customer's bill. “Gas retailers have a limited ability to influence these components; for instance, increased wholesale spot market costs have led to higher contract prices, which in turn increases costs to retailers, particularly those that are not vertically integrated”.

About the Australian Energy Council

The Australian Energy Council is the peak industry body for electricity and downstream natural gas businesses operating in the competitive wholesale and retail energy markets. AEC members generate and sell energy to 10 million homes and businesses and are major investors in renewable energy generation. The AEC supports reaching net-zero by 2050 as well as a 55 per cent emissions reduction target by 2035 and is committed to delivering the energy transition for the benefit of consumers.

Media contact Carl Kitchen 0401 691 342

[i] Retail electricity prices review - Determination of default market offer prices 2022–23 | Australian Energy Regulator (aer.gov.au)

[ii] https://www.pc.gov.au/inquiries/completed/electricity/report/28-electricity-appendixc.pdf

[iii] ibid

[iv] 2020 Retail energy competition review - Final report (aemc.gov.au)

Send an email with your question or comment, and include your name and a short message and we'll get back to you shortly.